Global Cloud Infrastructure Super-Cycle: Alphabet, Amazon, and Alibaba Diverge on AI CapEx Realignment as Sovereign Data Mandates Define 2026 Outlook

Date : 2026-05-06

Reading : 280

Driven by the EU AI Act and US BIS export controls, the global cloud sector has entered a highly bifurcated infrastructure super-cycle. Alphabet and Amazon are absorbing massive $90B+ capital expenditures to vertically integrate proprietary silicon and secure long-term baseload power in the US. Conversely, geopolitical hardware embargoes force Alibaba and Tencent to pivot toward open-source architectures across emerging Asia-Pacific markets. This structural divergence mandates a forensic reassessment of hyperscaler free cash flow conversion, as soaring energy density constraints and European sovereign cloud mandates dictate 2026 operating leverage.

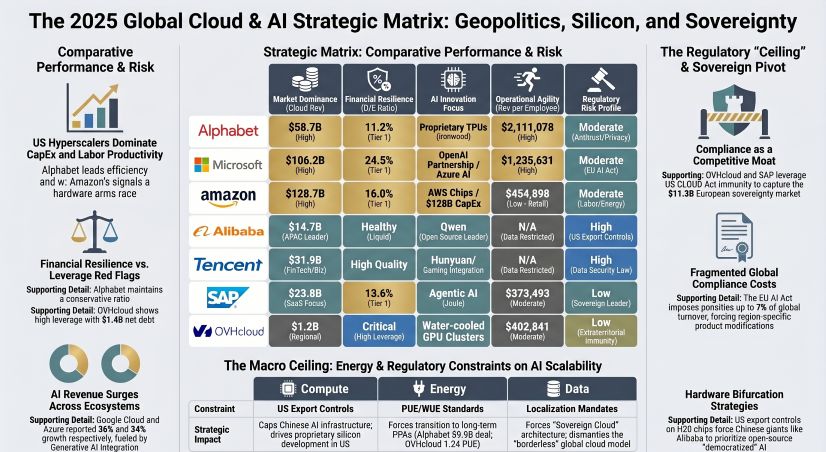

Figure The 2025 Global Cloud & Al Strategic Matrix: Geopolitics, Silicon, and Sovereignty

CapEx Super-Cycle vs. Free Cash Flow Squeeze

CapEx Super-Cycle vs. Free Cash Flow Squeeze

Beneath the headline AI revenue surges—typified by a 36% jump in Google Cloud and a 34% rise in Microsoft Azure—a stark divergence in earnings quality and free cash flow (FCF) conversion separates the software-centric platforms from physical logistics and infrastructure operators.

Tencent Holdings (HKG: 0700) currently leads the peer group with an exceptional 31.9% FCF margin, translating $27.33B in Net Income into a massive $42.35B Operating Cash Flow (OCF). This highlights a highly scalable digital ecosystem largely immune to heavy infrastructure drag. Alphabet (NASDAQ: GOOGL) exhibits unparalleled labor productivity, generating $2.11M in revenue and $676,234 in operating income per headcount. Alphabet’s robust $164.7B OCF easily absorbs its $91.4B CapEx outlay, preserving an 18.2% FCF margin despite an aggressive AI hardware build-out.

Conversely, Amazon (NASDAQ: AMZN) operates under severe capital intensity. Despite generating $716.9B in top-line revenue, Amazon’s FCF margin collapses to a razor-thin 1.6%. This margin compression is driven by a staggering $128.3B CapEx allocation and relies heavily on a Stock-Based Compensation (SBC) illusion. Amazon logged $19.47B in SBC; backing out this non-cash equity dilution pushes Amazon’s true cash flow into negative territory by over $8B. Furthermore, Amazon's forensic accounting reveals a tactical toggling of useful life estimates—reducing server depreciation schedules from 6 to 5 years, which forced a $1.4B D&A hit—suggesting aggressive earnings management to mask the raw cost of AI hardware cycles.

