Global Nutrition Trough-Discovery: Danone, Nestlé, and Regional Constituents Diverge on CapEx Realignment as Sub-8M China Births Define 2026 Outlook

Date : 2026-05-07

Reading : 298

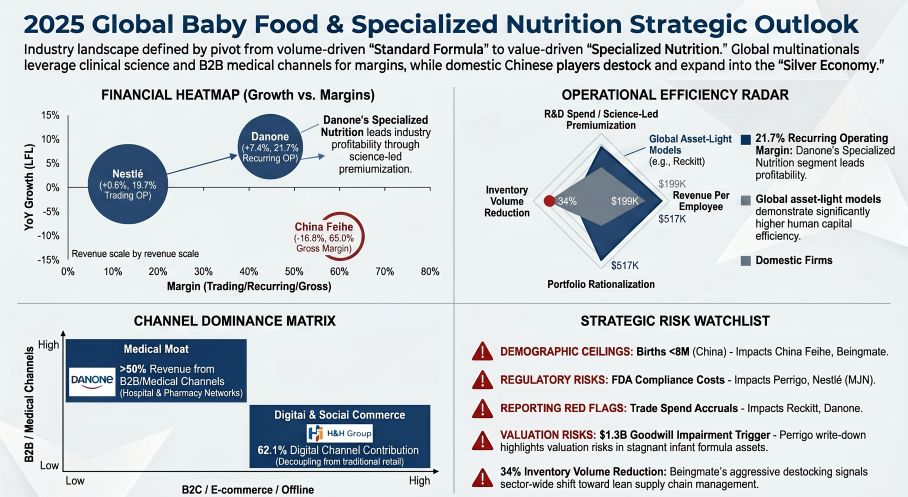

The 2025 infant nutrition sector is aggressively decoupling from standard volume growth as China’s sub-8 million birth rate acts as a terminal macro ceiling. While Danone (EPA: BN) expanded recurring operating margins to 21.7% by pivoting into B2B medical nutrition, U.S.-centric players like Perrigo (NYSE: PRGO) face acute supply chain bottlenecks, reporting massive operational losses triggered by FDA “Operation Stork Speed” compliance costs. This divergence isolates highly-levered incumbents from asset-light innovators utilizing precision fermentation and Human Milk Oligosaccharide (HMO) integration to capture premium unit economics.

Figure 2025 Global Baby Food & Specialized Nutrition Strategic Outlook

Earnings Purity and Margin Compression Profiles

Earnings Purity and Margin Compression Profiles

The optical stability of top-line revenue across the nutrition sector masks severe underlying distortions in cash-conversion cycles and asset valuation. Top-tier operators are offsetting volume losses with aggressive price/mix variance, but forensic review exposes critical earnings discrepancies.

Reckitt Benckiser (LSE: RKT) exhibits a classic red flag in earnings quality. While reporting a highly optical 20.4% adjusted operating margin, net income ($4.2B) wildly outpaced operating cash flow ($3.0B)—a divergence heavily distorted by a $1.64B non-cash gain on the disposal of its Essential Home business. Core operational yield is structurally misaligned with the reported bottom line, exacerbated by auditor warnings regarding variable executive compensation tied to highly subjective trade-spend accruals.

Conversely, Abbott Laboratories (NYSE: ABT) and Danone demonstrate fortress cash conversion. Abbott generated $9.5B in OCF against $6.5B in net income, easily absorbing $287M in restructuring charges. Danone achieved the highest peer-group unit economics (21.7% margin) through strict portfolio rationalization and integration of higher-margin acquisitions, such as Kate Farms in the U.S.

On the distressed end of the spectrum, massive delayed write-downs confirm structural value destruction. Perrigo realized $1.36B in non-cash impairments directly tied to deteriorating infant formula cash flows, whilst Hain Celestial (NASDAQ: HAIN) logged a $530.8M net loss driven by goodwill impairments across its U.S. and U.K. reporting units. Crucially, Hain disclosed a material weakness in internal controls over financial reporting regarding asset valuation, signaling that its internal discount rate and margin assumptions were fundamentally decoupled from market realities.

Capacity Rationalization and Regulatory Agility

Competitiveness in 2026 is strictly predicated on shielding supply chains from regulatory interventions and localizing advanced manufacturing.

Nestlé (SWX: NESN) leveraged its deep clinical R&D moats to offset regional volume declines, driving pricing power through the launch of *NAN Sinergity*, a proprietary blend featuring six HMOs structurally identical to breastmilk. Despite facing temporary 20-basis-point headwinds from domestic recall replenishments, its asset-light pivot allowed it to maintain a near-20% margin profile and ~USD 397K revenue-per-employee leverage.

In stark contrast to asset-light global peers, Chinese domestic market leaders rely on capital-intensive physical integration and hyper-liquidity. China Feihe (HKG: 6186) operates with a 3.0x current ratio and an interest coverage ratio (ICR) >100x. This fortress balance sheet isolates it from immediate debt pressure, acting as a direct funding mechanism for its massive offline operational moat—sustaining over 2,800 distributors and funding 700,000 face-to-face consumer seminars. Similarly, Yili (SHA: 600887) directed a $215.6M CapEx outlay into a 5G industrial internet infant formula expansion, creating a "28-Day Fresh" supply chain to outmaneuver foreign incumbents on turnaround speed.

