Nano-X Imaging: Manufacturing Restructuring Near Yongin, South Korea as $40.8M Operating Cash Burn Signals Imminent Dilution Event

Date : 2026-05-09

Reading : 79

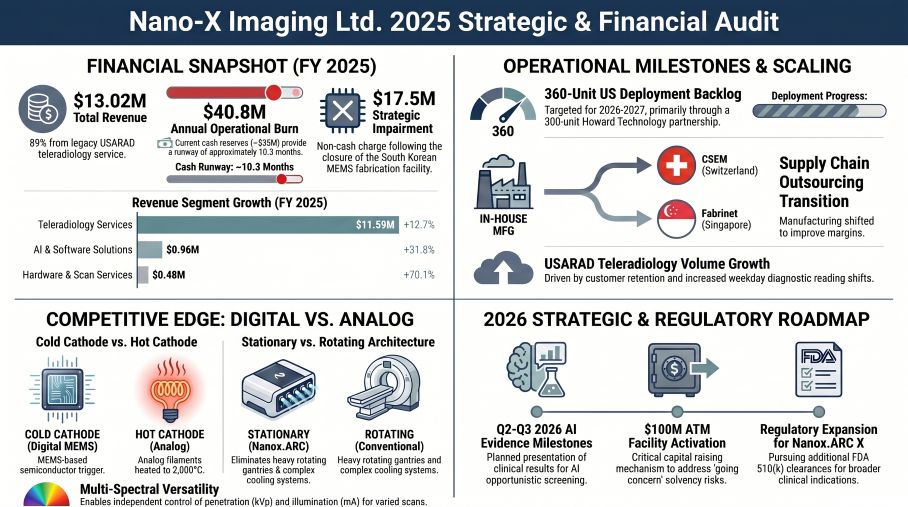

The Q4 2025 closure of Nano-X Imaging (NASDAQ: NNOX) Yongin fabrication facility marks a desperate pivot from vertical integration to outsourced survivability. While the company recorded a 15.4% top-line increase driven by legacy U.S. teleradiology, an escalating $40.8 million operational cash drain against just $35.0 million in remaining liquidity creates a fatal mismatch. For institutional LPs, the structural shift to a CapEx sales model masks severe unit economic imbalances—currently costing $1.98 to generate $1.00 in revenue. Imminent, highly dilutive capital raises are an absolute mathematical certainty.

The $1.98 Unit Economic Deficit

An audit of NASDAQ: NNOX's 2025 fiscal data reveals a severely constrained path to breakeven. Management's transition from an R&D framework to a commercial deployment model has triggered massive operating leverage deterioration. Currently, the legacy USARAD teleradiology hub accounts for the overwhelming majority of revenue, while the proprietary Nanox.ARC hardware footprint remains financially immaterial.

Figure Nano-Xlmaging Ltd 2025 Strategic & Financial Audit

Segmental & Geographic Top-Line Disaggregation:

Segmental & Geographic Top-Line Disaggregation:

* Total Revenue: $13,021,000 (+15.4% YoY from $11,283,000 in 2024).

* Geographic Concentration: United States operations generated 98% ($12,760,000); Rest of World (Europe, Asia, etc.) accounted for just 2% ($260,000). The filings specifically omit explicit revenue data for Taiwan, Province of China, and the broader Chinese market due to UN compliance constraints and U.S.-China tariff exposures.

* Teleradiology Services: $11,585,000 (+12.7% YoY / +$1.3M). Supported by a network of ~20 radiologists serving ~100 customers across 200 facilities.

* AI and Software Solutions (Nanox.AI & Nanox Health IT): $958,000 (+31.8% YoY). Growth includes a $382,000 post-acquisition contribution following the November 2025 purchase of Nanox Health IT (formerly Vaso Healthcare IT Corp.).

* Hardware and Scan Services (Nanox.ARC & Nanox.CONNECT): $478,000 (+70.1% YoY).