In Europe, OVHcloud (EPA: OVH) presents a high-risk capital structure. While posting a 5.3% FCF margin, the firm is alarmingly levered, holding just $31.9M in equity against $1.41B in net debt. Top-line metrics are further clouded by related-party transactions, with founder-controlled entities (Shadow and Qwant) accounting for roughly 2% of overall sales, raising immediate audit flags regarding revenue circularity.

Proprietary Silicon & Sovereign Energy Architectures

The commoditization of standard computing utility has ended. The new operational moats are forged through custom silicon vertical integration and hyper-localized power procurement.

US hyperscalers are actively bypassing third-party GPU bottlenecks. Alphabet is scaling its 7th-generation custom Ironwood TPUs to power the Gemini 3 multimodal architecture, while Amazon aggressively deploys proprietary AWS chips alongside NVIDIA clusters. This hardware density fundamentally alters the "macro ceiling" of grid capacity. To bypass energy gridlock, Alphabet executed a $9.9B Power Purchase Agreement (PPA) spanning 2027-2047 and acquired energy infrastructure provider Intersect for $4.8B.

Simultaneously, the geopolitical fragmentation of data privacy is creating localized fortresses. In Europe, SAP (NYSE: SAP) and OVHcloud are capturing the "AI Sovereignty" premium. SAP is migrating global enterprises via its EU AI Cloud and embedding Joule Agents directly into localized ERPs. OVHcloud leverages its immunity to the US CLOUD Act to secure government contracts, deploying offline-capable On-Prem Cloud Platforms (OPCP) for Luxembourg’s DEEP. Operationally, OVHcloud supports extreme dense-compute thermal loads using a proprietary 5th-generation direct watercooling system, achieving an industry-leading Power Usage Effectiveness (PUE) of 1.24.

Meanwhile, Alibaba (NYSE: BABA) faces a US BIS-mandated hardware embargo that caps its access to frontier GPUs like the Nvidia H100. Unable to compete on raw global compute capacity, Alibaba has executed an asymmetric supply chain pivot, open-sourcing its Qwen foundation models (surpassing 300M downloads) to build ecosystem reliance across unregulated global developer networks, heavily targeting the Asia-Pacific region.

HDIN Institutional Perspective

The sector is entering a 'trough-discovery' phase regarding CapEx efficiency. While the Street applauds double-digit top-line cloud growth, the underlying cash-conversion reality reveals an increasingly toxic reliance on equity dilution to fund physical infrastructure. Amazon’s near-zero FCF (post-SBC adjustment) signals an impending 2H2026 margin squeeze if AWS volume fails to offset the $128B CapEx weight.

Furthermore, the strategic divergence between US, European, and Chinese entities is fundamentally reshaping relative valuation. OVHcloud's "Sovereign Cloud" narrative is masking a perilous debt-to-equity ratio that leaves it highly vulnerable to Eurozone rate shocks. Concurrently, Alibaba’s open-source pivot—while strategically necessary—is less a disruptive triumph and more a forced capitulation to US export controls, permanently capping its ability to capture enterprise-grade AI monetization in Western markets. Institutional capital must rotate focus from Gross Margins toward Free Cash Flow per Share and PUE efficiency, as energy costs and regulatory fines become the primary destroyers of operating leverage.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.

Figure The 2025 Global Cloud & Al Strategic Matrix: Geopolitics, Silicon, and Sovereignty

CapEx Super-Cycle vs. Free Cash Flow SqueezeBeneath the headline AI revenue surges—typified by a 36% jump in Google Cloud and a 34% rise in Microsoft Azure—a stark divergence in earnings quality and free cash flow (FCF) conversion separates the software-centric platforms from physical logistics and infrastructure operators.

Tencent Holdings (HKG: 0700) currently leads the peer group with an exceptional 31.9% FCF margin, translating $27.33B in Net Income into a massive $42.35B Operating Cash Flow (OCF). This highlights a highly scalable digital ecosystem largely immune to heavy infrastructure drag. Alphabet (NASDAQ: GOOGL) exhibits unparalleled labor productivity, generating $2.11M in revenue and $676,234 in operating income per headcount. Alphabet’s robust $164.7B OCF easily absorbs its $91.4B CapEx outlay, preserving an 18.2% FCF margin despite an aggressive AI hardware build-out.

