Global Semiconductor Decoupling Phase: NASDAQ: AMD, NASDAQ: INTC, and SHSE: 688047 Diverge on CAPEX Allocation as 900-Day Inventory Spreads Define 2026 Outlook

Date : 2026-05-04

Reading : 567

AMD's $440 million inventory write-down on MI308 GPUs underscores the immediate financial bleed of US Department of Commerce export controls. Concurrently, NASDAQ: INTC is retreating from European expansions—pausing German and Polish greenfield fabs—to defend its domestic $3.3 billion Secure Enclave mandate. In China, SHSE: 688047 (Loongson) is weaponizing a 79.7% R&D-to-revenue ratio to migrate its 3C6000 silicon to sovereign 1Xnm nodes. This tri-polar divergence signals a structural shift: geopolitical compliance is now superseding pure unit economics, fracturing the global wafer supply chain ahead of 2026.

Figure 2025 Semiconductor Strategic Outlook: The Battle for CPU Supremacy

Unit Economics & Cash Flow Distortions

Unit Economics & Cash Flow Distortions

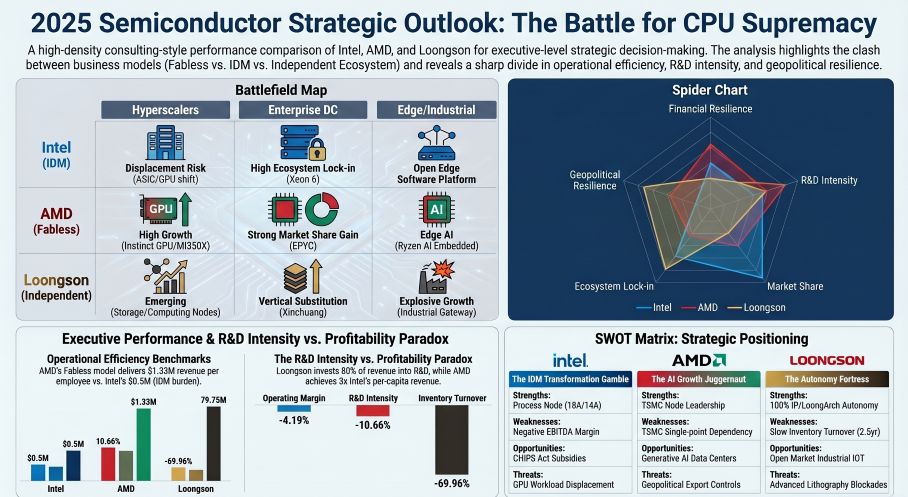

Behind the top-line revenue metrics, a forensic audit of operating leverage reveals severe sector-wide dislocations. NASDAQ: AMD exemplifies the ultimate Fabless cash-conversion vehicle, translating $34.6 billion in net revenue into $7.7 billion in operating cash flow (OCF) while commanding a pristine $1.33 million revenue-per-employee metric. However, this agility is offset by extreme balance sheet fragility: goodwill now sits at $25.1 billion (32.6% of total assets) following the $3.2 billion acquisition of ZT Systems. Any deceleration in AI infrastructure CAPEX exposes the firm to catastrophic impairment risks.

Conversely, NASDAQ: INTC is utilizing heavy IDM asset depreciation to mask core liquidity decay. While Intel reported a robust $9.6 billion in OCF against a net loss of $267 million, this is artificially shielded by $10.75 billion in D&A and a massive $950 million manufacturing asset impairment. Furthermore, Intel’s reliance on non-recourse receivables factoring to third-party institutions is a highly aggressive liquidity maneuver designed to camouflage a deteriorating cash-conversion cycle and a bloated, inefficient workforce generating barely $500,000 per head.

On the domestic substitution front, SHSE: 688047 is flashing a structural liquidity crisis. Despite a gross margin of 47%, the firm is choking on a 900-day inventory turnover cycle. Coupling a RMB 1.09 billion gross inventory overhang with a 30.6% bad debt provision on its RMB 679 million receivables indicates that Loongson’s transition from government procurement to open-market competition is stalling, resulting in trapped working capital that cannot be easily liquidated.

Comparative Resilience in a Fractured Supply Chain

Supply chain resilience is no longer measured by cost-efficiency, but by geopolitical survivability. NASDAQ: AMD operates with maximum geographic vulnerability. Its 7nm-and-below architecture, including the Ryzen 9000 and Instinct MI350X, is 100% reliant on TSMC, while backend testing is tethered to ATMP JVs (like Tongfu Microelectronics) in the Asia-Pacific. A Taiwan Strait disruption would yield an immediate, total cessation of AMD's advanced node deliveries.

NASDAQ: INTC is executing a triage strategy on its physical footprint to maintain its IDM 2.0 pivot. It is actively shrinking its geographic surface area—shifting Costa Rica operations to concentrate advanced packaging in Vietnam and Malaysia—while desperately trying to ramp the Intel 18A node using highly constrained ASML High-NA EUV equipment. Furthermore, its Intel 7 operations in Israel face uninsurable wartime business-interruption risks, forcing the company to heavily subsidize its domestic capacity via the US CHIPS Act to maintain a survivable supply baseline.

