Solid-State Battery Contraction Cycle: QuantumScape, Solid Power, and Ensurge Diverge on Capital-Light Licensing as Subsidy Cliff Defines 2026 Outlook

Date : 2026-05-06

Reading : 244

The 2025 solid-state battery landscape is entering a severe contractionary phase as the U.S. "One Big Beautiful Bill Act" accelerates the phase-out of EV tax credits. Forced into capital preservation, NYSE: QS and NASDAQ: SLDP are abandoning gigafactory ambitions for asset-light licensing models, relying on Volkswagen's PowerCo and SK On to absorb commercialization CapEx. Meanwhile, OB: ENSU faces critical insolvency at its San Jose R2R facility, underscoring a sector-wide pivot where survival dictates shifting from vertically integrated manufacturing to localized, tier-1 supply chain integration.

Figure The 2025 Solid-State Battery Divergence: Capital Survival vs Commercial Scaling

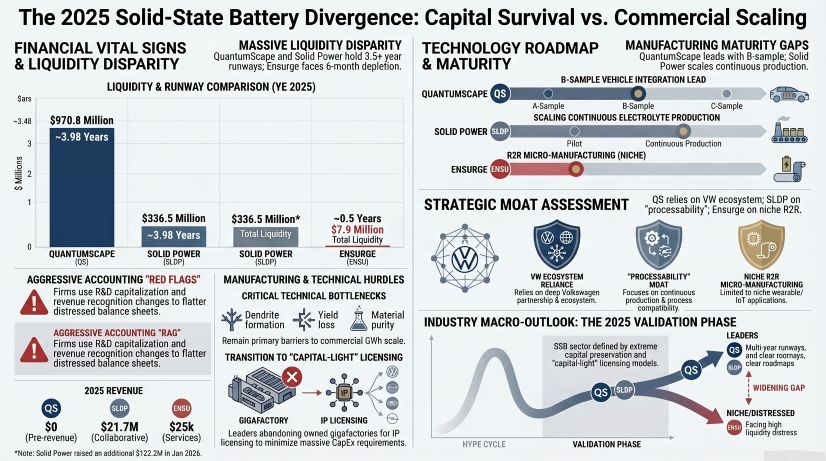

Engineering Margins and CapEx Realignment

Engineering Margins and CapEx Realignment

The sector's financial profile reveals a structural migration away from intensive capital expenditures toward subsidized technology transfer. NYSE: QS aggressively reduced its property and equipment purchases to $36.28M, anchoring its scale-up to a predefined $130M royalty prepayment framework from PowerCo. However, a forensic view of QS's accounting maneuvers—specifically logging a $19.5M capital contribution from PowerCo directly into equity rather than the P&L—artificially shields operating margins while obscuring the true commercial unit economics of the joint venture.

NASDAQ: SLDP exhibits the highest operational monetization per headcount (~$94,552), driven by a sudden shift to a "cost-to-cost" revenue recognition model. Yet, this metric is engineered through circular capital flows: SLDP paid $6.3M to its South Korean installation partner, Dahae Energy Co., Ltd., while simultaneously issuing Dahae executives 298,508 restricted stock grants. This accounting mechanism artificially pulls forward revenue recognition without confirming independent commercial scale.

On the micro-scale, OB: ENSU's path to profitability has structurally collapsed. The entity capitalized $8.94M in R&D to deflate reported operating expenses before abruptly ceasing 24/7 manufacturing operations. Saddled with a distressed $7.91M liquidity balance and a burn rate yielding a sub-6-month runway, the company is siphoning over 15% of its remaining cash to related-party consultants, flashing severe corporate governance warnings.

Comparative Resilience

As upstream supply chains fragment under escalating U.S.-China tariffs and export controls, competitive moats are strictly defined by precursor access and equipment compatibility. NASDAQ: SLDP demonstrates superior comparative resilience through its Sulfide-Based Solid Electrolyte architecture. By enabling integration into standard roll-to-roll lithium-ion equipment, SLDP drastically reduces OEM adoption barriers. However, its core vulnerability is the global commercial unavailability of the Lithium Sulfide (Li2S) precursor, forcing a capital-intensive dual-track strategy to vertically integrate synthesis in-house.

Conversely, NYSE: QS relies on a high-barrier Inorganic Ceramic Solid-State Electrolyte-Separator and an Anode-Free Architecture that fundamentally eliminates the graphite/silicon host material costs. While QS boasts an ironclad 3.48-year liquidity runway ($970.8M), it remains severely exposed to the exact same global nickel, cobalt, and lithium bottlenecks as incumbent lithium-ion producers.