However, channel reliance is fracturing. While China Feihe remains wedded to legacy brick-and-mortar ecosystems, H&H Group (HKG: 1112) executed a radical digital transition, capturing 82% of its adult nutrition revenue via cross-border e-commerce. Yet, H&H's heavily leveraged balance sheet (3.45x net leverage) leaves little margin for error if digital customer acquisition costs accelerate. Meanwhile, Perrigo's supply chain is actively failing; crippling compliance requirements and depressed production yields forced management to halt a planned $240M *Nutrition Network Optimization* CapEx injection, pushing the unit into strategic review.

HDIN Institutional Perspective

The global nutrition sector has officially entered a trough-discovery phase regarding standard infant formula. While management teams frequently highlight premiumization to soothe retail investors, the balance sheet data tells a story of survivalist pivots. Reckitt’s margin optically looks strong, but its structural reliance on non-recurring asset sales points to an inability to generate organic cash conversion at a sustainable rate. Conversely, the true long-term defensive alpha lies with entities like Danone. By decisively reallocating CapEx toward specialized B2B medical nutrition channels and clinical adult care, Danone is entirely immunizing its enterprise value from the structural demographic collapse currently devastating lower-tier operators.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*

Figure 2025 Global Baby Food & Specialized Nutrition Strategic Outlook

Earnings Purity and Margin Compression ProfilesThe optical stability of top-line revenue across the nutrition sector masks severe underlying distortions in cash-conversion cycles and asset valuation. Top-tier operators are offsetting volume losses with aggressive price/mix variance, but forensic review exposes critical earnings discrepancies.

Reckitt Benckiser (LSE: RKT) exhibits a classic red flag in earnings quality. While reporting a highly optical 20.4% adjusted operating margin, net income ($4.2B) wildly outpaced operating cash flow ($3.0B)—a divergence heavily distorted by a $1.64B non-cash gain on the disposal of its Essential Home business. Core operational yield is structurally misaligned with the reported bottom line, exacerbated by auditor warnings regarding variable executive compensation tied to highly subjective trade-spend accruals.

Conversely, Abbott Laboratories (NYSE: ABT) and Danone demonstrate fortress cash conversion. Abbott generated $9.5B in OCF against $6.5B in net income, easily absorbing $287M in restructuring charges. Danone achieved the highest peer-group unit economics (21.7% margin) through strict portfolio rationalization and integration of higher-margin acquisitions, such as Kate Farms in the U.S.

On the distressed end of the spectrum, massive delayed write-downs confirm structural value destruction. Perrigo realized $1.36B in non-cash impairments directly tied to deteriorating infant formula cash flows, whilst Hain Celestial (NASDAQ: HAIN) logged a $530.8M net loss driven by goodwill impairments across its U.S. and U.K. reporting units. Crucially, Hain disclosed a material weakness in internal controls over financial reporting regarding asset valuation, signaling that its internal discount rate and margin assumptions were fundamentally decoupled from market realities.

Capacity Rationalization and Regulatory Agility

Competitiveness in 2026 is strictly predicated on shielding supply chains from regulatory interventions and localizing advanced manufacturing.

Nestlé (SWX: NESN) leveraged its deep clinical R&D moats to offset regional volume declines, driving pricing power through the launch of *NAN Sinergity*, a proprietary blend featuring six HMOs structurally identical to breastmilk. Despite facing temporary 20-basis-point headwinds from domestic recall replenishments, its asset-light pivot allowed it to maintain a near-20% margin profile and ~USD 397K revenue-per-employee leverage.

In stark contrast to asset-light global peers, Chinese domestic market leaders rely on capital-intensive physical integration and hyper-liquidity. China Feihe (HKG: 6186) operates with a 3.0x current ratio and an interest coverage ratio (ICR) >100x. This fortress balance sheet isolates it from immediate debt pressure, acting as a direct funding mechanism for its massive offline operational moat—sustaining over 2,800 distributors and funding 700,000 face-to-face consumer seminars. Similarly, Yili (SHA: 600887) directed a $215.6M CapEx outlay into a 5G industrial internet infant formula expansion, creating a "28-Day Fresh" supply chain to outmaneuver foreign incumbents on turnaround speed.

However, channel reliance is fracturing. While China Feihe remains wedded to legacy brick-and-mortar ecosystems, H&H Group (HKG: 1112) executed a radical digital transition, capturing 82% of its adult nutrition revenue via cross-border e-commerce. Yet, H&H's heavily leveraged balance sheet (3.45x net leverage) leaves little margin for error if digital customer acquisition costs accelerate. Meanwhile, Perrigo's supply chain is actively failing; crippling compliance requirements and depressed production yields forced management to halt a planned $240M *Nutrition Network Optimization* CapEx injection, pushing the unit into strategic review.

HDIN Institutional Perspective

The global nutrition sector has officially entered a trough-discovery phase regarding standard infant formula. While management teams frequently highlight premiumization to soothe retail investors, the balance sheet data tells a story of survivalist pivots. Reckitt’s margin optically looks strong, but its structural reliance on non-recurring asset sales points to an inability to generate organic cash conversion at a sustainable rate. Conversely, the true long-term defensive alpha lies with entities like Danone. By decisively reallocating CapEx toward specialized B2B medical nutrition channels and clinical adult care, Danone is entirely immunizing its enterprise value from the structural demographic collapse currently devastating lower-tier operators.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards.*