RadRock: Fab-Lite Pivot Near Chongqing MEMS Device Production Base as 30.63% Cost Reduction Signals 2028 Breakeven Path

Date : 2026-05-11

Reading : 121

RadRock investment thesis hinges on its brutal, capital-intensive transition from a Fabless to a Fab-lite model. By localizing SAW/TC-SAW/ML-SAW filter production at its Chongqing MEMS Device Production Base, the company aims to break the Skyworks/Qorvo monopoly on high-integration 5G architectures. While a recent $78.61M state-backed debt-to-equity swap neutralized immediate solvency crises, a severe -$39.28M FY25 operating cash bleed underscores structural working capital friction. The firm’s survival depends on scaling its L-PAMiD pipeline to outpace rapid inventory obsolescence and geopolitical EDA/lithography bottlenecks ahead of its projected 2028 breakeven.

Forensic Analysis: Margin Compression vs. CAPEX Dilution

RadRock is navigating a severe profitability trough driven by aggressive price-mix variances and capacity ramp-up friction. While top-line revenue demonstrates a 15.04% CAGR, operating leverage is non-existent due to heavy initial depreciation and predatory pricing in commoditized 4G segments.

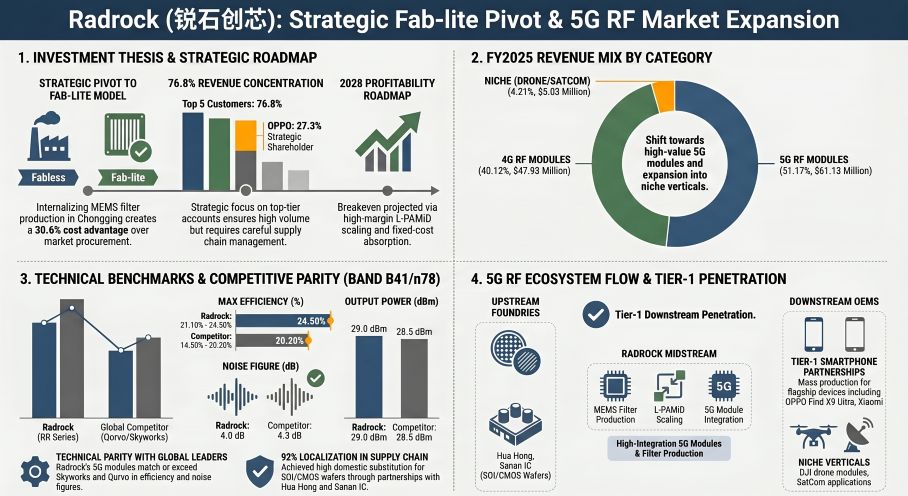

Figure Radrock: Strategic Fab-lite Pivot & 5G RF Market Expansion

Entity & Technological Index:

Entity & Technological Index:

* Proprietary Technologies: L-PAMiD (Phase 8M/8L NSA), L-PAMiF, DiFEM, 3D printed cavity formation technology (sub-150μm thickness).

* Key Network: OPPO, Sanan IC, Hua Hong Semiconductor, ASML, Skyworks.

Table Quantitative Inventory & Segmental Unit Economics (FY23–FY25)

Segmental Architecture & Operating Volumes:

* Price-Mix Erosion: 5G unit prices plummeted from $0.43 to $0.30, a strategic penetration pricing maneuver. Despite this, total 5G revenue hit $61.13M (51.17% of total), while 4G contributed $47.93M (40.12%). Emerging verticals contributed marginally: Discrete ($5.37M, 4.50%), Drone ($4.55M, 3.81%), and Satellite/NTN ($0.48M, 0.40%).

* Production vs. Absorption: FY25 total production volume hit 926.07M units with a sales volume of 844.07M (91.14% Production-to-Sales ratio).

* Internal Capital Allocation (IPO Proceeds): The $112.61M planned IPO is structurally partitioned: $51.37M (45.6%) for the Chongqing MEMS Phase II Project, $45.94M (40.8%) for R&D, and $15.30M (13.6%) for working capital.

* R&D-to-Moat Translation: R&D expenses hit $29.14M in FY25 (24.38% of revenue). Excluding SBC, core R&D intensity is 22.60%, outstripping the 20.14% peer average. The 247-person R&D team (59.52% of workforce) supports 382 patents with lifecycles spanning 2038 to 2044.

Geo-Economic Moat & Supply Chain Physicality: The Chongqing-Shanghai Axis

RadRock operates a heavily localized yet technically vulnerable physical footprint, bridging domestic foundries with overseas equipment dependencies.

