Oxford Nanopore Executes $29.8M CapEx Realignment as 59.9% Clinical Revenue Surge Signals FY27 EBITDA Breakeven

Date : 2026-05-07

Reading : 108

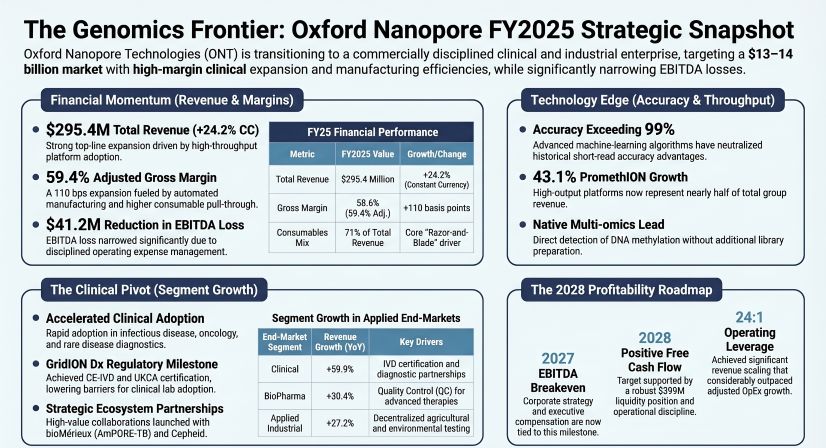

Oxford Nanopore (LSE: ONT) delivered a 24.2% constant currency revenue jump to $295.37 million in FY2025, driven by a 59.9% surge in clinical adoption. To insulate against U.S. NIH funding cuts and U.S./U.K. GPU export controls choking the China market, management executed a $29.81 million restructuring. By opening the 56,000 sq ft Spectrum facility in Abingdon and sunsetting legacy hardware, the firm is aggressively locking in high-margin clinical consumable revenues, pivoting from a cash-burning academic tool provider to a structurally profitable diagnostic enterprise.

Figure The Genomics Frontier: Oxford Nanopore FY2025 Strategic Snapshot

De-coupling Top-Line Growth from OpEx

De-coupling Top-Line Growth from OpEx

The FY25 print reveals a decisive shift in unit economics and operating leverage. While top-line revenue scaled to $295.37 million, adjusted operating expenses (OpEx) were constrained to a mere 1.0% growth. This disparity indicates the underlying business model is fundamentally decoupling from its historical cash-intensive growth phase. Adjusted EBITDA losses contracted by $41.16 million to $(114.37) million, mapping a highly credible, data-driven trajectory toward management's FY27 breakeven target.

The firm’s cash-conversion cycle is maturing rapidly. By intentionally shifting away from leasing devices (asset costs plummeted from $27.18 million to $13.32 million) to outright capital purchases, LSE: ONT has accelerated its path to free cash flow (FCF) positivity. Furthermore, the $29.81 million restructuring charge—which included the removal of 138 heads and the impairment of the ElysION automation platform—acts as a surgical "clearing of the decks." This OpEx baseline reset ensures that incremental gross profit generated by the high-throughput PromethION platforms (which saw revenues spike 43.1%) will drop directly to the bottom line in FY26.

Capturing the "Razor-and-Blade" Yield

Technologically, the moat relies on >99% basecalling accuracy and native methylation streaming. Commercially, however, the moat is solidifying via regulatory capture and supply chain verticalization. Consumables now represent a commanding 71% of total revenue. This "blade" recurring revenue is heavily protected by the rollout of the CE-IVD marked GridION Dx and assay partnerships like the AmPORE-TB test with bioMérieux. Once clinical and biomanufacturing laboratories validate workflows on locked-down hardware, the switching costs become prohibitively high.

To protect this recurring revenue from margin degradation and raw material inflation, LSE: ONT operationalized the purpose-built Spectrum facility. The deployment of next-generation automated flow cell assembly lines directly contributed 460 basis points to the 59.4% adjusted gross margin by minimizing defective yields. Paired with a strategic migration of European logistics to UPS Healthcare and a circular supply chain that recovered 61% of shipped flow cells, the firm has fundamentally insulated its unit cost structure against external supply chain shocks.