To bypass Western IP chokeholds, SHSE: 688047 is undertaking a radical "Fab-lite" integration. By discarding ARM/x86 dependencies in favor of its proprietary LoongArch instruction set, and internalizing QFN/BGA packaging via proprietary testing labs, Loongson is shortening its exposure to foreign fabrication nodes. By optimizing the microarchitecture of its LA864 cores, it is extracting 7nm-equivalent performance from trailing-edge sovereign 1Xnm/2Xnm nodes, effectively designing around the EUV embargo.

HDIN Institutional Perspective

The sector is entering a 'trough-discovery' phase. While NASDAQ: AMD signals robust top-line capture via its historic 6GW OpenAI deployment, its ballooning inventory ($7.92 billion) and heavy goodwill exposure suggest peak-cycle vulnerability. Conversely, NASDAQ: INTC is executing a defensive survival maneuver rather than a genuine turnaround; its massive fixed-cost divestitures and strategic node delays suggest IDM 2.0 is fundamentally incompatible with current demand realities. For SHSE: 688047, the 900-day inventory overhang is the ultimate red flag—state subsidies and domestic substitution mandates cannot indefinitely shield a company from basic working capital collapse. The 2H2026 margin squeeze will mercilessly punish entities carrying underutilized physical silicon assets.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Figure 2025 Semiconductor Strategic Outlook: The Battle for CPU Supremacy

Unit Economics & Cash Flow DistortionsBehind the top-line revenue metrics, a forensic audit of operating leverage reveals severe sector-wide dislocations. NASDAQ: AMD exemplifies the ultimate Fabless cash-conversion vehicle, translating $34.6 billion in net revenue into $7.7 billion in operating cash flow (OCF) while commanding a pristine $1.33 million revenue-per-employee metric. However, this agility is offset by extreme balance sheet fragility: goodwill now sits at $25.1 billion (32.6% of total assets) following the $3.2 billion acquisition of ZT Systems. Any deceleration in AI infrastructure CAPEX exposes the firm to catastrophic impairment risks.

Conversely, NASDAQ: INTC is utilizing heavy IDM asset depreciation to mask core liquidity decay. While Intel reported a robust $9.6 billion in OCF against a net loss of $267 million, this is artificially shielded by $10.75 billion in D&A and a massive $950 million manufacturing asset impairment. Furthermore, Intel’s reliance on non-recourse receivables factoring to third-party institutions is a highly aggressive liquidity maneuver designed to camouflage a deteriorating cash-conversion cycle and a bloated, inefficient workforce generating barely $500,000 per head.

On the domestic substitution front, SHSE: 688047 is flashing a structural liquidity crisis. Despite a gross margin of 47%, the firm is choking on a 900-day inventory turnover cycle. Coupling a RMB 1.09 billion gross inventory overhang with a 30.6% bad debt provision on its RMB 679 million receivables indicates that Loongson’s transition from government procurement to open-market competition is stalling, resulting in trapped working capital that cannot be easily liquidated.

Comparative Resilience in a Fractured Supply Chain

Supply chain resilience is no longer measured by cost-efficiency, but by geopolitical survivability. NASDAQ: AMD operates with maximum geographic vulnerability. Its 7nm-and-below architecture, including the Ryzen 9000 and Instinct MI350X, is 100% reliant on TSMC, while backend testing is tethered to ATMP JVs (like Tongfu Microelectronics) in the Asia-Pacific. A Taiwan Strait disruption would yield an immediate, total cessation of AMD's advanced node deliveries.

NASDAQ: INTC is executing a triage strategy on its physical footprint to maintain its IDM 2.0 pivot. It is actively shrinking its geographic surface area—shifting Costa Rica operations to concentrate advanced packaging in Vietnam and Malaysia—while desperately trying to ramp the Intel 18A node using highly constrained ASML High-NA EUV equipment. Furthermore, its Intel 7 operations in Israel face uninsurable wartime business-interruption risks, forcing the company to heavily subsidize its domestic capacity via the US CHIPS Act to maintain a survivable supply baseline.

To bypass Western IP chokeholds, SHSE: 688047 is undertaking a radical "Fab-lite" integration. By discarding ARM/x86 dependencies in favor of its proprietary LoongArch instruction set, and internalizing QFN/BGA packaging via proprietary testing labs, Loongson is shortening its exposure to foreign fabrication nodes. By optimizing the microarchitecture of its LA864 cores, it is extracting 7nm-equivalent performance from trailing-edge sovereign 1Xnm/2Xnm nodes, effectively designing around the EUV embargo.

HDIN Institutional Perspective

The sector is entering a 'trough-discovery' phase. While NASDAQ: AMD signals robust top-line capture via its historic 6GW OpenAI deployment, its ballooning inventory ($7.92 billion) and heavy goodwill exposure suggest peak-cycle vulnerability. Conversely, NASDAQ: INTC is executing a defensive survival maneuver rather than a genuine turnaround; its massive fixed-cost divestitures and strategic node delays suggest IDM 2.0 is fundamentally incompatible with current demand realities. For SHSE: 688047, the 900-day inventory overhang is the ultimate red flag—state subsidies and domestic substitution mandates cannot indefinitely shield a company from basic working capital collapse. The 2H2026 margin squeeze will mercilessly punish entities carrying underutilized physical silicon assets.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*