Margin Compression & Cost Containment Metrics:

* Cost of Revenue (CoR): $25,809,000 (+17.9% YoY), far outpacing top-line growth and resulting in a $1.98 expenditure for every $1.00 of recognized revenue.

* Gross Loss: $(12,788,000), representing a 20.5% YoY deterioration.

* R&D Expenses: $19,236,000 (-4.7% YoY). Core base salaries rose to $11.2M, offset by a $1.3M reduction in share-based compensation (SBC) and a $1.5M decrease in direct materials as Nanox.ARC cleared regulatory hurdles.

* Sales & Marketing (S&M): $5,665,000 (+66.1% YoY). Driven by a $2.6M spike in marketing to support CapEx distribution partnerships.

* General & Administrative (G&A): $21,587,000 (-3.9% YoY). Savings realized via a $1.0M drop in legal fees (following SEC settlements) and a $0.6M reduction in D&O insurance premiums.

* Impairment of Long-Lived Assets: $17,528,000 non-cash charge directly tied to the South Korean MEMS fab closure.

Cash Conversion & Runway Solvency:

* Operating Loss: $(78,234,000) (+37.9% YoY).

* Net Loss (GAAP): $(75,018,000) (+40.2% YoY).

* Non-GAAP Reconciliations: Adjusting the GAAP net loss for $33.4M in non-cash items—including the $17.528M fab impairment, $10.508M legacy M&A amortization, $4.190M SBC, $1.189M depreciation, $(1.972M) in minor items, and $2.782M from working capital optimization—yields a Proxy Non-GAAP Adjusted Loss of $(43,575,000).

* Operating Cash Burn: $(40,793,000) (+11.5% YoY).

* Liquidity Position: Total liquid assets were $60.0 million on Dec 31, 2025, but dwindled to a preliminary $35.0 million by the report's issuance date.

* Runway Assessment: With a ~10.3-month cash runway, auditors have formally issued a "Going Concern" qualification. Management estimates only $0.5 million in cash restructuring charges remain for 2026, meaning the true liquidity drain is pure operational burn.

The Global Outsourcing Pivot

The physical reality of NASDAQ: NNOX's operations is undergoing a violent restructuring to preserve capital. The strategic abandonment of vertical integration introduces acute single-source geographic dependencies.

* The Yongin Shutdown (South Korea): The closure of the proprietary MEMS X-ray chip fabrication line in Gyeonggi province unwinds the legacy operational relationship with SK Telecom. Remaining operations here are downsized strictly to R&D and X-ray tube production.

* The Swiss Bottleneck (Switzerland): Primary MEMS chip production is migrating to the Swiss Center for Electronics and Microtechnology (CSEM). By mid-2026, the delivery of hundreds of production-level chips from this foundry will dictate the viability of the entire hardware backlog.

* The Assembly Hub (Singapore): Scalable manufacturing of the FDA 510(k)-cleared (April 2025) Nanox.ARC X system is entirely outsourced to Fabrinet via an August 2025 Volume Supply Agreement.

* X-Ray Tube Production (Italy & USA): Tube supply is diversified between SKAN-X Radiology Devices SRL (CEI) in Bologna, Italy (a Dec 2024 Preferred Supplier Agreement), and Varex Imaging Corporation in the U.S. (operating under a revenue-sharing model based on global pay-per-scan yields).

* Headquarters & Geopolitical Threat (Israel): Petach Tikva houses the global HQ and $13.14 million in long-lived assets. Ongoing hostilities—escalating into direct ballistic exchanges with Iran during the June 2025 "Twelve-Day War" and again in Feb/April 2026—have forced the company to maintain vital emitter inventory stockpiles outside of Israel as a geopolitical hedge.

* Commercial Hardware Deployment (USA): U.S. bases include the USARAD teleradiology hub in Florida and corporate offices in New Jersey. Operationally, only ~36 Nanox.ARC systems are in deployment, with 17 additional units slated under the Nanox Imaging Network (NIN) with Monarch Medical Management. Management claims a contracted backlog of 360 CapEx systems over 2-3 years (including 300 units via Howard Technology Solutions). Furthermore, AI opportunistic screening trial results are slated for Summer 2026, following the rollout of the TAP2D cloud enhancement in February 2026.

