Sublue Ocean Science: $208M Capital Pivot Near Tianjin TEDA Hub as 45.8% Margin Signals 2026 Commercial Inflection

Date : 2026-05-09

Reading : 92

Sublue’s 2025 prospectus signals a critical transition from state-subsidized incubator to commercial hegemon. While the company reports a $1.41 million net loss, an exceptional $9.82 million operating cash flow generation proves extreme structural improvements. By leveraging a dual-engine model—premiumizing global D2C consumer hardware and securing rigid defense demand—Sublue is actively disrupting the Western duopoly held by Saab and Teledyne. For institutional LPs, the upcoming $208.73 million IPO capitalization poses severe near-term ROE dilution, yet cements the firm’s monopoly-breaking 2026 profitability mandate amid China's "Maritime Power" tailwinds.

Forensic Financials & Segmental Inventory

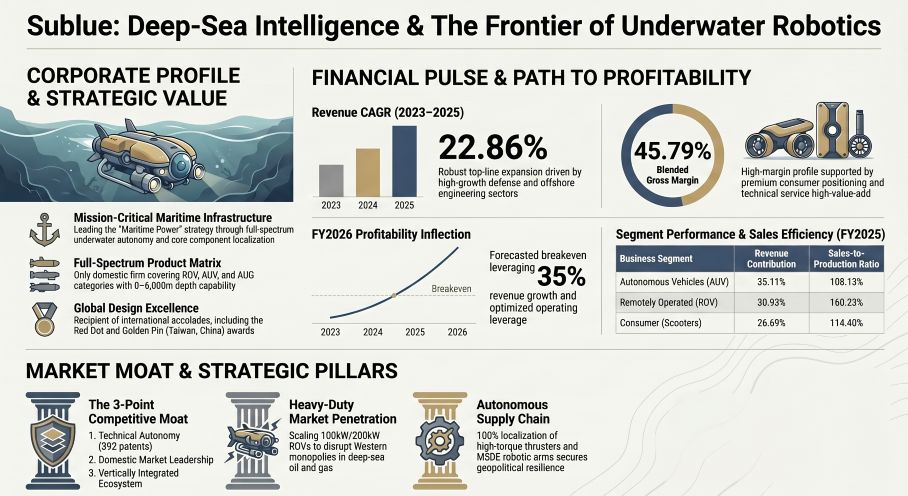

Sublue is executing a highly differentiated internal capital allocation strategy, balancing high-velocity consumer cash generation with high-barrier industrial defense engineering. In FY2025, total revenue reached $49.39 million (core business: $49.33 million), achieving a 22.86% 3-year CAGR. The blended gross margin expanded significantly to 45.79%, driven by distinct price-mix variances across its dual product engines.

Figure Sublue: Deep-Sea Intelligence & The Frontier of Underwater Robotics

Segmental Unit Economics & Margin Matrix (FY2025):

Segmental Unit Economics & Margin Matrix (FY2025):

* Autonomous Underwater Vehicles (AUV): Overtook ROVs as the largest revenue driver ($17.32 million, 35.11% of total). Sales volume hit 133 units at a premium Average Selling Price (ASP) of $117,203. Gross margins recovered to 34.36% as heavy initial R&D costs were absorbed.

* Remotely Operated Vehicles (ROV): Generated $15.26 million (30.93% of total). Moving 141 units at an ASP of $100,758, ROV gross margins expanded to 44.82% due to advancing economies of scale.

* Underwater Scooters (Consumer B2C): Yielded $13.16 million moving 18,570 units. At an ASP of $612, this segment commanded a 53.06% gross margin, capitalizing on the high-end "Vapor" series launch and optimized D2C Shopify penetration in North America and Europe.

* Technical Services: A high value-add data processing segment generating $3.59 million at an exceptional 78.48% gross margin.

Operating Leverage & Cash Conversion:

The net margin improved drastically from -39.38% (2023) to -2.86% (2025). This is heavily attributed to operating leverage; R&D expenses ($7.31 million in 2025) dropped from 25.15% to 14.79% of revenue. Crucially, the $9.82 million positive operating cash flow demonstrates aggressive working capital management—specifically, accelerated Accounts Receivable (A/R) turnover (2.63x) and a $24.88 million YoY surge in cash received from sales, effectively overriding the artificial net loss generated by non-cash depreciation and share-based compensation.

Supply Chain Audit & Geo-Economic Moat

Sublue’s physical manufacturing footprint is strategically decentralized to isolate R&D, component manufacturing, and final assembly, insulating the company against singular regional disruptions.

Geographic Base & Asset Footprint:

* TEDA, Tianjin (Headquarters): The central nervous system for consumer intelligent equipment and global B2C channel management.

* Binhai Hi-Tech Zone, Tianjin: The industrial stronghold housing *Haiyi Technology* (dedicated AUV/ROV system production) and *Nengyuan Technology* (specialized underwater robot battery R&D).

* Yazhou Bay Science City, Sanya, Hainan: The deep-sea testing outpost (*Sanya Sublue*) explicitly localized for South China Sea engineering, validating platforms like the 6,000m-depth rated *Chengsha III* AUV.

Upstream Vulnerabilities & Localization Leverage:

Sublue holds significant upstream pricing power, enforcing a strict dual-sourcing mandate. The top 5 suppliers—led by Zhuji Haiwen New Material Technology ($1.13 million) and China State Shipbuilding Corporation ($1.06 million)—account for only 18.67% of total procurement. The firm has successfully broken the Western technology blockade in mechanical and power systems, fully substituting foreign imports like the Bravo5 with its proprietary M5DE all-electric robotic arms. However, geopolitical friction remains a tangible threat: the company remains structurally dependent on a highly concentrated international oligopoly for ultra-high-end acoustic imaging sensors and precision inertial navigation systems.

