BrainAurora: B2B2C Commercial Pivot Near Beijing-Tianjin-Hebei Hubs as 34.03% S&M Expense Ratio Signals Sustained Operating Leverage

Date : 2026-05-09

Reading : 66

For institutional LPs, BrainAurora’s $44.02 million FY25 net loss masks a highly efficient commercialization engine. By strictly expensing its entire $23.08 million R&D outlay, the firm strategically shields its balance sheet from future impairment while accumulating a $102.55 million tax shield to protect future margins. The 99.14% surge in active users—bolstered by its 30-province medical insurance penetration—indicates that the digital therapeutics pioneer is monetizing its B2B2C channel effectively, rendering its current optical gearing ratio a temporary artifact of SaaS-style market capture rather than structural insolvency.

Forensic Analysis of Financials & Segmental Inventory

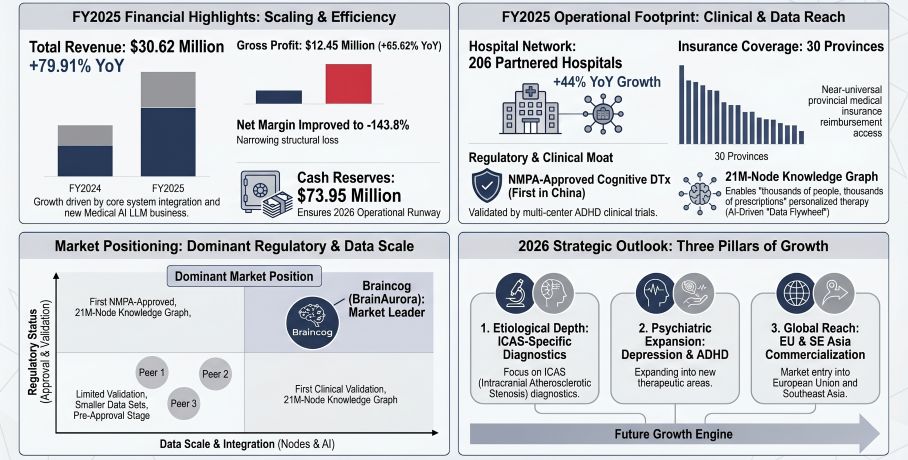

BrainAurora’s financial architecture reflects a classic Software-as-a-Medical-Device (SaMD) scaling phase. The top line exhibited aggressive acceleration, with 2025 revenue reaching $30.62 million (CNY 220.05 million), representing a 79.91% YoY increase. The divergence between accounting net profit (-$44.02 million) and actual operating cash flow (-$24.77 million) is reconciled by $19.79 million in non-cash expenses, predominantly $10.74 million in share-based compensation (SBC), $5.41 million in expected credit loss (ECL) provisions, and $3.64 million in D&A.

Figure BrainAurora 2025 Performance & 2026 Strategic Roadmap

Quantitative Inventory:

Quantitative Inventory:

* Segmental Revenue Matrix:

> In-Hospital System Integration: $15.85 million (Primary Anchor).

> Out-of-Hospital Solutions: $7.42 million (Driving B2C subscription stickiness).

> Medical AI LLM Solutions: $6.93 million (New 2025 hardware/software stream).

> Research & Other Operations: $0.43 million combined.

* Margin & Cost Dynamics: Total gross profit expanded 65.62% to $12.45 million, yielding a blended corporate gross margin of 40.7%. Sales & Marketing (S&M) expenditure grew at 55.95% to $10.42 million, notably lagging revenue growth. Consequently, S&M as a percentage of revenue compressed from 39.26% to 34.03%, signaling structural CAC dilution and expanding LTV—validated by a peak December MAU of 10,229 and 23.29 minutes of daily usage per user.

* Balance Sheet & Capital Allocation: The total asset base stands at $101.97 million, heavily anchored by $73.95 million in bank balances and cash (Current Assets constitute 90% of the total). Property, Plant, and Equipment (PPE) is minimal at $3.77 million (3.7%). R&D intensity remains high at $23.08 million (+38.92% YoY), maintaining a 0% capitalization rate.