Corporate Governance, Litigation, & IP Defensibility

A Forensic Analysis of the corporate governance structure reveals substantial cash retention for executives despite the ongoing solvency crisis, alongside a highly fragmented IP and litigation landscape.

* Executive Compensation: CEO Erez Meltzer (who acts in a dual CEO/Chairman capacity) received total 2025 compensation of $2,094,689 ($900,000 base, $310,662 benefits, $771,707 in 4-year vesting equity, and a $112,500 cash bonus). CFO Ran Daniel will exit on July 31, 2026, to be replaced by Guy Nathanzon.

* IP Portfolio Audit: The "cold cathode" moat is protected by 48 granted patents (31 US, 5 Israel, 3 EPO, 3 China, 3 South Korea, 2 Hong Kong, 1 Germany) and 12 pending applications (7 US, 4 EPO, 1 Israel). The portfolio also holds 25 global trademarks. However, core patents expire tightly between 2032 and 2041, and software architecture relies heavily on non-exclusive third-party licenses via Nanox.CLOUD.

* Litigation & Malpractice Liabilities: The company is settling legacy SEC penalties ($650,000 corporate; $150,000 for the late Chairman Ran Poliakine) and executed an April 2026 settlement issuing 450,000 ordinary shares to resolve a December 2025 asset transaction dispute. A cross-border jurisdictional dispute involving a 2015 agreement with "Nanox Gibraltar PLC" generated active court motions in Feb 2026. Simultaneously, USARAD faces escalating medical malpractice lawsuits across Edgar County (IL), St. Lawrence County (NY), Philadelphia (PA), and Okaloosa County (FL).

* Data Regulation Chokeholds: Nanox.AI faces severe 2025/2026 compliance headwinds from the US DOJ "Final Rule" on health data (auditing required by Oct 2025), the EU AI Act (penalties up to €35M or 7% turnover), the EU Data Act (Sept 2025), and Israel's PPL Amendment 13 (Aug 2025).

HDIN Institutional Perspective

While management touts a pipeline of 360 contracted systems and the "software-first" transition of its AI portfolio (HealthFLD, HealthCCSng V2.0, HealthOST, and the upcoming ARC.AI), HDIN Research views the 2025/2026 narrative as fundamentally misaligned with its unit economics.

The strategic pivot to a U.S. Capital Expenditure (CapEx) model actively contradicts the original Medical Software as a Service (MSaaS) "pay-per-scan" thesis. By transferring hardware upfront, the company mitigates placement costs but subjects itself to grueling hospital procurement cycles and structurally lower gross margins inherent in the newly acquired IT reseller business. With an active going concern warning, $40.8 million in operational cash burn, and just 36 units deployed, the structural reality is that NASDAQ: NNOX is a traditional, hardware-intensive enterprise running out of time. The street has not fully priced in the operational friction of migrating core MEMS chip production to Switzerland amidst active Middle Eastern warfare.

Presentation Download & Video Access:

* Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

* Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

The $1.98 Unit Economic Deficit

An audit of NASDAQ: NNOX's 2025 fiscal data reveals a severely constrained path to breakeven. Management's transition from an R&D framework to a commercial deployment model has triggered massive operating leverage deterioration. Currently, the legacy USARAD teleradiology hub accounts for the overwhelming majority of revenue, while the proprietary Nanox.ARC hardware footprint remains financially immaterial.

Figure Nano-Xlmaging Ltd 2025 Strategic & Financial Audit

Segmental & Geographic Top-Line Disaggregation:* Total Revenue: $13,021,000 (+15.4% YoY from $11,283,000 in 2024).

