Digital Imaging Sector Consolidation Phase: Insta360 and GoPro Diverge on Capital Allocation as $406M Inventory Bulge Defines 2026 Outlook

Date : 2026-05-05

Reading : 260

The global digital imaging duopoly has fractured. While Insta360 aggressively scaled FY2025 revenue to $1.35 billion, capturing market share through heavy R&D and proprietary Smart Imaging Equipment Production Base expansions in Mainland China, NASDAQ: GPRO relies on aggressive 29% headcount reductions and an outsourced Southeast Asian supply chain. As US tariff hikes hit GoPro's Malaysian and Thai nodes, Insta360's hyper-growth masks a critical vulnerability: a $406 million inventory overhang. This divergence signals a brutal 2026 sector realignment dictated by balance sheet leverage, cross-border patent warfare, and edge-AI monetization.

Figure Digital lmaging Duel: GoPro vs Insta360-FY2025 Strategic Battlecard

Operating Leverage Collapse vs. Hyper-Growth Burn

Operating Leverage Collapse vs. Hyper-Growth Burn

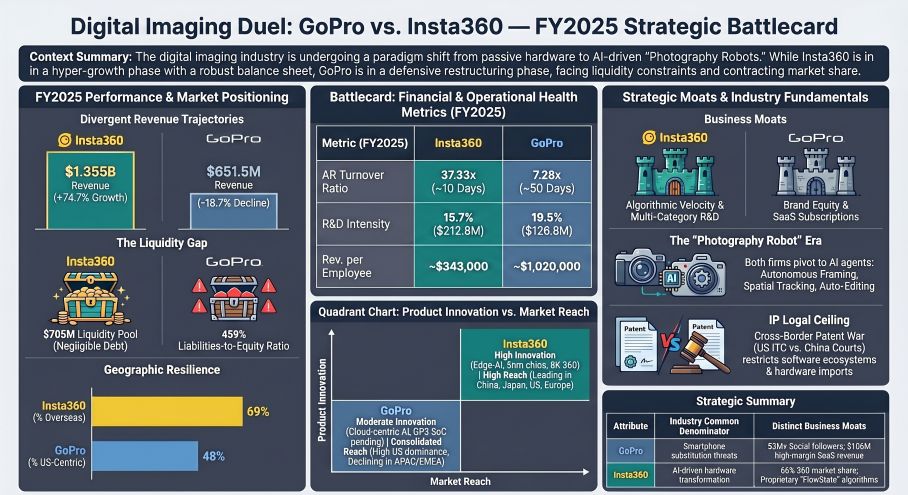

The unit economics between the two imaging giants reflect companies operating at opposite ends of the corporate lifecycle. NASDAQ: GPRO is trapped in a structural contraction. Despite a focused hardware pricing strategy that drove average selling price (ASP) up 8.2% to $357, GoPro posted a devastating net loss of $93.5 million on $651.5 million in total revenue for FY2025. Operating leverage has effectively collapsed; the company suffered a 25% year-over-year plunge in camera shipments (1.82 million units) and was forced to execute emergency amendments in February 2026 to cure breaches of the 1.25x asset coverage and minimum EBITDA covenants on its credit facilities. GoPro’s $1.02 million revenue-per-employee is structurally artificial—an artifact of a 100% outsourced manufacturing model and brutal workforce capitulation.

Conversely, Insta360 is prioritizing market capture over near-term margin retention. The firm generated $1.355 billion in top-line revenue (+74.76% YoY), but its net profit margin compressed to 9.5%. This dilution of profitability is explicitly tied to a massive OPEX burn: $212.8 million deployed into R&D and $233.6 million in Sales & Marketing to push the brand into competitive new categories. Crucially, Insta360's earnings quality reveals extreme supply chain leverage. Its $192.8 million in operating cash flow was largely manufactured by stretching its accounts payable by $386.1 million. Insta360 is effectively utilizing its component vendors as an un-covenanted credit facility to fund its rapid hardware iterations.

Comparative Resilience and IP Warfare

The comparative resilience of both firms is currently tested by geographic concentration and aggressive inventory cycles. Insta360 boasts a hyper-efficient 10-day Accounts Receivable cycle, heavily outpacing GoPro's 50-day cycle due to superior direct-to-consumer channel leverage. Furthermore, Insta360 sits on a highly liquid $705 million balance sheet fortress. However, this is offset by an extreme inventory obsolescence risk: Insta360's inventory balance surged 191.88% YoY to $406.1 million. In the fast-iterating hardware sector, hoarding half a billion dollars in material exposes the firm to severe margin-crushing write-downs if consumer demand decelerates.

NASDAQ: GPRO operates a leaner balance sheet ($78.4 million inventory) but faces critical supply chain bottlenecks. Its complete reliance on sole-source components (like the GP3 custom SoC) and geographically dispersed contract manufacturers leaves it highly exposed to macroeconomic shocks. Specifically, GoPro's decision to shift U.S.-bound manufacturing out of China into Thailand and Malaysia backfired when these regions were hit with an August 2025 U.S. tariff hike from 10% to 19%, permanently structurally impairing gross margins.

The ultimate competitive ceiling, however, is being drafted in international courts. The firms are locked in mutually destructive intellectual property warfare. GoPro successfully utilized US ITC Section 337 to enforce import bans against Insta360's AI-enabled Ace and Ace Pro 2 action cameras, attempting to ring-fence its core Americas market. In retaliation, Insta360 launched a $26.5 million multi-jurisdictional patent assault in Chinese courts targeting GoPro's high-margin Quik software ecosystem—threatening the very subscription model GoPro relies on for survival. Simultaneously, Insta360's attempt to expand its hardware moat into panoramic drones was instantly contested by DJI, which filed a six-patent lawsuit specifically targeting the Antigravity A1 drone, effectively capping Insta360's total addressable market expansion.

