Luxury EV Trough-Discovery: Lucid, Polestar, and Lotus Diverge on Vertical Integration as Tariff Shock Defines 2026 Outlook

Date : 2026-05-04

Reading : 440

In FY2025, a brutal 137.5% U.S. tariff wall and the repeal of U.S. EV subsidies under the OBBBA forced a structural divergence across luxury automakers. While NASDAQ: LCID leveraged its Saudi sovereign backing to absorb a massive $815.7M inventory write-down at its AMP-1 facility, NASDAQ: PSNY and NASDAQ: LOT absorbed a combined $5 billion working capital deficit. Geopolitical decoupling has mathematically destroyed the asset-light arbitrage of Chinese-manufactured EVs in Western markets, triggering formal going-concern warnings for both Geely-backed entities heading into 2026.

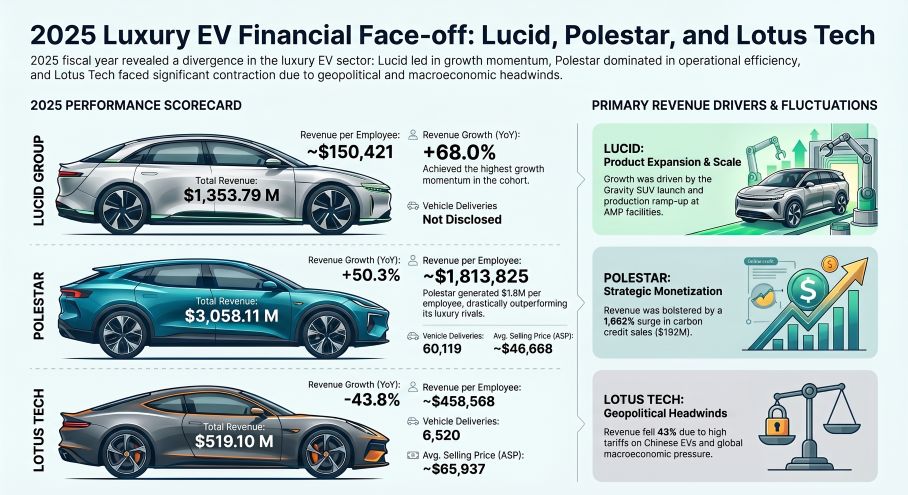

Figure 2025 Luxury EV Financial Face-off: Lucid, Polestar, and Lotus Tech

Margin Collapse and Phantom Operating Leverage

Margin Collapse and Phantom Operating Leverage

Top-line revenue optics mask a sector-wide unit economics crisis. NASDAQ: LCID captured the highest growth momentum (+68.0% YoY to $1.35 billion), driven by the Lucid Gravity launch. However, vertical integration generated a staggering 92.8% negative gross margin, severely distorted by $815.7 million in Lower of Cost or Net Realizable Value (LCNRV) inventory write-downs. Lucid's cash burn (OCF + CapEx) is approaching $3.8 billion, offset only by repeated equity injections from the Saudi PIF.

Conversely, NASDAQ: PSNY achieved peak revenue scale ($3.06 billion) and extraordinary optical efficiency, generating ~$1.81 million per employee. Yet, this "asset-light" leverage is superficial. Polestar’s GAAP gross loss of $1.08 billion was driven by a $1.05 billion non-cash impairment against the Polestar 2, 3, and 5 platforms due to collapsed European demand. Polestar's operating cash flow was artificially insulated by delaying related-party payables to Geely/Volvo, while its underlying margins were only salvaged by a 1,662% surge in EU carbon pool credit sales ($192.38 million).

NASDAQ: LOT remains the ultimate laggard. Revenue contracted 43.8% to $519.1 million amid a "gradual destocking" phase. A forced pivot from Direct-to-Consumer (D2C) to legacy dealer networks offloaded inventory risk but required massive wholesale rebating, effectively subsidizing Customer Acquisition Cost (CAC) by cannibalizing product margin. Furthermore, Lotus's boutique volume (6,520 units) yields highly toxic SG&A inefficiencies, exceeding $43,000 in overhead per vehicle.

Geopolitical Bottlenecks and Contract Agility

Supply chain resilience is currently dictated entirely by tariff avoidance. NASDAQ: PSNY demonstrates extreme geopolitical agility, dynamically routing production around the 137.5% U.S. tariff wall by shifting Polestar 3 assembly to Charleston, USA, and Polestar 4 to Busan, South Korea (dropping import tariffs to 15.0%).

NASDAQ: LOT is fundamentally bottlenecked. 100% of its lifestyle EV production is locked into Geely's Wuhan Global Smart Factory. This geographic concentration essentially prohibits commercial entry into the U.S. and absorbs a punitive 28.8% EU anti-subsidy duty, destroying structural pricing power.

