United Imaging Healthcare Aggressively Penetrates Western Markets as 1.43x OCF Conversion Signals Pristine Earnings Quality

Date : 2026-05-05

Reading : 102

United Imaging Healthcare (SHA: 688271) achieved a massive 75.18% surge in core operational profit for FY2025, neutralizing geopolitical friction via a decentralized "In-Region, For-Region" supply chain. By tripling capacity at its Houston Manufacturing Center and capturing $41.74M in direct savings through aggressive component localization, UIH successfully insulated its margin profile from Section 301 tariffs. As the uCT Ultima and uMR Jupiter 5T displace legacy oligopolies across North America and Europe, the company's 1.43x operating cash flow conversion cements its transition from regional challenger to cash-generative global tier-1 incumbent.

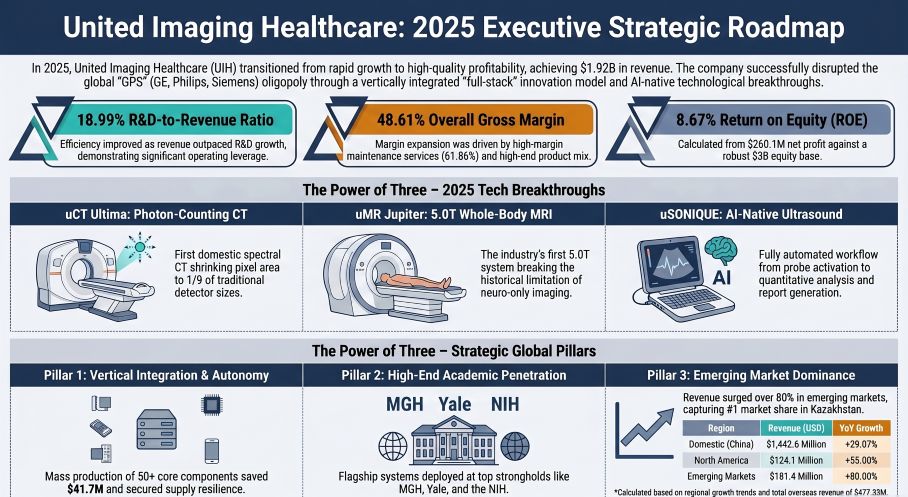

Figure United lmaging Healthcare 2025: Executive Strategic Roadmap

Operating Leverage and Working Capital Integrity

Operating Leverage and Working Capital Integrity

UIH’s top-line expansion to $1.92B (+33.98% YoY) masks a far more critical structural shift in unit economics: the aggressive scaling of its high-margin aftermarket operations. Service revenue surged 25.96% to $237.64M, pulling an outsized 61.86% gross margin that mathematically anchored the firm's bottom-line expansion. As UIH's global installed base breached 39,000 units, the dilution of fixed operational expenses generated massive operating leverage, with SG&A and R&D vertically compressing by 2.16 and 3.75 percentage points, respectively.

The Quality of Earnings (QoE) is exceptionally clean. The firm engineered a $458.86M absolute swing in Operating Cash Flow—from a negative position in 2024 to +$372.73M in 2025—yielding a 1.43x conversion ratio against its $260.08M net profit. Working capital metrics definitively rule out channel stuffing or supply chain bottlenecks: Accounts Receivable grew at 28.25% (trailing revenue growth), shrinking Days Sales Outstanding (DSO), while Inventory crawled at a microscopic 3.63% against a 37.97% COGS jump. This inventory-to-COGS divergence indicates hyper-accelerated asset turnover and the successful liquidation of legacy buffer stocks. Capital allocation exhibits strict discipline; management pragmatically deferred $1.08B in heavy-capex R&D and industrialization drawdowns to 2027 to avoid premature overcapacity, while fully deploying $278.26M to inject immediate liquidity into its global sales network.

Vertical Integration as Geopolitical Hedge

UIH is systematically dismantling its reliance on vulnerable global feedstocks and third-party markup. By executing domestic mass-production switching for over 50 core components in 2025, the firm recognized over $41.74M in direct material cost savings. To counter escalating global resource scarcity, UIH engineered a technological bypass around the liquid helium supply chain, deploying zero-boil-off and low-liquid-helium superconducting magnets across its MRI portfolio.

Geographically, UIH is utilizing localized infrastructure to absorb macroeconomic shocks. The threefold capacity expansion at the Houston facility enables agile forward-stocking, effectively stripping out cross-border logistics friction and acting as a physical hedge against U.S.-China trade volatility. The R&D-to-Moat translation is equally formidable. The commercialization of the uMR 600—equipped with proprietary Silicon Carbide (SiC) Gradient Power Amplifiers—slashes operational energy consumption by over 53%, delivering a mathematically superior Total Cost of Ownership (TCO) proposition to Western hospital administrators. This underlying cost-leadership structure provides UIH the pricing elasticity required to underbid the entrenched GE HealthCare, Philips Healthcare, and Siemens Healthineers oligopoly without compressing its own 46.56% equipment gross margin.

