Digital Document Software AI Supercycle: Adobe and Foxit Diverge on Capital Allocation as $28.73M AR Surge Defines 2026 Outlook

Date : 2026-05-06

Reading : 446

Adobe’s (NASDAQ: ADBE) $23.77 billion revenue engine obscures a saturated SMB moat, forcing aggressive direct AI monetization via Acrobat AI Assistant. Conversely, Foxit Software (SHSE: 688095) targets stringent data sovereignty workflows, acquiring a 51% stake in Shanghai Tongban for $38.26 million to penetrate the Chinese public sector. This highlights a bifurcated macro reality: Adobe hedges US rate volatility with $2.7 billion in SOFR swaps, while Foxit navigates localized B2G collection cycles and GDPR compliance to fuel its 49.99% top-line acceleration.

Figure Adobe vs Foxit 2025: Strategic Equilibrium & Competitive Dynamics

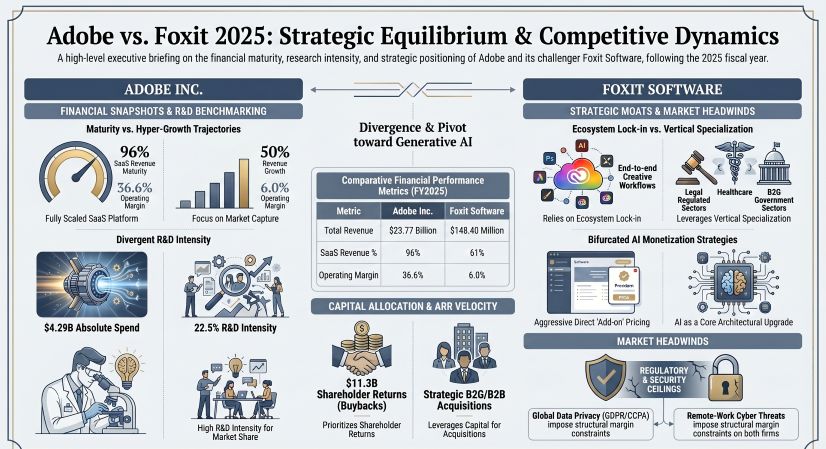

Operating Leverage and Quality of Earnings

Operating Leverage and Quality of Earnings

The 2025 fiscal data reveals a stark contrast between a hyper-scaled cash compounder and an aggressive, lower-margin vertical aggregator. Adobe operates at peak scalability, generating a 36.6% operating margin and an impregnable 34.2x interest coverage ratio (ICR) on entirely unsecured debt. The company’s $179 million CAPEX is heavily skewed toward AI server infrastructure to support its Adobe Firefly foundation models, while its staggering $10.03 billion in operating cash flow funds an $11.28 billion stock repurchase program.

Foxit’s financial posture represents a classic, high-friction SaaS transition. While top-line revenue surged 49.99% to $148.40 million (driven by its "Dual Transformation" strategy), its operating margin is suppressed at approximately 6.0%. Crucially, an analysis of Foxit's unit economics exposes deteriorating collection efficiency. While revenue grew 49.99%, Accounts Receivable (AR) ballooned by 69.88% to $28.73 million, dragging its AR Turnover down to 6.50x compared to Adobe’s 10.76x. This structural lag is directly tied to the integration of the Shanghai Tongban B2G unit, injecting elongated government procurement payment cycles into Foxit’s cash conversion cycle. Furthermore, Foxit has introduced structural balance sheet risk by leveraging a secured M&A bank loan pledged directly against its subsidiary equity—a sharp deviation from Adobe's unencumbered, SOFR-hedged capital structure.

Ecosystem Lock-In vs. Embedded Agnosticism

Adobe’s defensive moat relies on high-friction switching costs orchestrated through horizontal cloud ecosystems. Its developer monetization strategy does not sell raw PDF code; rather, it uses APIs to trigger automated enterprise marketing campaigns through Adobe GenStudio and the Adobe Experience Platform. By offering intellectual property indemnification for enterprise AI users, Adobe creates a "safe harbor" network effect that sidelines open-source alternatives.

Foxit explicitly abandons horizontal ecosystem wars to capture the foundational, bottom-up embedded developer market. Utilizing its historical contribution to the open-source PDFium project, Foxit actively monetizes its core intellectual property via the Foxit PDF SDK and OFD SDK. This architecture is ruthlessly agnostic, allowing localized deployment natively across Windows, Linux, Android, and HarmonyOS. Operationally, Foxit translates this agnostic SDK approach into highly targeted vertical moats. By deploying Intelligent Document Processing (IDP) capabilities to entities like the Beijing People's Procuratorate, Foxit turns raw PDF parsing into structured legal data extraction, satisfying stringent localized compliance mandates that horizontal competitors cannot economically address.