Meanwhile, NASDAQ: LCID executes the tightest operational control. By manufacturing proprietary LEAP architectures, miniaturized integrated drive units, and Wunderbox charging systems in-house at AMP-1 (Arizona) and AMP-2 (KAEC, Saudi Arabia), Lucid insulates itself from the capacity constraints and inter-company cost-plus markups that plague the Volvo/Geely contract-manufacturing ecosystem. However, this vertical integration comes at the cost of acute raw-material single-sourcing vulnerabilities.

HDIN Institutional Perspective

The luxury EV sector has entered an existential trough-discovery phase. While NASDAQ: LCID projects long-term structural dominance due to its proprietary 5.0 miles/kWh efficiency and unyielding sovereign liquidity, the "asset-light" models of NASDAQ: PSNY and NASDAQ: LOT are failing under the weight of geopolitical decoupling. Polestar’s $3.52 billion net current liability deficit and Lotus’s highly dilutive "stock-settled" debt provisions signal an imminent 2026 restructuring cycle. Outsourced manufacturing is a liability, not a moat, when punitive U.S. and EU tariffs eviscerate the underlying unit economics of Chinese assembly lines.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Figure 2025 Luxury EV Financial Face-off: Lucid, Polestar, and Lotus Tech

Margin Collapse and Phantom Operating LeverageTop-line revenue optics mask a sector-wide unit economics crisis. NASDAQ: LCID captured the highest growth momentum (+68.0% YoY to $1.35 billion), driven by the Lucid Gravity launch. However, vertical integration generated a staggering 92.8% negative gross margin, severely distorted by $815.7 million in Lower of Cost or Net Realizable Value (LCNRV) inventory write-downs. Lucid's cash burn (OCF + CapEx) is approaching $3.8 billion, offset only by repeated equity injections from the Saudi PIF.

Conversely, NASDAQ: PSNY achieved peak revenue scale ($3.06 billion) and extraordinary optical efficiency, generating ~$1.81 million per employee. Yet, this "asset-light" leverage is superficial. Polestar’s GAAP gross loss of $1.08 billion was driven by a $1.05 billion non-cash impairment against the Polestar 2, 3, and 5 platforms due to collapsed European demand. Polestar's operating cash flow was artificially insulated by delaying related-party payables to Geely/Volvo, while its underlying margins were only salvaged by a 1,662% surge in EU carbon pool credit sales ($192.38 million).

NASDAQ: LOT remains the ultimate laggard. Revenue contracted 43.8% to $519.1 million amid a "gradual destocking" phase. A forced pivot from Direct-to-Consumer (D2C) to legacy dealer networks offloaded inventory risk but required massive wholesale rebating, effectively subsidizing Customer Acquisition Cost (CAC) by cannibalizing product margin. Furthermore, Lotus's boutique volume (6,520 units) yields highly toxic SG&A inefficiencies, exceeding $43,000 in overhead per vehicle.

Geopolitical Bottlenecks and Contract Agility

Supply chain resilience is currently dictated entirely by tariff avoidance. NASDAQ: PSNY demonstrates extreme geopolitical agility, dynamically routing production around the 137.5% U.S. tariff wall by shifting Polestar 3 assembly to Charleston, USA, and Polestar 4 to Busan, South Korea (dropping import tariffs to 15.0%).

NASDAQ: LOT is fundamentally bottlenecked. 100% of its lifestyle EV production is locked into Geely's Wuhan Global Smart Factory. This geographic concentration essentially prohibits commercial entry into the U.S. and absorbs a punitive 28.8% EU anti-subsidy duty, destroying structural pricing power.

Meanwhile, NASDAQ: LCID executes the tightest operational control. By manufacturing proprietary LEAP architectures, miniaturized integrated drive units, and Wunderbox charging systems in-house at AMP-1 (Arizona) and AMP-2 (KAEC, Saudi Arabia), Lucid insulates itself from the capacity constraints and inter-company cost-plus markups that plague the Volvo/Geely contract-manufacturing ecosystem. However, this vertical integration comes at the cost of acute raw-material single-sourcing vulnerabilities.

HDIN Institutional Perspective

The luxury EV sector has entered an existential trough-discovery phase. While NASDAQ: LCID projects long-term structural dominance due to its proprietary 5.0 miles/kWh efficiency and unyielding sovereign liquidity, the "asset-light" models of NASDAQ: PSNY and NASDAQ: LOT are failing under the weight of geopolitical decoupling. Polestar’s $3.52 billion net current liability deficit and Lotus’s highly dilutive "stock-settled" debt provisions signal an imminent 2026 restructuring cycle. Outsourced manufacturing is a liability, not a moat, when punitive U.S. and EU tariffs eviscerate the underlying unit economics of Chinese assembly lines.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*