SYNergy ScienTech: Capital Reallocation Near Kunshan Base as Margin Compression Signals Deficit-Driven Automation Mandate

Date : 2026-05-11

Reading : 95

Driven by a structural 400bps margin contraction resulting from Mainland China’s export tax rebate cut (13% to 9%), SYNergy’s USD $3.06 million net loss in 2025 necessitates a severe internal capital reallocation. For institutional LPs, the thesis relies on whether SYNergy can transition its Kunshan production footprint from commoditized B2B consumer cells to high-margin 5kWh Battery Backup Units (BBU) and medical-grade solid-state architectures. Failure to scale these technical moats before legacy price-mix variance further deteriorates FCF conversion capabilities presents a critical, near-term structural viability test.

Figure SYNergy ScienTech 2025 Strategic Landscape: The Pivot to High-Value Integration

Financials & Segmental Inventory

Financials & Segmental Inventory

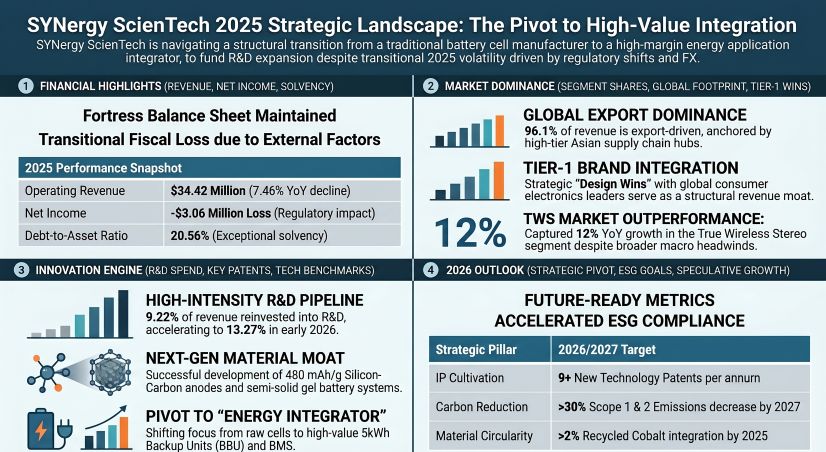

The 2025 reporting period for SYNergy indicates a classic transitional deficit profile, characterized by aggressive R&D-to-Moat translation amidst deteriorating legacy unit economics. Facing an operating loss of USD $2.00 million on revenues of USD $34.42 million (a 7.46% YoY decline), the firm's internal capital allocation is heavily skewed toward speculative capacity upgrades over immediate profit-sharing.

Segmental & Financial Audit:

* Top-Line & Segmental Mix: Total 2025 revenue reached USD $34.42 million (NT$1.07 billion). Battery Packs functioned as the core revenue engine, generating USD $30.88 million (89.72% of total), while raw Battery Cores contributed USD $3.54 million (10.28%).

* R&D-to-Moat Capital Allocation: FY2025 R&D expenditure stood at USD $3.17 million (9.22% of revenue), which aggressively accelerated to USD $0.97 million (13.27% of revenue) in Q1 2026 against just USD $7.31 million in Q1 revenue. The 2026 forward CAPEX budget reserves USD $3.74 million explicitly for R&D.

* Client Concentration Limits: The top three clients account for 40.31% of revenue, adhering to management's strict <30% individual concentration threshold. Customer #2086028 leads at 19.20% (USD $6.61M), followed by related-party #2066003 at 15.80% (USD $5.44M), and #2852049 at 5.31% (USD $1.83M).

* Executive Compensation vs. P&L: Due to the USD $3.06 million net loss, the statutory 5% employee and 2.5% director profit-sharing provisions were nullified. However, counter-cyclical retention bonuses drove General Manager Hsieh, Hsiang-Hao's total remuneration to TWD 7,281,000 (USD $233,618), maintaining leadership stability.

* Anchor Equity Resilience: Institutional stability is sustained by President International Development Corp., holding an unchanged 13,450,966 shares (14.34% of total equity), rendering minor insider sell-offs (e.g., CTO Shen, Chih-Hung's 78,500 share reduction) immaterial.