* The Physical Manufacturing Base: The strategic anchor is the Chongqing MEMS Device Production Base (Total Assets: $91.73M, FY25 Revenue: $38.01M), executing the Fab-lite transition. R&D nodes operate in the Shanghai R&D Center (Assets: $22.07M) and Chengdu R&D Center (Assets: $2.31M), while the Shenzhen Sales & R&D Center ($5.01M paid-in capital) anchors Southern China tech hubs. Hong Kong (Assets: $11.42M) serves as the primary overseas logistics/settlement conduit handling 40.40% ($48.27M) of FY25 global revenues.

* Supplier Concentration & Upstream Leverage: Top-5 suppliers control 58.66% ($76.97M) of procurement. Hua Hong Semiconductor dominates SOI wafers ($26.71M, 20.35%), while Sanan IC commands GaAs procurement ($21.28M, 16.22%). OSAT partners include Xinde Semiconductor ($13.81M) and Yongsil ($6.63M). Despite domestic substitution reaching 68.37% (GaAs) and 92.09% (SOI), reliance on AWSC, GlobalFoundries, X-FAB, TSMC, and Win Semiconductors persists.

* Geopolitical Friction Points: The firm openly discloses critical dependencies on imported ASML lithography machinery for the MEMS Phase II build-out, alongside an absolute reliance on Western EDA software. Any tightening of export controls would freeze capacity expansion.

* Downstream Concentration: Client architecture is dangerously concentrated. The Top-5 customers account for 76.81% ($91.81M) of FY25 revenue. Distributors SAC (Pinjia), Hangxin, Damai, and Pinchuang represent $59.14M combined. Crucially, OPPO stands as the largest direct client ($32.67M, 27.33% of revenue) and a related-party shareholder (5.9431% equity), driving 58.69% of core gross profit.

HDIN Institutional Perspective: The Critical Edge

While management asserts that integrating the Chongqing MEMS facility generates a 30.63% cost reduction on proprietary filters—paving a theoretical path to a 2028 breakeven—HDIN Research assigns a high margin-of-error to this timeline.

Our sensitivity analysis reveals severe structural fragility: a mere 10% decrease in Average Selling Price (ASP) erodes net profit by $11.95M, completely obliterating the current 9.57% gross margin layer and pushing unit economics into negative territory. Conversely, a 10% raw material cost inflation only degrades the bottom line by $7.31M. This confirms that STAR: RadRock suffers from a chronic pricing-power deficit, not just a cost-containment issue. Furthermore, internal control audits flag prior-period restatements (a 1.02% adjustment to FY24 management fees) and a $1.65M non-operating fund occupation by Founder Ni Jianxing (subsequently repaid with interest to total $1.67M). Coupled with OPPO’s dual leverage as a massive 27.33% revenue contributor and strategic shareholder, the Street is structurally underpricing the risk of perpetual gross-margin suppression as OEMs squeeze suppliers to protect their own hardware margins.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Forensic Analysis: Margin Compression vs. CAPEX Dilution

RadRock is navigating a severe profitability trough driven by aggressive price-mix variances and capacity ramp-up friction. While top-line revenue demonstrates a 15.04% CAGR, operating leverage is non-existent due to heavy initial depreciation and predatory pricing in commoditized 4G segments.

Figure Radrock: Strategic Fab-lite Pivot & 5G RF Market Expansion

Entity & Technological Index:* Proprietary Technologies: L-PAMiD (Phase 8M/8L NSA), L-PAMiF, DiFEM, 3D printed cavity formation technology (sub-150μm thickness).

* Key Network: OPPO, Sanan IC, Hua Hong Semiconductor, ASML, Skyworks.

Table Quantitative Inventory & Segmental Unit Economics (FY23–FY25)

| Financial Metric | FY23 | FY24 | FY25 | Variance / Notes |

|---|---|---|---|---|

| Top-Line Revenue | $90.31M | $93.02M | $119.53M | Driven by 5G volume expansion. FY25: CNY 859.14M. |

| Core Gross Margin | 13.90% | 8.78% | 9.57% | Peer average stands at 19.80%. 5G FY25 GM: 14.24%; 4G GM: 5.58%. |

| Net Profit | -$45.67M | -$49.11M | -$41.10M | Accumulated unrecovered deficit reached -$251.75M. |

| Operating Cash Flow | -$30.86M | -$36.39M | -$39.28M | Widening gap vs. net loss driven by $22.76M FY25 inventory cash drain. |

| SBC Non-Cash Expense | $15.40M | $2.16M | $3.62M | ESOP mandates a 36-month post-IPO lock-up with punitive clawbacks. |

| AR & Inventory Turnover | AR: 28.31x / Inv: 1.98x | AR: 11.18x / Inv: 1.58x | AR: 8.74x / Inv: 1.61x | Credit terms extended to 60 days via direct OEM sales pivot. |

| Inventory & Provisioning | Provision: 22.71% | Provision: 27.14% | Provision: 22.77% | FY25 inventory reached $56.54M, with $16.67M provisioned for devaluation. |

| Solvency (Debt-to-Equity) | N/A | 9.43x | 1.21x | Asset-liability ratio declined from 90.41% to 54.71% through a $78.61M debt-equity swap. |