HDIN Institutional Perspective

We confirm the bull case on UIH’s cash-generation capabilities, but the aggressive 7.64 percentage-point spike in the R&D capitalization rate (reaching 29.73%) warrants strict institutional scrutiny. While management correctly maps this to a cluster of late-stage clinical validations and new FDA/CE clearances for systems like the uAngio AVIVA, any future regulatory bottlenecks in the U.S. or EU could rapidly force these capitalized assets back into the P&L as aggressive write-downs. Furthermore, while the 51.39% surge in international revenue proves market viability, UIH’s long-term valuation multiple will not be dictated by hardware placements. The true test of UIH's global durability will be its ability to scale 60%+ margin recurring service contracts in North America against the deeply entrenched, decades-old service monopolies held by Western incumbents.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Figure United lmaging Healthcare 2025: Executive Strategic Roadmap

Operating Leverage and Working Capital IntegrityUIH’s top-line expansion to $1.92B (+33.98% YoY) masks a far more critical structural shift in unit economics: the aggressive scaling of its high-margin aftermarket operations. Service revenue surged 25.96% to $237.64M, pulling an outsized 61.86% gross margin that mathematically anchored the firm's bottom-line expansion. As UIH's global installed base breached 39,000 units, the dilution of fixed operational expenses generated massive operating leverage, with SG&A and R&D vertically compressing by 2.16 and 3.75 percentage points, respectively.

The Quality of Earnings (QoE) is exceptionally clean. The firm engineered a $458.86M absolute swing in Operating Cash Flow—from a negative position in 2024 to +$372.73M in 2025—yielding a 1.43x conversion ratio against its $260.08M net profit. Working capital metrics definitively rule out channel stuffing or supply chain bottlenecks: Accounts Receivable grew at 28.25% (trailing revenue growth), shrinking Days Sales Outstanding (DSO), while Inventory crawled at a microscopic 3.63% against a 37.97% COGS jump. This inventory-to-COGS divergence indicates hyper-accelerated asset turnover and the successful liquidation of legacy buffer stocks. Capital allocation exhibits strict discipline; management pragmatically deferred $1.08B in heavy-capex R&D and industrialization drawdowns to 2027 to avoid premature overcapacity, while fully deploying $278.26M to inject immediate liquidity into its global sales network.

Vertical Integration as Geopolitical Hedge

UIH is systematically dismantling its reliance on vulnerable global feedstocks and third-party markup. By executing domestic mass-production switching for over 50 core components in 2025, the firm recognized over $41.74M in direct material cost savings. To counter escalating global resource scarcity, UIH engineered a technological bypass around the liquid helium supply chain, deploying zero-boil-off and low-liquid-helium superconducting magnets across its MRI portfolio.

Geographically, UIH is utilizing localized infrastructure to absorb macroeconomic shocks. The threefold capacity expansion at the Houston facility enables agile forward-stocking, effectively stripping out cross-border logistics friction and acting as a physical hedge against U.S.-China trade volatility. The R&D-to-Moat translation is equally formidable. The commercialization of the uMR 600—equipped with proprietary Silicon Carbide (SiC) Gradient Power Amplifiers—slashes operational energy consumption by over 53%, delivering a mathematically superior Total Cost of Ownership (TCO) proposition to Western hospital administrators. This underlying cost-leadership structure provides UIH the pricing elasticity required to underbid the entrenched GE HealthCare, Philips Healthcare, and Siemens Healthineers oligopoly without compressing its own 46.56% equipment gross margin.

HDIN Institutional Perspective

We confirm the bull case on UIH’s cash-generation capabilities, but the aggressive 7.64 percentage-point spike in the R&D capitalization rate (reaching 29.73%) warrants strict institutional scrutiny. While management correctly maps this to a cluster of late-stage clinical validations and new FDA/CE clearances for systems like the uAngio AVIVA, any future regulatory bottlenecks in the U.S. or EU could rapidly force these capitalized assets back into the P&L as aggressive write-downs. Furthermore, while the 51.39% surge in international revenue proves market viability, UIH’s long-term valuation multiple will not be dictated by hardware placements. The true test of UIH's global durability will be its ability to scale 60%+ margin recurring service contracts in North America against the deeply entrenched, decades-old service monopolies held by Western incumbents.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*