HDIN Institutional Perspective

The Street is currently underpricing LSE: ONT’s transition from an R&D-heavy hardware manufacturer to an integrated clinical diagnostics ecosystem. The strategic discontinuation of the standalone PromethION 2 Solo (P2S) proves that the incoming executive team is prioritizing return on invested capital (ROIC) and standardized clinical workflows over absolute market share accumulation in the fragmented academic space. Tying 33.3% of LTIP executive compensation directly to 2027/2028 EBITDA milestones confirms an institutional-grade alignment with shareholder equity.

However, management’s forward guidance remains highly vulnerable to macroeconomic crosscurrents in Asia. While the $399.45 million cash runway guarantees operational funding, ongoing U.S. and U.K. export controls targeting advanced AI and GPUs directly threaten the deployability of ONT’s computational hardware in China. The firm is forced into a defensive posture, deploying heavy SG&A resources toward end-user due diligence and export licensing. If this geopolitical chokehold tightens, the anticipated margin expansion in Western clinical markets may merely offset Asian revenue erosion, rather than driving the net-new EBITDA acceleration required to meet FY27 targets.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards."

Figure The Genomics Frontier: Oxford Nanopore FY2025 Strategic Snapshot

De-coupling Top-Line Growth from OpExThe FY25 print reveals a decisive shift in unit economics and operating leverage. While top-line revenue scaled to $295.37 million, adjusted operating expenses (OpEx) were constrained to a mere 1.0% growth. This disparity indicates the underlying business model is fundamentally decoupling from its historical cash-intensive growth phase. Adjusted EBITDA losses contracted by $41.16 million to $(114.37) million, mapping a highly credible, data-driven trajectory toward management's FY27 breakeven target.

The firm’s cash-conversion cycle is maturing rapidly. By intentionally shifting away from leasing devices (asset costs plummeted from $27.18 million to $13.32 million) to outright capital purchases, LSE: ONT has accelerated its path to free cash flow (FCF) positivity. Furthermore, the $29.81 million restructuring charge—which included the removal of 138 heads and the impairment of the ElysION automation platform—acts as a surgical "clearing of the decks." This OpEx baseline reset ensures that incremental gross profit generated by the high-throughput PromethION platforms (which saw revenues spike 43.1%) will drop directly to the bottom line in FY26.

Capturing the "Razor-and-Blade" Yield

Technologically, the moat relies on >99% basecalling accuracy and native methylation streaming. Commercially, however, the moat is solidifying via regulatory capture and supply chain verticalization. Consumables now represent a commanding 71% of total revenue. This "blade" recurring revenue is heavily protected by the rollout of the CE-IVD marked GridION Dx and assay partnerships like the AmPORE-TB test with bioMérieux. Once clinical and biomanufacturing laboratories validate workflows on locked-down hardware, the switching costs become prohibitively high.

To protect this recurring revenue from margin degradation and raw material inflation, LSE: ONT operationalized the purpose-built Spectrum facility. The deployment of next-generation automated flow cell assembly lines directly contributed 460 basis points to the 59.4% adjusted gross margin by minimizing defective yields. Paired with a strategic migration of European logistics to UPS Healthcare and a circular supply chain that recovered 61% of shipped flow cells, the firm has fundamentally insulated its unit cost structure against external supply chain shocks.

HDIN Institutional Perspective

The Street is currently underpricing LSE: ONT’s transition from an R&D-heavy hardware manufacturer to an integrated clinical diagnostics ecosystem. The strategic discontinuation of the standalone PromethION 2 Solo (P2S) proves that the incoming executive team is prioritizing return on invested capital (ROIC) and standardized clinical workflows over absolute market share accumulation in the fragmented academic space. Tying 33.3% of LTIP executive compensation directly to 2027/2028 EBITDA milestones confirms an institutional-grade alignment with shareholder equity.

However, management’s forward guidance remains highly vulnerable to macroeconomic crosscurrents in Asia. While the $399.45 million cash runway guarantees operational funding, ongoing U.S. and U.K. export controls targeting advanced AI and GPUs directly threaten the deployability of ONT’s computational hardware in China. The firm is forced into a defensive posture, deploying heavy SG&A resources toward end-user due diligence and export licensing. If this geopolitical chokehold tightens, the anticipated margin expansion in Western clinical markets may merely offset Asian revenue erosion, rather than driving the net-new EBITDA acceleration required to meet FY27 targets.

Presentation Download & Video Access:

Click the PDF download link under 'Related Topics' to access the presentation of this report.

Click this link to watch the YouTube video.

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for data synthesis and structural drafting, with all strategic insights and financial data verified by our editorial board to ensure professional accuracy and compliance with 2026 search standards."