* Price-Mix Erosion: 5G unit prices plummeted from $0.43 to $0.30, a strategic penetration pricing maneuver. Despite this, total 5G revenue hit $61.13M (51.17% of total), while 4G contributed $47.93M (40.12%). Emerging verticals contributed marginally: Discrete ($5.37M, 4.50%), Drone ($4.55M, 3.81%), and Satellite/NTN ($0.48M, 0.40%).

* Production vs. Absorption: FY25 total production volume hit 926.07M units with a sales volume of 844.07M (91.14% Production-to-Sales ratio).

* Internal Capital Allocation (IPO Proceeds): The $112.61M planned IPO is structurally partitioned: $51.37M (45.6%) for the Chongqing MEMS Phase II Project, $45.94M (40.8%) for R&D, and $15.30M (13.6%) for working capital.

* R&D-to-Moat Translation: R&D expenses hit $29.14M in FY25 (24.38% of revenue). Excluding SBC, core R&D intensity is 22.60%, outstripping the 20.14% peer average. The 247-person R&D team (59.52% of workforce) supports 382 patents with lifecycles spanning 2038 to 2044.

Geo-Economic Moat & Supply Chain Physicality: The Chongqing-Shanghai Axis

RadRock operates a heavily localized yet technically vulnerable physical footprint, bridging domestic foundries with overseas equipment dependencies.

* The Physical Manufacturing Base: The strategic anchor is the Chongqing MEMS Device Production Base (Total Assets: $91.73M, FY25 Revenue: $38.01M), executing the Fab-lite transition. R&D nodes operate in the Shanghai R&D Center (Assets: $22.07M) and Chengdu R&D Center (Assets: $2.31M), while the Shenzhen Sales & R&D Center ($5.01M paid-in capital) anchors Southern China tech hubs. Hong Kong (Assets: $11.42M) serves as the primary overseas logistics/settlement conduit handling 40.40% ($48.27M) of FY25 global revenues.

* Supplier Concentration & Upstream Leverage: Top-5 suppliers control 58.66% ($76.97M) of procurement. Hua Hong Semiconductor dominates SOI wafers ($26.71M, 20.35%), while Sanan IC commands GaAs procurement ($21.28M, 16.22%). OSAT partners include Xinde Semiconductor ($13.81M) and Yongsil ($6.63M). Despite domestic substitution reaching 68.37% (GaAs) and 92.09% (SOI), reliance on AWSC, GlobalFoundries, X-FAB, TSMC, and Win Semiconductors persists.

* Geopolitical Friction Points: The firm openly discloses critical dependencies on imported ASML lithography machinery for the MEMS Phase II build-out, alongside an absolute reliance on Western EDA software. Any tightening of export controls would freeze capacity expansion.

* Downstream Concentration: Client architecture is dangerously concentrated. The Top-5 customers account for 76.81% ($91.81M) of FY25 revenue. Distributors SAC (Pinjia), Hangxin, Damai, and Pinchuang represent $59.14M combined. Crucially, OPPO stands as the largest direct client ($32.67M, 27.33% of revenue) and a related-party shareholder (5.9431% equity), driving 58.69% of core gross profit.

HDIN Institutional Perspective: The Critical Edge

While management asserts that integrating the Chongqing MEMS facility generates a 30.63% cost reduction on proprietary filters—paving a theoretical path to a 2028 breakeven—HDIN Research assigns a high margin-of-error to this timeline.

Our sensitivity analysis reveals severe structural fragility: a mere 10% decrease in Average Selling Price (ASP) erodes net profit by $11.95M, completely obliterating the current 9.57% gross margin layer and pushing unit economics into negative territory. Conversely, a 10% raw material cost inflation only degrades the bottom line by $7.31M. This confirms that STAR: RadRock suffers from a chronic pricing-power deficit, not just a cost-containment issue. Furthermore, internal control audits flag prior-period restatements (a 1.02% adjustment to FY24 management fees) and a $1.65M non-operating fund occupation by Founder Ni Jianxing (subsequently repaid with interest to total $1.67M). Coupled with OPPO’s dual leverage as a massive 27.33% revenue contributor and strategic shareholder, the Street is structurally underpricing the risk of perpetual gross-margin suppression as OEMs squeeze suppliers to protect their own hardware margins.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."