* Geographic Concentration: United States operations generated 98% ($12,760,000); Rest of World (Europe, Asia, etc.) accounted for just 2% ($260,000). The filings specifically omit explicit revenue data for Taiwan, Province of China, and the broader Chinese market due to UN compliance constraints and U.S.-China tariff exposures.

* Teleradiology Services: $11,585,000 (+12.7% YoY / +$1.3M). Supported by a network of ~20 radiologists serving ~100 customers across 200 facilities.

* AI and Software Solutions (Nanox.AI & Nanox Health IT): $958,000 (+31.8% YoY). Growth includes a $382,000 post-acquisition contribution following the November 2025 purchase of Nanox Health IT (formerly Vaso Healthcare IT Corp.).

* Hardware and Scan Services (Nanox.ARC & Nanox.CONNECT): $478,000 (+70.1% YoY).

Margin Compression & Cost Containment Metrics:

* Cost of Revenue (CoR): $25,809,000 (+17.9% YoY), far outpacing top-line growth and resulting in a $1.98 expenditure for every $1.00 of recognized revenue.

* Gross Loss: $(12,788,000), representing a 20.5% YoY deterioration.

* R&D Expenses: $19,236,000 (-4.7% YoY). Core base salaries rose to $11.2M, offset by a $1.3M reduction in share-based compensation (SBC) and a $1.5M decrease in direct materials as Nanox.ARC cleared regulatory hurdles.

* Sales & Marketing (S&M): $5,665,000 (+66.1% YoY). Driven by a $2.6M spike in marketing to support CapEx distribution partnerships.

* General & Administrative (G&A): $21,587,000 (-3.9% YoY). Savings realized via a $1.0M drop in legal fees (following SEC settlements) and a $0.6M reduction in D&O insurance premiums.

* Impairment of Long-Lived Assets: $17,528,000 non-cash charge directly tied to the South Korean MEMS fab closure.

Cash Conversion & Runway Solvency:

* Operating Loss: $(78,234,000) (+37.9% YoY).

* Net Loss (GAAP): $(75,018,000) (+40.2% YoY).

* Non-GAAP Reconciliations: Adjusting the GAAP net loss for $33.4M in non-cash items—including the $17.528M fab impairment, $10.508M legacy M&A amortization, $4.190M SBC, $1.189M depreciation, $(1.972M) in minor items, and $2.782M from working capital optimization—yields a Proxy Non-GAAP Adjusted Loss of $(43,575,000).

* Operating Cash Burn: $(40,793,000) (+11.5% YoY).

* Liquidity Position: Total liquid assets were $60.0 million on Dec 31, 2025, but dwindled to a preliminary $35.0 million by the report's issuance date.

* Runway Assessment: With a ~10.3-month cash runway, auditors have formally issued a "Going Concern" qualification. Management estimates only $0.5 million in cash restructuring charges remain for 2026, meaning the true liquidity drain is pure operational burn.

The Global Outsourcing Pivot

The physical reality of NASDAQ: NNOX's operations is undergoing a violent restructuring to preserve capital. The strategic abandonment of vertical integration introduces acute single-source geographic dependencies.

* The Yongin Shutdown (South Korea): The closure of the proprietary MEMS X-ray chip fabrication line in Gyeonggi province unwinds the legacy operational relationship with SK Telecom. Remaining operations here are downsized strictly to R&D and X-ray tube production.

* The Swiss Bottleneck (Switzerland): Primary MEMS chip production is migrating to the Swiss Center for Electronics and Microtechnology (CSEM). By mid-2026, the delivery of hundreds of production-level chips from this foundry will dictate the viability of the entire hardware backlog.

* The Assembly Hub (Singapore): Scalable manufacturing of the FDA 510(k)-cleared (April 2025) Nanox.ARC X system is entirely outsourced to Fabrinet via an August 2025 Volume Supply Agreement.

* X-Ray Tube Production (Italy & USA): Tube supply is diversified between SKAN-X Radiology Devices SRL (CEI) in Bologna, Italy (a Dec 2024 Preferred Supplier Agreement), and Varex Imaging Corporation in the U.S. (operating under a revenue-sharing model based on global pay-per-scan yields).