* Capital Structure Pivot: Triggered by its January 8, 2025 listing, the automatic conversion of $39.71 million in Series A-1 preferred shares transformed the equity position from a severe -$64.56 million deficit to a positive $13.28 million. Borrowings increased to $48.15 million to fund working capital.

Supply Chain Audit & Geo-Economic Moat

The physicality of BrainAurora operates on a zero-friction distribution model, contrasting sharply with traditional pharmaceutical capital expenditure. The $5.34 million in 2025 CAPEX was strategically deployed toward data acquisitions and specialized out-of-hospital hardware.

Geographic Footprint & Commercial Architecture:

* Domestic Core Network: 100% of recognized FY25 revenue originated from Mainland China. Commercial operations are heavily entrenched in the Pearl River Delta, Beijing-Tianjin-Hebei, Sichuan, and Henan. The company expanded its formal hospital partnerships by 44.06% to 206 institutions, driving the active installation of 160 specialized cognitive centers.

* Transnational Asset Distribution: The company holds non-current assets offshore to prepare for regional expansion, specifically $1.37 million in Hong Kong and $0.26 million in Japan. Commercialization footholds are actively being secured in Singapore, Malaysia, and Macau. Crucially, its Cognitive Impairment Treatment Software has secured the EU CE mark, slating European commercialization for 2026.

* Procurement & Hardware Dependencies: The launch of the BrainAu Onebox M1 required a $6.59 million outlay in AI hardware procurement. Despite this new vector, supply chain fragility remains negligible, with the top 5 suppliers accounting for only 27.13% of total procurement (Max supplier at 9.89%).

Clinical Backlog & Temporal Markers:

* Q2 2026: Target submission for Cardiovascular Disease Cognitive Impairment registration and launch of registration clinical trials for Bone Trauma DTx.

* Q3 2027: Anticipated NMPA approval for the Dyslexia Supplementary Rehabilitation Training Software (currently stabilizing at 43 active clinical subjects).

HDIN Institutional Perspective

While optical screeners will flag BrainAurora’s 362.5% capital gearing ratio, HDIN Research views this metric as mathematically distorted by historical accumulated losses ($299 million) that artificially compress the denominator (equity). The true institutional friction point is not balance sheet solvency—supported by a 1.6x current ratio and zero reliance on government subsidies (which account for a mere $0.32 million)—but rather its working capital cycle.

The firm’s accounts receivable structure exhibits material client concentration, with Client A representing 19.64% of total revenue ($6.01 million) and 35.30% of AR, while Client B holds 18.94% of AR. This prolonged settlement cycle is a systemic feature of Chinese public hospital procurement, necessitating the $48.15 million in structural borrowings.

However, management has masterfully weaponized human capital via a highly restrictive Pre-IPO Share Award Scheme. By pricing 85.16 million reward shares at roughly $0.45 (post-split) and deferring the final 40% vesting tranche to January 2028, they have instituted a near-impenetrable retention mechanism ( evidenced by a microscopic 0.64% forfeiture rate in 2025). Coupled with proprietary algorithmic pivots—such as utilizing token-wise cross-layer entropy to eliminate AI hallucinations in the BrainAuGPT model—the company has constructed a definitive "Standard + Data" clinical moat that generic tech entrants cannot replicate.

Presentation Download & Video Access:

*Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

*Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Forensic Analysis of Financials & Segmental Inventory

BrainAurora’s financial architecture reflects a classic Software-as-a-Medical-Device (SaMD) scaling phase. The top line exhibited aggressive acceleration, with 2025 revenue reaching $30.62 million (CNY 220.05 million), representing a 79.91% YoY increase. The divergence between accounting net profit (-$44.02 million) and actual operating cash flow (-$24.77 million) is reconciled by $19.79 million in non-cash expenses, predominantly $10.74 million in share-based compensation (SBC), $5.41 million in expected credit loss (ECL) provisions, and $3.64 million in D&A.

Figure BrainAurora 2025 Performance & 2026 Strategic Roadmap

Quantitative Inventory:* Segmental Revenue Matrix:

> In-Hospital System Integration: $15.85 million (Primary Anchor).

> Out-of-Hospital Solutions: $7.42 million (Driving B2C subscription stickiness).

> Medical AI LLM Solutions: $6.93 million (New 2025 hardware/software stream).

