Global Battery Materials 2026 Outlook: Why Umicore and GEM Diverge on CAPEX Allocation Amid Incoming EU Battery Passport Regulations

Date : 2026-05-11

Reading : 277

As the 2027 EU Battery Passport deadlines loom, structural divergence is defining the global battery materials sector. Euronext: UMI (Umicore) quietly wiped out $985.88 million in deferred tax assets, signaling a defensive retreat from aggressive EV capacity expansion into high-margin platinum recycling and core cash generation. Conversely, SZSE: 002340 (GEM Co., Ltd.) is aggressively leveraging its Indonesian zero-carbon nickel footprint to bypass Western trade barriers and capture Tier-1 OEM market share. For institutional LPs, this signals a critical transition: the era of speculative capacity expansion is dead, replaced by a margin-focused battle for closed-loop compliance and localized critical mineral sovereignty.

Forensic Financials & Segmental Inventory

A Forensic Analysis of the 2025 financial disclosures reveals a stark contrast in earnings quality, operational leverage, and capital discipline between the European materials incumbent and the Chinese recycling challenger.

Figure 2025 Strategic Performance Benchmark Umicore vs GEM

Umicore (Euronext: UMI) – Value Recovery & Synthetic Margin Protection

Umicore (Euronext: UMI) – Value Recovery & Synthetic Margin Protection

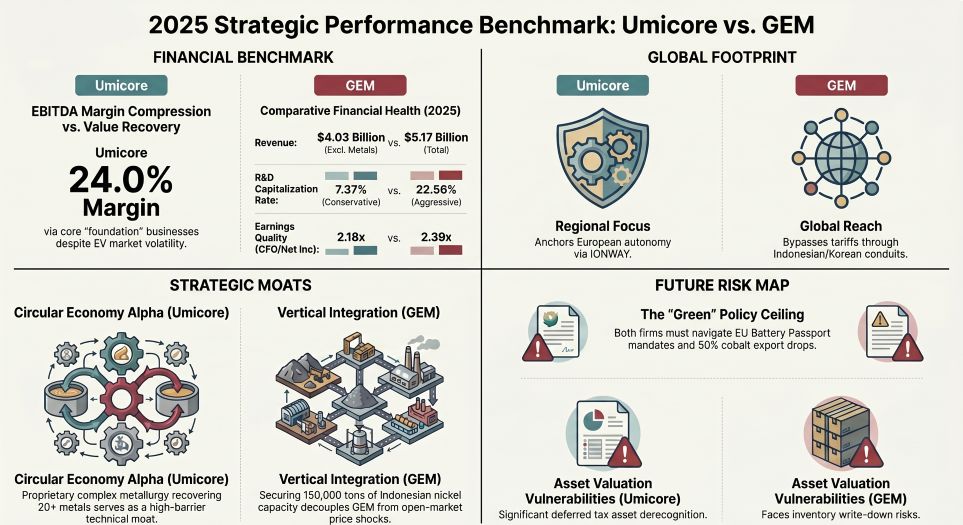

* Top-Line & Core Margins: Reported turnover of $21,904.4 million with value-added revenues (excluding metals) of $4,027.7 million. Adjusted EBITDA stood at $957.6 million (a 24.0% margin).

* Operating Leverage: Umicore generates superior unit economics with a value-added revenue per employee of $358,655. The foundation businesses drive profitability: Catalysis ($1,886.0 million revenue, 27.0% EBITDA margin) and Recycling ($1,070.8 million revenue, generating a >90% ROCE).

* Forensic Red Flags: The reported EBITDA is artificially inflated by a one-off sale-and-leaseback of permanent gold inventories, which injected a massive $550.04 million into EBITDA. Meanwhile, the Battery Materials Solutions segment ($493.3 million revenue) essentially operated at breakeven, prompting management to derecognize $985.88 million in deferred tax assets—a clear leading indicator of downgraded internal long-term EV volume projections.

* Capital Discipline: Total 2025-2028 CAPEX is strictly capped at €2.1 billion ($2.37 billion), with battery materials receiving less than €500 million. Debt architecture is highly defensive, with 83.3% of its $3,213.17 million gross debt locked at fixed interest rates.

GEM Co., Ltd. (SZSE: 002340) – Top-Line Velocity & Working Capital Friction

* Top-Line Growth: Generated $5,165.0 million in total revenue, driven heavily by New Energy Battery Materials ($2,777.3 million) and Critical Metal Extraction ($1,799.5 million). Attributable net profit surged 54.87% to $219.87 million.

