Xiaomi Group's Smart EV Strategic Pivot as 24.3% Automotive Margin Signals a Self-Sustaining Capital Cycle

Date : 2026-05-05

Reading : 74

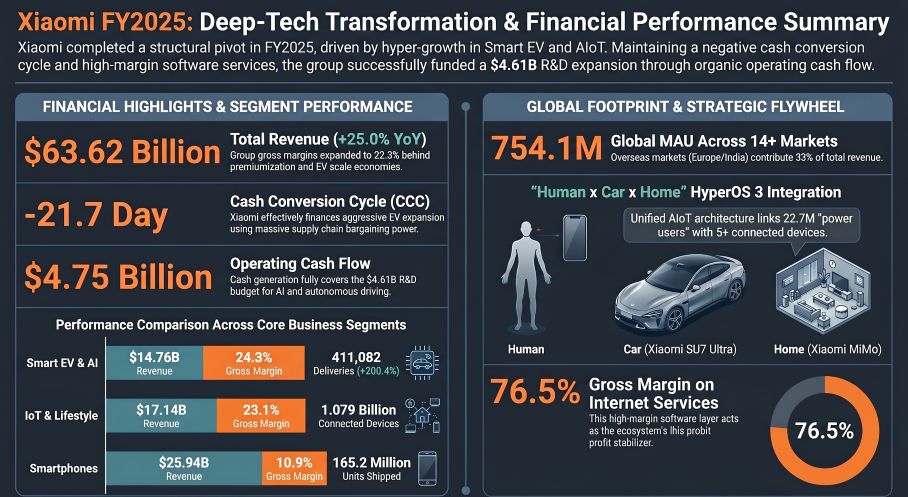

Xiaomi Group has fundamentally de-risked its automotive transition. Disclosed in its 2025 Annual Report, the 24.3% gross margin for the Smart EV segment shatters the bearish thesis of permanent margin dilution. Despite a 37.8% surge in R&D to $4.61B to fund Xiaomi HAD autonomous architectures, the company generated $4.75B in operating cash flow. This organic funding loop at the Beijing EV Factory insulates the firm from broader Chinese NEV price wars, proving its "Human x Car x Home" ecosystem is now a fully monetizable, self-sustaining loop.

Figure Xiaomi FY2025: Deep-Tech Transformation & Financial Performance Summary

Price-Mix Variance and Operating Leverage

Price-Mix Variance and Operating Leverage

While legacy hardware metrics show structural fatigue—smartphone revenue contracted 2.8% to $25.94B with margins compressing to 10.9%—the underlying unit economics reveal a deliberate price-mix variance strategy. Xiaomi is absorbing smartphone margin compression to maintain its 754.1 million MAU acquisition funnel, directly subsidizing the explosive Smart EV & AI segment. The EV division delivered a 223.8% top-line surge to $14.76B, achieving an Average Selling Price (ASP) of $34,945 driven by premium models like the Xiaomi SU7 Ultra and YU7.

Crucially, the aggregate asset turnover remains highly efficient at 1.00x, and the Return on Equity (ROE) hit an exceptional ~18.22%. This signals that the $1.67B allocated to EV Capex is generating immediate operating leverage, rather than sitting as idle capital. Furthermore, stock-based compensation (SBC) of $746.4 million accounts for roughly 17.6% of total remuneration, tightly aligning the deep-tech engineering workforce with shareholder value without draining immediate cash reserves.

The Negative CCC and 'Co-Creation' Resilience

Xiaomi's working capital structure acts as a hidden liquidity engine. The company operates on a heavily inverted Cash Conversion Cycle (CCC) of -21.7 days, holding $15.40B in trade payables against only $2.12B in receivables. This allows HKG: 1810 to force suppliers to underwrite its rapid Capex expansion.

At the Beijing EV Factory, utilization rates are optimized by "super die-casting" technology that consolidates 72 stamped parts into a single body floorpiece in 100 seconds. Rather than pursuing capital-intensive upstream M&A, Xiaomi relies on embedded R&D "co-creation," explicitly co-developing 2,200MPa ultra-high-strength steel and integrating ASIL-D Battery Management Systems (BMS) directly with tier-1 suppliers. Additionally, AI agentic frameworks like Xiaomi MiMo and Miloco within HyperOS 3 streamline cross-device data flows under a strict "Security Shift Left" European GDPR-compliant architecture, effectively neutralizing regulatory pushback in premium overseas markets.