Unit Economics & Proprietary Technologies:

Operating leverage is currently depressed by foreign exchange volatility (NTD appreciation against USD) and the aforementioned 400bps export rebate haircut. To recover pricing power, SYNergy is indexing advanced chemistries:

* Silicon-Carbon (SiC) Hybrid Anodes: Scaled to 12% SiC formulation yielding 480 mAh/g capacity with >80% retention after 500 cycles at 1C.

* High-Voltage Fast Charging: Rollout of 4.45V 5C charging architectures and 4.35V NCM613+Graphite systems delivering 260 Wh/Kg at a 10C discharge rate for drone markets.

* Thermal Resilience: Gel-type semi-solid deliveries to semiconductor clients cleared extreme 270°C hot-plate tests, alongside LATP/(LLZO) solid-state iterations logging zero combustion failures.

Supply Chain Audit & Geo-Economic Moat

The physical execution of SYNergy's pivot relies on dual-hub operations: R&D housed in the Hsinchu Science Park (Taiwan, Province of China) and primary manufacturing executed by Kunshan Synergy Scientech Co., Ltd. within the Kunshan Economic and Technological Development Zone (Mainland China).

Geographic Revenue & Physical Upgrades:

The firm is heavily exposed to Asian supply chains, generating 83.88% of 2025 revenue (USD $28.87M) from the region, with the Americas lagging at 10.67%. To counteract rising regional labor OPEX and optimize production yields, a 15% automation capacity upgrade for winding and stacking lines was implemented in Kunshan.

Regulatory Compliance & Upstream Circularity:

Anticipating stringent European Union Battery Regulation mandates, the firm is overhauling its Bill of Materials (BOM) and physical architecture:

* Modular Hardware: Implementation of replaceable "Hard Pack" enclosures to meet EU lifecycle mandates.

* Material Substitution (ESG): Transitioning to PFAS-free formulations and mandating that recycled cobalt account for >2% of Lithium Cobalt Oxide (LCO) procurement in 2025, scaling to >5% by 2027.

* Decarbonization Metrics: The 2025 carbon footprint audit reported Scope 1 (601.41 tons), Scope 2 (5,174.94 tons), and Scope 3 (14,737.32 tons) emissions. With an integration of 855,800 kWh in solar generation, the firm is tracking toward its mandate of >30% renewable energy use by 2027. Safety execution remains flawless, earning a Level 2 standardization reward of USD $17,391.

HDIN Institutional Perspective

Challenge: While SYNergy outlines a sophisticated transition toward EN60730-1 certified 5kWh BBUs and high-margin drone/medical sectors, the CAPEX and 13.27% Q1 2026 R&D burn rate indicate speculative capacity expansion ahead of publicly disclosed firm order backlogs. By deliberately refraining from issuing forward revenue guidance, management signals that the 2026–2027 production ramp is preemptive rather than contracted.

Furthermore, the structural reliance on the Kunshan facility exposes the firm to acute geopolitical and trade policy risks. The abrupt 400bps margin erosion from the Chinese export tax rebate adjustment underscores a fragility that the targeted 15% automation yield improvement cannot entirely absorb. Until the LATP/(LLZO) solid-state systems and IoT semi-solid architectures register as dominant fixtures in the segmented revenue mix, the stock's near-term narrative remains tethered to raw material spot markets and severe NTD/USD exchange rate volatility rather than its R&D premium.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.

Figure SYNergy ScienTech 2025 Strategic Landscape: The Pivot to High-Value Integration

Financials & Segmental InventoryThe 2025 reporting period for SYNergy indicates a classic transitional deficit profile, characterized by aggressive R&D-to-Moat translation amidst deteriorating legacy unit economics. Facing an operating loss of USD $2.00 million on revenues of USD $34.42 million (a 7.46% YoY decline), the firm's internal capital allocation is heavily skewed toward speculative capacity upgrades over immediate profit-sharing.

Segmental & Financial Audit:

* Top-Line & Segmental Mix: Total 2025 revenue reached USD $34.42 million (NT$1.07 billion). Battery Packs functioned as the core revenue engine, generating USD $30.88 million (89.72% of total), while raw Battery Cores contributed USD $3.54 million (10.28%).

* R&D-to-Moat Capital Allocation: FY2025 R&D expenditure stood at USD $3.17 million (9.22% of revenue), which aggressively accelerated to USD $0.97 million (13.27% of revenue) in Q1 2026 against just USD $7.31 million in Q1 revenue. The 2026 forward CAPEX budget reserves USD $3.74 million explicitly for R&D.