* Unit Economics: Driven by high-volume, variable-cost-intensive models, direct materials account for >90% of segment costs. Value-added revenue per employee is estimated at less than $85,000 across its 9,683-strong workforce.

* Forensic Red Flags: Aggressive accounting practices are artificially buffering current-period net income. GEM capitalized 22.56% ($48.88 million) of its R&D expenditures. Furthermore, on a gross inventory balance of $1.41 billion, GEM has recorded a negligible impairment provision of only $10.80 million (0.77%), exposing the balance sheet to severe downward volatility in LME Nickel and Cobalt pricing.

* Production Volumes: Shipped 149,790 tons of Ternary Precursors (pCAM) and recovered 52,576 tons of end-of-life EV batteries (capturing >10% of China’s total retired volume).

Supply Chain Audit & Geo-Economic Moat

The physical footprints of both entities dictate their ability to navigate the incoming "Policy Ceiling," marked by the EU Corporate Sustainability Due Diligence Directive (CSDDD) and the Democratic Republic of Congo's 2026/2027 cobalt export quota reduction to 96,600 tons.

GEM’s Indonesian Bypass & Directional Circulation

GEM’s primary geo-economic moat is anchored in the International Green Industrial Park (IGIP) in Indonesia. By co-investing $232.3 million with the Indonesian Sovereign Wealth Fund, PT Vale Indonesia, and South Korea’s ECOPRO, GEM operates a state-of-the-art High-Pressure Acid Leaching (HPAL) facility that shipped over 110,839 metal tons of Mixed Hydroxide Precipitate (MHP) in 2025. This allows GEM to legally bypass Western tariffs by routing low-carbon precursor materials through Free Trade Agreement (FTA) allies like South Korea (via SK On and Samsung SDI) before final delivery to OEMs like Toyota.

Umicore’s Domesticated European Loop & Asian Retreat

Umicore’s strategy relies on extreme regional localization to satisfy EU local content mandates. Its physical moat remains the Hoboken Precious Metals Refining facility in Belgium, capable of processing highly complex multi-metal waste. Downstream, Umicore is executing a $282.65 million equity injection into the IONWAY JV facility in Nysa, Poland, deeply integrating with Volkswagen’s PowerCo via take-or-pay contracts. Conversely, Umicore is structurally retreating from peripheral Asian exposure—slating the closure of its Japanese automotive catalyst testing center by mid-2027 to consolidate operations in Songdo, South Korea, while relying on its Extra Mile Materials JV (with HS Hyosung Advanced Materials) to offshore the R&D burden for Silicon-Carbon Anodes.

HDIN Institutional Perspective

While the Street may view Umicore’s 24.0% Adjusted EBITDA margin as a sign of operational resilience amid EV macro headwinds, our forensic audit challenges this consensus. Stripping out the $550.04 million one-off gold inventory maneuver reveals a core battery materials division struggling with overcapacity and stagnant refining premiums. Umicore's decision to indefinitely postpone the commercial scale-up of its battery recycling solutions confirms a defensive posture.

Conversely, GEM is effectively dominating the global closed-loop narrative, having commercialized high-temperature activation technology that achieves a >96.5% lithium recovery rate for LFP Black Mass. However, we urge institutional investors to scrutinize GEM's shadow financing network. The company extended a $48.24 million related-party loan to the unconsolidated PT Green Eco Nickel and relies on $2.36 billion in untapped bank lines to maintain its 0.66 quick ratio. GEM's top-line scaling is fundamentally sound, but its earnings quality remains highly vulnerable to raw material cyclicality that Umicore has systematically hedged against.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Forensic Financials & Segmental Inventory

A Forensic Analysis of the 2025 financial disclosures reveals a stark contrast in earnings quality, operational leverage, and capital discipline between the European materials incumbent and the Chinese recycling challenger.

Figure 2025 Strategic Performance Benchmark Umicore vs GEM

Umicore (Euronext: UMI) – Value Recovery & Synthetic Margin Protection* Top-Line & Core Margins: Reported turnover of $21,904.4 million with value-added revenues (excluding metals) of $4,027.7 million. Adjusted EBITDA stood at $957.6 million (a 24.0% margin).

* Operating Leverage: Umicore generates superior unit economics with a value-added revenue per employee of $358,655. The foundation businesses drive profitability: Catalysis ($1,886.0 million revenue, 27.0% EBITDA margin) and Recycling ($1,070.8 million revenue, generating a >90% ROCE).