Conversely, Amazon (NASDAQ: AMZN) operates under severe capital intensity. Despite generating $716.9B in top-line revenue, Amazon’s FCF margin collapses to a razor-thin 1.6%. This margin compression is driven by a staggering $128.3B CapEx allocation and relies heavily on a Stock-Based Compensation (SBC) illusion. Amazon logged $19.47B in SBC; backing out this non-cash equity dilution pushes Amazon’s true cash flow into negative territory by over $8B. Furthermore, Amazon's forensic accounting reveals a tactical toggling of useful life estimates—reducing server depreciation schedules from 6 to 5 years, which forced a $1.4B D&A hit—suggesting aggressive earnings management to mask the raw cost of AI hardware cycles.

In Europe, OVHcloud (EPA: OVH) presents a high-risk capital structure. While posting a 5.3% FCF margin, the firm is alarmingly levered, holding just $31.9M in equity against $1.41B in net debt. Top-line metrics are further clouded by related-party transactions, with founder-controlled entities (Shadow and Qwant) accounting for roughly 2% of overall sales, raising immediate audit flags regarding revenue circularity.

Proprietary Silicon & Sovereign Energy Architectures

The commoditization of standard computing utility has ended. The new operational moats are forged through custom silicon vertical integration and hyper-localized power procurement.

US hyperscalers are actively bypassing third-party GPU bottlenecks. Alphabet is scaling its 7th-generation custom Ironwood TPUs to power the Gemini 3 multimodal architecture, while Amazon aggressively deploys proprietary AWS chips alongside NVIDIA clusters. This hardware density fundamentally alters the "macro ceiling" of grid capacity. To bypass energy gridlock, Alphabet executed a $9.9B Power Purchase Agreement (PPA) spanning 2027-2047 and acquired energy infrastructure provider Intersect for $4.8B.

Simultaneously, the geopolitical fragmentation of data privacy is creating localized fortresses. In Europe, SAP (NYSE: SAP) and OVHcloud are capturing the "AI Sovereignty" premium. SAP is migrating global enterprises via its EU AI Cloud and embedding Joule Agents directly into localized ERPs. OVHcloud leverages its immunity to the US CLOUD Act to secure government contracts, deploying offline-capable On-Prem Cloud Platforms (OPCP) for Luxembourg’s DEEP. Operationally, OVHcloud supports extreme dense-compute thermal loads using a proprietary 5th-generation direct watercooling system, achieving an industry-leading Power Usage Effectiveness (PUE) of 1.24.

Meanwhile, Alibaba (NYSE: BABA) faces a US BIS-mandated hardware embargo that caps its access to frontier GPUs like the Nvidia H100. Unable to compete on raw global compute capacity, Alibaba has executed an asymmetric supply chain pivot, open-sourcing its Qwen foundation models (surpassing 300M downloads) to build ecosystem reliance across unregulated global developer networks, heavily targeting the Asia-Pacific region.

HDIN Institutional Perspective

The sector is entering a 'trough-discovery' phase regarding CapEx efficiency. While the Street applauds double-digit top-line cloud growth, the underlying cash-conversion reality reveals an increasingly toxic reliance on equity dilution to fund physical infrastructure. Amazon’s near-zero FCF (post-SBC adjustment) signals an impending 2H2026 margin squeeze if AWS volume fails to offset the $128B CapEx weight.

Furthermore, the strategic divergence between US, European, and Chinese entities is fundamentally reshaping relative valuation. OVHcloud's "Sovereign Cloud" narrative is masking a perilous debt-to-equity ratio that leaves it highly vulnerable to Eurozone rate shocks. Concurrently, Alibaba’s open-source pivot—while strategically necessary—is less a disruptive triumph and more a forced capitulation to US export controls, permanently capping its ability to capture enterprise-grade AI monetization in Western markets. Institutional capital must rotate focus from Gross Margins toward Free Cash Flow per Share and PUE efficiency, as energy costs and regulatory fines become the primary destroyers of operating leverage.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.