HDIN Institutional Perspective

The Street is rightfully cheering the 24.3% EV margin, but a structural forensic audit reveals two critical pressure points. First, the ecosystem's ultimate profit stabilizer remains the Internet Services division—generating 28.1% of aggregate gross profit on a staggering 76.5% margin. This software monetization engine is actively masking the core smartphone segment's 10.9% margin trough.

Second, the unresolved geopolitical overhang in India—where $526.60 million (INR 48.55 billion) remains frozen over tax and customs disputes—is a material liquidity trap. While management bypassed a formal financial provision, an adverse ruling would instantly wipe out roughly 11% of the group's FY2025 operating cash flow. Xiaomi's execution in scaling EV production is undeniably elite, but its long-term equity upside is entirely tethered to resolving this South Asian capital trap and preventing further ASP dilution in its legacy handset division.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Figure Xiaomi FY2025: Deep-Tech Transformation & Financial Performance Summary

Price-Mix Variance and Operating LeverageWhile legacy hardware metrics show structural fatigue—smartphone revenue contracted 2.8% to $25.94B with margins compressing to 10.9%—the underlying unit economics reveal a deliberate price-mix variance strategy. Xiaomi is absorbing smartphone margin compression to maintain its 754.1 million MAU acquisition funnel, directly subsidizing the explosive Smart EV & AI segment. The EV division delivered a 223.8% top-line surge to $14.76B, achieving an Average Selling Price (ASP) of $34,945 driven by premium models like the Xiaomi SU7 Ultra and YU7.

Crucially, the aggregate asset turnover remains highly efficient at 1.00x, and the Return on Equity (ROE) hit an exceptional ~18.22%. This signals that the $1.67B allocated to EV Capex is generating immediate operating leverage, rather than sitting as idle capital. Furthermore, stock-based compensation (SBC) of $746.4 million accounts for roughly 17.6% of total remuneration, tightly aligning the deep-tech engineering workforce with shareholder value without draining immediate cash reserves.

The Negative CCC and 'Co-Creation' Resilience

Xiaomi's working capital structure acts as a hidden liquidity engine. The company operates on a heavily inverted Cash Conversion Cycle (CCC) of -21.7 days, holding $15.40B in trade payables against only $2.12B in receivables. This allows HKG: 1810 to force suppliers to underwrite its rapid Capex expansion.

At the Beijing EV Factory, utilization rates are optimized by "super die-casting" technology that consolidates 72 stamped parts into a single body floorpiece in 100 seconds. Rather than pursuing capital-intensive upstream M&A, Xiaomi relies on embedded R&D "co-creation," explicitly co-developing 2,200MPa ultra-high-strength steel and integrating ASIL-D Battery Management Systems (BMS) directly with tier-1 suppliers. Additionally, AI agentic frameworks like Xiaomi MiMo and Miloco within HyperOS 3 streamline cross-device data flows under a strict "Security Shift Left" European GDPR-compliant architecture, effectively neutralizing regulatory pushback in premium overseas markets.

HDIN Institutional Perspective

The Street is rightfully cheering the 24.3% EV margin, but a structural forensic audit reveals two critical pressure points. First, the ecosystem's ultimate profit stabilizer remains the Internet Services division—generating 28.1% of aggregate gross profit on a staggering 76.5% margin. This software monetization engine is actively masking the core smartphone segment's 10.9% margin trough.

Second, the unresolved geopolitical overhang in India—where $526.60 million (INR 48.55 billion) remains frozen over tax and customs disputes—is a material liquidity trap. While management bypassed a formal financial provision, an adverse ruling would instantly wipe out roughly 11% of the group's FY2025 operating cash flow. Xiaomi's execution in scaling EV production is undeniably elite, but its long-term equity upside is entirely tethered to resolving this South Asian capital trap and preventing further ASP dilution in its legacy handset division.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*