HDIN Institutional Perspective

The sector is entering a definitive 'trough-discovery' phase. While Insta360’s top-line dominance and rapid integration of edge-AI "Photography Robots" project overwhelming market momentum, its $406 million inventory overhang suggests a severe 2H2026 margin squeeze is inevitable if the global consumer electronics cycle rolls over. The company's massive payable leverage will immediately invert into a liquidity trap if turnover slows. Conversely, GoPro’s hyper-outsourced, defensive posture cannot mask a fundamental decay in structural ROIC. Management's attempt to pivot into cloud-based AI monetization and tech-enabled helmets is vastly undercapitalized against Insta360's $212 million annual R&D spend. Unless GoPro can extract significant recurring revenue from its proprietary AI Training programs, it faces a protracted path to irrelevance, while Insta360 risks choking on its own hardware supply.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Figure Digital lmaging Duel: GoPro vs Insta360-FY2025 Strategic Battlecard

Operating Leverage Collapse vs. Hyper-Growth BurnThe unit economics between the two imaging giants reflect companies operating at opposite ends of the corporate lifecycle. NASDAQ: GPRO is trapped in a structural contraction. Despite a focused hardware pricing strategy that drove average selling price (ASP) up 8.2% to $357, GoPro posted a devastating net loss of $93.5 million on $651.5 million in total revenue for FY2025. Operating leverage has effectively collapsed; the company suffered a 25% year-over-year plunge in camera shipments (1.82 million units) and was forced to execute emergency amendments in February 2026 to cure breaches of the 1.25x asset coverage and minimum EBITDA covenants on its credit facilities. GoPro’s $1.02 million revenue-per-employee is structurally artificial—an artifact of a 100% outsourced manufacturing model and brutal workforce capitulation.

Conversely, Insta360 is prioritizing market capture over near-term margin retention. The firm generated $1.355 billion in top-line revenue (+74.76% YoY), but its net profit margin compressed to 9.5%. This dilution of profitability is explicitly tied to a massive OPEX burn: $212.8 million deployed into R&D and $233.6 million in Sales & Marketing to push the brand into competitive new categories. Crucially, Insta360's earnings quality reveals extreme supply chain leverage. Its $192.8 million in operating cash flow was largely manufactured by stretching its accounts payable by $386.1 million. Insta360 is effectively utilizing its component vendors as an un-covenanted credit facility to fund its rapid hardware iterations.

Comparative Resilience and IP Warfare

The comparative resilience of both firms is currently tested by geographic concentration and aggressive inventory cycles. Insta360 boasts a hyper-efficient 10-day Accounts Receivable cycle, heavily outpacing GoPro's 50-day cycle due to superior direct-to-consumer channel leverage. Furthermore, Insta360 sits on a highly liquid $705 million balance sheet fortress. However, this is offset by an extreme inventory obsolescence risk: Insta360's inventory balance surged 191.88% YoY to $406.1 million. In the fast-iterating hardware sector, hoarding half a billion dollars in material exposes the firm to severe margin-crushing write-downs if consumer demand decelerates.

NASDAQ: GPRO operates a leaner balance sheet ($78.4 million inventory) but faces critical supply chain bottlenecks. Its complete reliance on sole-source components (like the GP3 custom SoC) and geographically dispersed contract manufacturers leaves it highly exposed to macroeconomic shocks. Specifically, GoPro's decision to shift U.S.-bound manufacturing out of China into Thailand and Malaysia backfired when these regions were hit with an August 2025 U.S. tariff hike from 10% to 19%, permanently structurally impairing gross margins.

The ultimate competitive ceiling, however, is being drafted in international courts. The firms are locked in mutually destructive intellectual property warfare. GoPro successfully utilized US ITC Section 337 to enforce import bans against Insta360's AI-enabled Ace and Ace Pro 2 action cameras, attempting to ring-fence its core Americas market. In retaliation, Insta360 launched a $26.5 million multi-jurisdictional patent assault in Chinese courts targeting GoPro's high-margin Quik software ecosystem—threatening the very subscription model GoPro relies on for survival. Simultaneously, Insta360's attempt to expand its hardware moat into panoramic drones was instantly contested by DJI, which filed a six-patent lawsuit specifically targeting the Antigravity A1 drone, effectively capping Insta360's total addressable market expansion.

HDIN Institutional Perspective

The sector is entering a definitive 'trough-discovery' phase. While Insta360’s top-line dominance and rapid integration of edge-AI "Photography Robots" project overwhelming market momentum, its $406 million inventory overhang suggests a severe 2H2026 margin squeeze is inevitable if the global consumer electronics cycle rolls over. The company's massive payable leverage will immediately invert into a liquidity trap if turnover slows. Conversely, GoPro’s hyper-outsourced, defensive posture cannot mask a fundamental decay in structural ROIC. Management's attempt to pivot into cloud-based AI monetization and tech-enabled helmets is vastly undercapitalized against Insta360's $212 million annual R&D spend. Unless GoPro can extract significant recurring revenue from its proprietary AI Training programs, it faces a protracted path to irrelevance, while Insta360 risks choking on its own hardware supply.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*