HDIN Institutional Perspective

The sector is entering an AI-monetization 'trough-discovery' phase. While Adobe’s aggressive strategy to extract paid AI add-on fees even from free Adobe Acrobat Reader users signals immediate top-line resilience and margin defense, Foxit’s rising AR overhang suggests a severe 2H2026 cash-conversion squeeze for the challenger. Foxit’s 49.99% top-line acceleration is undeniably impressive, but the underlying quality of earnings is deteriorating. Relying on a secured M&A bank loan tied to subsidiary equity introduces acute vulnerability to Chinese local government budget contractions. Until Foxit can align its B2G collection cycles with its SaaS deferred revenue growth, its vertical market capture remains a high-beta enterprise scale-up fraught with localized liquidity risks.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Figure Adobe vs Foxit 2025: Strategic Equilibrium & Competitive Dynamics

Operating Leverage and Quality of EarningsThe 2025 fiscal data reveals a stark contrast between a hyper-scaled cash compounder and an aggressive, lower-margin vertical aggregator. Adobe operates at peak scalability, generating a 36.6% operating margin and an impregnable 34.2x interest coverage ratio (ICR) on entirely unsecured debt. The company’s $179 million CAPEX is heavily skewed toward AI server infrastructure to support its Adobe Firefly foundation models, while its staggering $10.03 billion in operating cash flow funds an $11.28 billion stock repurchase program.

Foxit’s financial posture represents a classic, high-friction SaaS transition. While top-line revenue surged 49.99% to $148.40 million (driven by its "Dual Transformation" strategy), its operating margin is suppressed at approximately 6.0%. Crucially, an analysis of Foxit's unit economics exposes deteriorating collection efficiency. While revenue grew 49.99%, Accounts Receivable (AR) ballooned by 69.88% to $28.73 million, dragging its AR Turnover down to 6.50x compared to Adobe’s 10.76x. This structural lag is directly tied to the integration of the Shanghai Tongban B2G unit, injecting elongated government procurement payment cycles into Foxit’s cash conversion cycle. Furthermore, Foxit has introduced structural balance sheet risk by leveraging a secured M&A bank loan pledged directly against its subsidiary equity—a sharp deviation from Adobe's unencumbered, SOFR-hedged capital structure.

Ecosystem Lock-In vs. Embedded Agnosticism

Adobe’s defensive moat relies on high-friction switching costs orchestrated through horizontal cloud ecosystems. Its developer monetization strategy does not sell raw PDF code; rather, it uses APIs to trigger automated enterprise marketing campaigns through Adobe GenStudio and the Adobe Experience Platform. By offering intellectual property indemnification for enterprise AI users, Adobe creates a "safe harbor" network effect that sidelines open-source alternatives.

Foxit explicitly abandons horizontal ecosystem wars to capture the foundational, bottom-up embedded developer market. Utilizing its historical contribution to the open-source PDFium project, Foxit actively monetizes its core intellectual property via the Foxit PDF SDK and OFD SDK. This architecture is ruthlessly agnostic, allowing localized deployment natively across Windows, Linux, Android, and HarmonyOS. Operationally, Foxit translates this agnostic SDK approach into highly targeted vertical moats. By deploying Intelligent Document Processing (IDP) capabilities to entities like the Beijing People's Procuratorate, Foxit turns raw PDF parsing into structured legal data extraction, satisfying stringent localized compliance mandates that horizontal competitors cannot economically address.

HDIN Institutional Perspective

The sector is entering an AI-monetization 'trough-discovery' phase. While Adobe’s aggressive strategy to extract paid AI add-on fees even from free Adobe Acrobat Reader users signals immediate top-line resilience and margin defense, Foxit’s rising AR overhang suggests a severe 2H2026 cash-conversion squeeze for the challenger. Foxit’s 49.99% top-line acceleration is undeniably impressive, but the underlying quality of earnings is deteriorating. Relying on a secured M&A bank loan tied to subsidiary equity introduces acute vulnerability to Chinese local government budget contractions. Until Foxit can align its B2G collection cycles with its SaaS deferred revenue growth, its vertical market capture remains a high-beta enterprise scale-up fraught with localized liquidity risks.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*