OB: ENSU, despite establishing a niche moat in 1-100 mAh medical/IoT applications using ultra-thin 10 µm substrates, operates with perilous external dependency. Its reliance on Corning Incorporated for proprietary Ribbon Ceramic materials and unnamed Asian suppliers creates severe tariff vulnerabilities that it lacks the balance sheet to absorb.

HDIN Institutional Perspective

The sector is entering a 'trough-discovery' phase characterized by an illusion of commercial progress. While NYSE: QS and NASDAQ: SLDP signal B-sample maturity and continuous pilot line advancements, their asset-light pivots are defensive rather than strategic. The true systemic bottleneck is not cell chemistry, but OEM capital expenditure; with Volkswagen and Ford visibly curtailing electrification CapEx, the anticipated multi-gigawatt licensing royalties are highly vulnerable to indefinite deferment. Furthermore, the aggressive use of related-party transactions and accounting policy shifts to flatter top-line revenue suggests a failure to organically scale unit economics. The broader group faces a severe margin squeeze by 2H2026 unless localized, commercial-scale precursor supply chains materialize to offset the disappearance of federal subsidies.

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Figure The 2025 Solid-State Battery Divergence: Capital Survival vs Commercial Scaling

Engineering Margins and CapEx RealignmentThe sector's financial profile reveals a structural migration away from intensive capital expenditures toward subsidized technology transfer. NYSE: QS aggressively reduced its property and equipment purchases to $36.28M, anchoring its scale-up to a predefined $130M royalty prepayment framework from PowerCo. However, a forensic view of QS's accounting maneuvers—specifically logging a $19.5M capital contribution from PowerCo directly into equity rather than the P&L—artificially shields operating margins while obscuring the true commercial unit economics of the joint venture.

NASDAQ: SLDP exhibits the highest operational monetization per headcount (~$94,552), driven by a sudden shift to a "cost-to-cost" revenue recognition model. Yet, this metric is engineered through circular capital flows: SLDP paid $6.3M to its South Korean installation partner, Dahae Energy Co., Ltd., while simultaneously issuing Dahae executives 298,508 restricted stock grants. This accounting mechanism artificially pulls forward revenue recognition without confirming independent commercial scale.

On the micro-scale, OB: ENSU's path to profitability has structurally collapsed. The entity capitalized $8.94M in R&D to deflate reported operating expenses before abruptly ceasing 24/7 manufacturing operations. Saddled with a distressed $7.91M liquidity balance and a burn rate yielding a sub-6-month runway, the company is siphoning over 15% of its remaining cash to related-party consultants, flashing severe corporate governance warnings.

Comparative Resilience

As upstream supply chains fragment under escalating U.S.-China tariffs and export controls, competitive moats are strictly defined by precursor access and equipment compatibility. NASDAQ: SLDP demonstrates superior comparative resilience through its Sulfide-Based Solid Electrolyte architecture. By enabling integration into standard roll-to-roll lithium-ion equipment, SLDP drastically reduces OEM adoption barriers. However, its core vulnerability is the global commercial unavailability of the Lithium Sulfide (Li2S) precursor, forcing a capital-intensive dual-track strategy to vertically integrate synthesis in-house.

Conversely, NYSE: QS relies on a high-barrier Inorganic Ceramic Solid-State Electrolyte-Separator and an Anode-Free Architecture that fundamentally eliminates the graphite/silicon host material costs. While QS boasts an ironclad 3.48-year liquidity runway ($970.8M), it remains severely exposed to the exact same global nickel, cobalt, and lithium bottlenecks as incumbent lithium-ion producers.

OB: ENSU, despite establishing a niche moat in 1-100 mAh medical/IoT applications using ultra-thin 10 µm substrates, operates with perilous external dependency. Its reliance on Corning Incorporated for proprietary Ribbon Ceramic materials and unnamed Asian suppliers creates severe tariff vulnerabilities that it lacks the balance sheet to absorb.

HDIN Institutional Perspective

The sector is entering a 'trough-discovery' phase characterized by an illusion of commercial progress. While NYSE: QS and NASDAQ: SLDP signal B-sample maturity and continuous pilot line advancements, their asset-light pivots are defensive rather than strategic. The true systemic bottleneck is not cell chemistry, but OEM capital expenditure; with Volkswagen and Ford visibly curtailing electrification CapEx, the anticipated multi-gigawatt licensing royalties are highly vulnerable to indefinite deferment. Furthermore, the aggressive use of related-party transactions and accounting policy shifts to flatter top-line revenue suggests a failure to organically scale unit economics. The broader group faces a severe margin squeeze by 2H2026 unless localized, commercial-scale precursor supply chains materialize to offset the disappearance of federal subsidies.

Presentation Download: Click the PDF download link under 'Related Topics' to access the presentation of this report.

Video Link: Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*