HDIN Institutional Perspective

Differentiated Viewpoint: While management’s projection of achieving consolidated GAAP profitability by 2026 is mathematically supported by top-line CAGR and margin expansion, the Street must aggressively price in the "Capacity Digestion" risk inherent to the impending IPO.

Sublue is targeting a massive $208.73 million (1.50 billion CNY) capital raise—roughly double its entire FY2025 asset base ($106.80 million). With $120.33 million exclusively earmarked to transition from flexible small-batch manufacturing to large-scale industrial production in Tianjin (targeting 100kW/200kW heavy work-class ROVs), the firm will incur an immediate, severe depreciation drag. If macro demand from defense contractors (CSSC) or global offshore wind capital expenditures stalls, the resulting idle capacity will rapidly compress asset turnover (currently highly optimized at 0.46x) and exacerbate the existing -$87.60 million accumulated deficit. Sublue is trading near-term ROE for the monopolistic capability to challenge Teledyne and Saab Seaeye in the heavy-duty sector.

Presentation Download & Video Access:

* Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

* Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Forensic Financials & Segmental Inventory

Sublue is executing a highly differentiated internal capital allocation strategy, balancing high-velocity consumer cash generation with high-barrier industrial defense engineering. In FY2025, total revenue reached $49.39 million (core business: $49.33 million), achieving a 22.86% 3-year CAGR. The blended gross margin expanded significantly to 45.79%, driven by distinct price-mix variances across its dual product engines.

Figure Sublue: Deep-Sea Intelligence & The Frontier of Underwater Robotics

Segmental Unit Economics & Margin Matrix (FY2025):* Autonomous Underwater Vehicles (AUV): Overtook ROVs as the largest revenue driver ($17.32 million, 35.11% of total). Sales volume hit 133 units at a premium Average Selling Price (ASP) of $117,203. Gross margins recovered to 34.36% as heavy initial R&D costs were absorbed.

* Remotely Operated Vehicles (ROV): Generated $15.26 million (30.93% of total). Moving 141 units at an ASP of $100,758, ROV gross margins expanded to 44.82% due to advancing economies of scale.

* Underwater Scooters (Consumer B2C): Yielded $13.16 million moving 18,570 units. At an ASP of $612, this segment commanded a 53.06% gross margin, capitalizing on the high-end "Vapor" series launch and optimized D2C Shopify penetration in North America and Europe.

* Technical Services: A high value-add data processing segment generating $3.59 million at an exceptional 78.48% gross margin.

Operating Leverage & Cash Conversion:

The net margin improved drastically from -39.38% (2023) to -2.86% (2025). This is heavily attributed to operating leverage; R&D expenses ($7.31 million in 2025) dropped from 25.15% to 14.79% of revenue. Crucially, the $9.82 million positive operating cash flow demonstrates aggressive working capital management—specifically, accelerated Accounts Receivable (A/R) turnover (2.63x) and a $24.88 million YoY surge in cash received from sales, effectively overriding the artificial net loss generated by non-cash depreciation and share-based compensation.

Supply Chain Audit & Geo-Economic Moat

Sublue’s physical manufacturing footprint is strategically decentralized to isolate R&D, component manufacturing, and final assembly, insulating the company against singular regional disruptions.

Geographic Base & Asset Footprint:

* TEDA, Tianjin (Headquarters): The central nervous system for consumer intelligent equipment and global B2C channel management.

* Binhai Hi-Tech Zone, Tianjin: The industrial stronghold housing *Haiyi Technology* (dedicated AUV/ROV system production) and *Nengyuan Technology* (specialized underwater robot battery R&D).

* Yazhou Bay Science City, Sanya, Hainan: The deep-sea testing outpost (*Sanya Sublue*) explicitly localized for South China Sea engineering, validating platforms like the 6,000m-depth rated *Chengsha III* AUV.

Upstream Vulnerabilities & Localization Leverage:

Sublue holds significant upstream pricing power, enforcing a strict dual-sourcing mandate. The top 5 suppliers—led by Zhuji Haiwen New Material Technology ($1.13 million) and China State Shipbuilding Corporation ($1.06 million)—account for only 18.67% of total procurement. The firm has successfully broken the Western technology blockade in mechanical and power systems, fully substituting foreign imports like the Bravo5 with its proprietary M5DE all-electric robotic arms. However, geopolitical friction remains a tangible threat: the company remains structurally dependent on a highly concentrated international oligopoly for ultra-high-end acoustic imaging sensors and precision inertial navigation systems.

HDIN Institutional Perspective

Differentiated Viewpoint: While management’s projection of achieving consolidated GAAP profitability by 2026 is mathematically supported by top-line CAGR and margin expansion, the Street must aggressively price in the "Capacity Digestion" risk inherent to the impending IPO.

Sublue is targeting a massive $208.73 million (1.50 billion CNY) capital raise—roughly double its entire FY2025 asset base ($106.80 million). With $120.33 million exclusively earmarked to transition from flexible small-batch manufacturing to large-scale industrial production in Tianjin (targeting 100kW/200kW heavy work-class ROVs), the firm will incur an immediate, severe depreciation drag. If macro demand from defense contractors (CSSC) or global offshore wind capital expenditures stalls, the resulting idle capacity will rapidly compress asset turnover (currently highly optimized at 0.46x) and exacerbate the existing -$87.60 million accumulated deficit. Sublue is trading near-term ROE for the monopolistic capability to challenge Teledyne and Saab Seaeye in the heavy-duty sector.

Presentation Download & Video Access:

* Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

* Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."