* Forensic Red Flags: The reported EBITDA is artificially inflated by a one-off sale-and-leaseback of permanent gold inventories, which injected a massive $550.04 million into EBITDA. Meanwhile, the Battery Materials Solutions segment ($493.3 million revenue) essentially operated at breakeven, prompting management to derecognize $985.88 million in deferred tax assets—a clear leading indicator of downgraded internal long-term EV volume projections.

* Capital Discipline: Total 2025-2028 CAPEX is strictly capped at €2.1 billion ($2.37 billion), with battery materials receiving less than €500 million. Debt architecture is highly defensive, with 83.3% of its $3,213.17 million gross debt locked at fixed interest rates.

GEM Co., Ltd. (SZSE: 002340) – Top-Line Velocity & Working Capital Friction

* Top-Line Growth: Generated $5,165.0 million in total revenue, driven heavily by New Energy Battery Materials ($2,777.3 million) and Critical Metal Extraction ($1,799.5 million). Attributable net profit surged 54.87% to $219.87 million.

* Unit Economics: Driven by high-volume, variable-cost-intensive models, direct materials account for >90% of segment costs. Value-added revenue per employee is estimated at less than $85,000 across its 9,683-strong workforce.

* Forensic Red Flags: Aggressive accounting practices are artificially buffering current-period net income. GEM capitalized 22.56% ($48.88 million) of its R&D expenditures. Furthermore, on a gross inventory balance of $1.41 billion, GEM has recorded a negligible impairment provision of only $10.80 million (0.77%), exposing the balance sheet to severe downward volatility in LME Nickel and Cobalt pricing.

* Production Volumes: Shipped 149,790 tons of Ternary Precursors (pCAM) and recovered 52,576 tons of end-of-life EV batteries (capturing >10% of China’s total retired volume).

Supply Chain Audit & Geo-Economic Moat

The physical footprints of both entities dictate their ability to navigate the incoming "Policy Ceiling," marked by the EU Corporate Sustainability Due Diligence Directive (CSDDD) and the Democratic Republic of Congo's 2026/2027 cobalt export quota reduction to 96,600 tons.

GEM’s Indonesian Bypass & Directional Circulation

GEM’s primary geo-economic moat is anchored in the International Green Industrial Park (IGIP) in Indonesia. By co-investing $232.3 million with the Indonesian Sovereign Wealth Fund, PT Vale Indonesia, and South Korea’s ECOPRO, GEM operates a state-of-the-art High-Pressure Acid Leaching (HPAL) facility that shipped over 110,839 metal tons of Mixed Hydroxide Precipitate (MHP) in 2025. This allows GEM to legally bypass Western tariffs by routing low-carbon precursor materials through Free Trade Agreement (FTA) allies like South Korea (via SK On and Samsung SDI) before final delivery to OEMs like Toyota.

Umicore’s Domesticated European Loop & Asian Retreat

Umicore’s strategy relies on extreme regional localization to satisfy EU local content mandates. Its physical moat remains the Hoboken Precious Metals Refining facility in Belgium, capable of processing highly complex multi-metal waste. Downstream, Umicore is executing a $282.65 million equity injection into the IONWAY JV facility in Nysa, Poland, deeply integrating with Volkswagen’s PowerCo via take-or-pay contracts. Conversely, Umicore is structurally retreating from peripheral Asian exposure—slating the closure of its Japanese automotive catalyst testing center by mid-2027 to consolidate operations in Songdo, South Korea, while relying on its Extra Mile Materials JV (with HS Hyosung Advanced Materials) to offshore the R&D burden for Silicon-Carbon Anodes.

HDIN Institutional Perspective

While the Street may view Umicore’s 24.0% Adjusted EBITDA margin as a sign of operational resilience amid EV macro headwinds, our forensic audit challenges this consensus. Stripping out the $550.04 million one-off gold inventory maneuver reveals a core battery materials division struggling with overcapacity and stagnant refining premiums. Umicore's decision to indefinitely postpone the commercial scale-up of its battery recycling solutions confirms a defensive posture.

Conversely, GEM is effectively dominating the global closed-loop narrative, having commercialized high-temperature activation technology that achieves a >96.5% lithium recovery rate for LFP Black Mass. However, we urge institutional investors to scrutinize GEM's shadow financing network. The company extended a $48.24 million related-party loan to the unconsolidated PT Green Eco Nickel and relies on $2.36 billion in untapped bank lines to maintain its 0.66 quick ratio. GEM's top-line scaling is fundamentally sound, but its earnings quality remains highly vulnerable to raw material cyclicality that Umicore has systematically hedged against.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."