* Client Concentration Limits: The top three clients account for 40.31% of revenue, adhering to management's strict <30% individual concentration threshold. Customer #2086028 leads at 19.20% (USD $6.61M), followed by related-party #2066003 at 15.80% (USD $5.44M), and #2852049 at 5.31% (USD $1.83M).

* Executive Compensation vs. P&L: Due to the USD $3.06 million net loss, the statutory 5% employee and 2.5% director profit-sharing provisions were nullified. However, counter-cyclical retention bonuses drove General Manager Hsieh, Hsiang-Hao's total remuneration to TWD 7,281,000 (USD $233,618), maintaining leadership stability.

* Anchor Equity Resilience: Institutional stability is sustained by President International Development Corp., holding an unchanged 13,450,966 shares (14.34% of total equity), rendering minor insider sell-offs (e.g., CTO Shen, Chih-Hung's 78,500 share reduction) immaterial.

Unit Economics & Proprietary Technologies:

Operating leverage is currently depressed by foreign exchange volatility (NTD appreciation against USD) and the aforementioned 400bps export rebate haircut. To recover pricing power, SYNergy is indexing advanced chemistries:

* Silicon-Carbon (SiC) Hybrid Anodes: Scaled to 12% SiC formulation yielding 480 mAh/g capacity with >80% retention after 500 cycles at 1C.

* High-Voltage Fast Charging: Rollout of 4.45V 5C charging architectures and 4.35V NCM613+Graphite systems delivering 260 Wh/Kg at a 10C discharge rate for drone markets.

* Thermal Resilience: Gel-type semi-solid deliveries to semiconductor clients cleared extreme 270°C hot-plate tests, alongside LATP/(LLZO) solid-state iterations logging zero combustion failures.

Supply Chain Audit & Geo-Economic Moat

The physical execution of SYNergy's pivot relies on dual-hub operations: R&D housed in the Hsinchu Science Park (Taiwan, Province of China) and primary manufacturing executed by Kunshan Synergy Scientech Co., Ltd. within the Kunshan Economic and Technological Development Zone (Mainland China).

Geographic Revenue & Physical Upgrades:

The firm is heavily exposed to Asian supply chains, generating 83.88% of 2025 revenue (USD $28.87M) from the region, with the Americas lagging at 10.67%. To counteract rising regional labor OPEX and optimize production yields, a 15% automation capacity upgrade for winding and stacking lines was implemented in Kunshan.

Regulatory Compliance & Upstream Circularity:

Anticipating stringent European Union Battery Regulation mandates, the firm is overhauling its Bill of Materials (BOM) and physical architecture:

* Modular Hardware: Implementation of replaceable "Hard Pack" enclosures to meet EU lifecycle mandates.

* Material Substitution (ESG): Transitioning to PFAS-free formulations and mandating that recycled cobalt account for >2% of Lithium Cobalt Oxide (LCO) procurement in 2025, scaling to >5% by 2027.

* Decarbonization Metrics: The 2025 carbon footprint audit reported Scope 1 (601.41 tons), Scope 2 (5,174.94 tons), and Scope 3 (14,737.32 tons) emissions. With an integration of 855,800 kWh in solar generation, the firm is tracking toward its mandate of >30% renewable energy use by 2027. Safety execution remains flawless, earning a Level 2 standardization reward of USD $17,391.

HDIN Institutional Perspective

Challenge: While SYNergy outlines a sophisticated transition toward EN60730-1 certified 5kWh BBUs and high-margin drone/medical sectors, the CAPEX and 13.27% Q1 2026 R&D burn rate indicate speculative capacity expansion ahead of publicly disclosed firm order backlogs. By deliberately refraining from issuing forward revenue guidance, management signals that the 2026–2027 production ramp is preemptive rather than contracted.

Furthermore, the structural reliance on the Kunshan facility exposes the firm to acute geopolitical and trade policy risks. The abrupt 400bps margin erosion from the Chinese export tax rebate adjustment underscores a fragility that the targeted 15% automation yield improvement cannot entirely absorb. Until the LATP/(LLZO) solid-state systems and IoT semi-solid architectures register as dominant fixtures in the segmented revenue mix, the stock's near-term narrative remains tethered to raw material spot markets and severe NTD/USD exchange rate volatility rather than its R&D premium.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.