* Headquarters & Geopolitical Threat (Israel): Petach Tikva houses the global HQ and $13.14 million in long-lived assets. Ongoing hostilities—escalating into direct ballistic exchanges with Iran during the June 2025 "Twelve-Day War" and again in Feb/April 2026—have forced the company to maintain vital emitter inventory stockpiles outside of Israel as a geopolitical hedge.

* Commercial Hardware Deployment (USA): U.S. bases include the USARAD teleradiology hub in Florida and corporate offices in New Jersey. Operationally, only ~36 Nanox.ARC systems are in deployment, with 17 additional units slated under the Nanox Imaging Network (NIN) with Monarch Medical Management. Management claims a contracted backlog of 360 CapEx systems over 2-3 years (including 300 units via Howard Technology Solutions). Furthermore, AI opportunistic screening trial results are slated for Summer 2026, following the rollout of the TAP2D cloud enhancement in February 2026.

Corporate Governance, Litigation, & IP Defensibility

A Forensic Analysis of the corporate governance structure reveals substantial cash retention for executives despite the ongoing solvency crisis, alongside a highly fragmented IP and litigation landscape.

* Executive Compensation: CEO Erez Meltzer (who acts in a dual CEO/Chairman capacity) received total 2025 compensation of $2,094,689 ($900,000 base, $310,662 benefits, $771,707 in 4-year vesting equity, and a $112,500 cash bonus). CFO Ran Daniel will exit on July 31, 2026, to be replaced by Guy Nathanzon.

* IP Portfolio Audit: The "cold cathode" moat is protected by 48 granted patents (31 US, 5 Israel, 3 EPO, 3 China, 3 South Korea, 2 Hong Kong, 1 Germany) and 12 pending applications (7 US, 4 EPO, 1 Israel). The portfolio also holds 25 global trademarks. However, core patents expire tightly between 2032 and 2041, and software architecture relies heavily on non-exclusive third-party licenses via Nanox.CLOUD.

* Litigation & Malpractice Liabilities: The company is settling legacy SEC penalties ($650,000 corporate; $150,000 for the late Chairman Ran Poliakine) and executed an April 2026 settlement issuing 450,000 ordinary shares to resolve a December 2025 asset transaction dispute. A cross-border jurisdictional dispute involving a 2015 agreement with "Nanox Gibraltar PLC" generated active court motions in Feb 2026. Simultaneously, USARAD faces escalating medical malpractice lawsuits across Edgar County (IL), St. Lawrence County (NY), Philadelphia (PA), and Okaloosa County (FL).

* Data Regulation Chokeholds: Nanox.AI faces severe 2025/2026 compliance headwinds from the US DOJ "Final Rule" on health data (auditing required by Oct 2025), the EU AI Act (penalties up to €35M or 7% turnover), the EU Data Act (Sept 2025), and Israel's PPL Amendment 13 (Aug 2025).

HDIN Institutional Perspective

While management touts a pipeline of 360 contracted systems and the "software-first" transition of its AI portfolio (HealthFLD, HealthCCSng V2.0, HealthOST, and the upcoming ARC.AI), HDIN Research views the 2025/2026 narrative as fundamentally misaligned with its unit economics.

The strategic pivot to a U.S. Capital Expenditure (CapEx) model actively contradicts the original Medical Software as a Service (MSaaS) "pay-per-scan" thesis. By transferring hardware upfront, the company mitigates placement costs but subjects itself to grueling hospital procurement cycles and structurally lower gross margins inherent in the newly acquired IT reseller business. With an active going concern warning, $40.8 million in operational cash burn, and just 36 units deployed, the structural reality is that NASDAQ: NNOX is a traditional, hardware-intensive enterprise running out of time. The street has not fully priced in the operational friction of migrating core MEMS chip production to Switzerland amidst active Middle Eastern warfare.

Presentation Download & Video Access:

* Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

* Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."