> Research & Other Operations: $0.43 million combined.

* Margin & Cost Dynamics: Total gross profit expanded 65.62% to $12.45 million, yielding a blended corporate gross margin of 40.7%. Sales & Marketing (S&M) expenditure grew at 55.95% to $10.42 million, notably lagging revenue growth. Consequently, S&M as a percentage of revenue compressed from 39.26% to 34.03%, signaling structural CAC dilution and expanding LTV—validated by a peak December MAU of 10,229 and 23.29 minutes of daily usage per user.

* Balance Sheet & Capital Allocation: The total asset base stands at $101.97 million, heavily anchored by $73.95 million in bank balances and cash (Current Assets constitute 90% of the total). Property, Plant, and Equipment (PPE) is minimal at $3.77 million (3.7%). R&D intensity remains high at $23.08 million (+38.92% YoY), maintaining a 0% capitalization rate.

* Capital Structure Pivot: Triggered by its January 8, 2025 listing, the automatic conversion of $39.71 million in Series A-1 preferred shares transformed the equity position from a severe -$64.56 million deficit to a positive $13.28 million. Borrowings increased to $48.15 million to fund working capital.

Supply Chain Audit & Geo-Economic Moat

The physicality of BrainAurora operates on a zero-friction distribution model, contrasting sharply with traditional pharmaceutical capital expenditure. The $5.34 million in 2025 CAPEX was strategically deployed toward data acquisitions and specialized out-of-hospital hardware.

Geographic Footprint & Commercial Architecture:

* Domestic Core Network: 100% of recognized FY25 revenue originated from Mainland China. Commercial operations are heavily entrenched in the Pearl River Delta, Beijing-Tianjin-Hebei, Sichuan, and Henan. The company expanded its formal hospital partnerships by 44.06% to 206 institutions, driving the active installation of 160 specialized cognitive centers.

* Transnational Asset Distribution: The company holds non-current assets offshore to prepare for regional expansion, specifically $1.37 million in Hong Kong and $0.26 million in Japan. Commercialization footholds are actively being secured in Singapore, Malaysia, and Macau. Crucially, its Cognitive Impairment Treatment Software has secured the EU CE mark, slating European commercialization for 2026.

* Procurement & Hardware Dependencies: The launch of the BrainAu Onebox M1 required a $6.59 million outlay in AI hardware procurement. Despite this new vector, supply chain fragility remains negligible, with the top 5 suppliers accounting for only 27.13% of total procurement (Max supplier at 9.89%).

Clinical Backlog & Temporal Markers:

* Q2 2026: Target submission for Cardiovascular Disease Cognitive Impairment registration and launch of registration clinical trials for Bone Trauma DTx.

* Q3 2027: Anticipated NMPA approval for the Dyslexia Supplementary Rehabilitation Training Software (currently stabilizing at 43 active clinical subjects).

HDIN Institutional Perspective

While optical screeners will flag BrainAurora’s 362.5% capital gearing ratio, HDIN Research views this metric as mathematically distorted by historical accumulated losses ($299 million) that artificially compress the denominator (equity). The true institutional friction point is not balance sheet solvency—supported by a 1.6x current ratio and zero reliance on government subsidies (which account for a mere $0.32 million)—but rather its working capital cycle.

The firm’s accounts receivable structure exhibits material client concentration, with Client A representing 19.64% of total revenue ($6.01 million) and 35.30% of AR, while Client B holds 18.94% of AR. This prolonged settlement cycle is a systemic feature of Chinese public hospital procurement, necessitating the $48.15 million in structural borrowings.

However, management has masterfully weaponized human capital via a highly restrictive Pre-IPO Share Award Scheme. By pricing 85.16 million reward shares at roughly $0.45 (post-split) and deferring the final 40% vesting tranche to January 2028, they have instituted a near-impenetrable retention mechanism ( evidenced by a microscopic 0.64% forfeiture rate in 2025). Coupled with proprietary algorithmic pivots—such as utilizing token-wise cross-layer entropy to eliminate AI hallucinations in the BrainAuGPT model—the company has constructed a definitive "Standard + Data" clinical moat that generic tech entrants cannot replicate.

Presentation Download & Video Access:

*Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

*Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."