Global Optical Transceiver Landscape 2025: The AI-Driven Great Divergence – Why InnoLight, Eoptolink, and Lumentum Diverge on 1.6T Capabilities Amid Southeast Asia Capex Ramps

Date : 2026-05-11

Reading : 5912

With North American hyperscalers projecting $570.8 billion in 2026 AI infrastructure capital expenditures, FY2025 optical transceiver filings reveal a brutal sector bifurcation. Pure-play 800G/1.6T developers are monopolizing datacom revenues and aggressively hoarding scarce 3nm DSP raw materials, weaponizing their balance sheets against legacy telecom incumbents. For institutional LPs, the prevailing narrative of a broad optical market recovery is a fallacy; the current super-cycle is strictly a highly concentrated AI hardware arms race dictating severe geographic decoupling and accelerating 400G telecom obsolescence.

Figure Global Optical Transceiver Landscape 2025: The Al-Driven Great Divergence

Segmental Financials & Inventory Obsolescence

Segmental Financials & Inventory Obsolescence

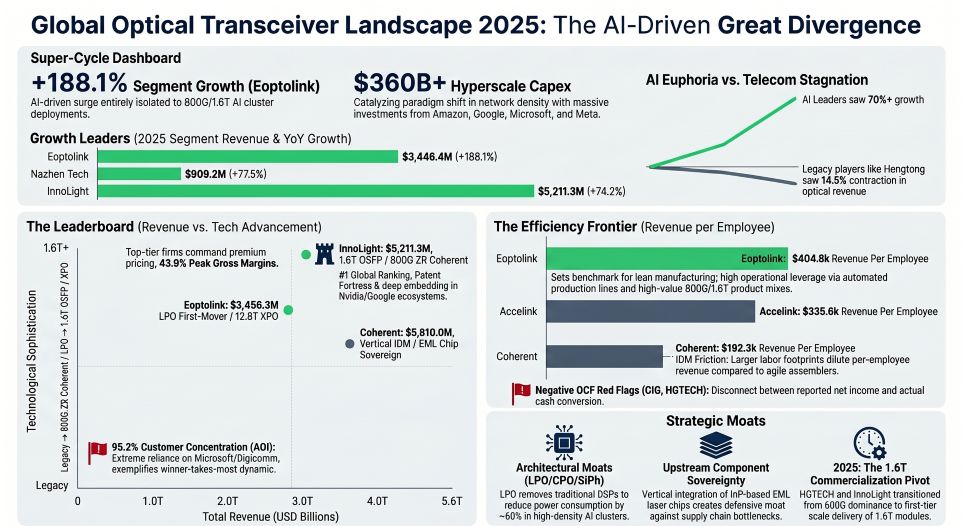

A forensic extraction of FY2025 segmental data proves the optical communications market operates on two mutually exclusive vectors: AI-driven hyper-growth and legacy telecom stagnation. Top-tier suppliers are structurally inflating raw material inventories to guarantee capacity for hyperscalers, while legacy telecom players face massive write-downs on finished goods.

* The High-Leverage Pure-Plays: SZSE: 300502 (Eoptolink) registered a 188.1% year-over-year optical segment surge to $3,446.4 million. The firm generated an industry-leading $404,837 in revenue per employee, supported by a 2.97x current ratio. Similarly, SZSE: 300308 (InnoLight) defended its #1 global position with $5,211.3 million in segment revenue (+74.2%), backing its 1.6T OSFP DR8 mass delivery with a 2,169-person R&D force that secured 44 new patents in 2025.

* The JDM Contenders: Nazhen Tech reported a 97.0% datacom spike ($760.9 million), driven heavily by its embedding into HKG: 0700 (Tencent) and ByteDance ecosystems. The firm compressed its inventory turnover to a hyper-agile 118.9 days.

* The Telecom Contraction & Write-Down Risk: NASDAQ: LITE (Lumentum) posted $1,410.8 million in cloud/networking revenues but masked a severe core operating loss of -$180.1 million via a $198.0 million UK deferred tax benefit and a $34.9 million facility sale. Meanwhile, legacy telecom operators faced toxic finished goods bloat; KOSDAQ: 138080 (OE Solutions) swallowed a 42% write-down on gross inventory, and SZSE: 002384 (Dongshan Precision) booked $173.8 million in inventory depreciation reserves.

Table Comparative FY2025 Optical & Datacom Segment Performance Benchmarking

Supply Chain Audit & Geo-Economic Moat

To navigate the US Section 301 tariffs, EAR constraints, and potential 20% fentanyl-related surcharges, the global optical supply chain is executing a massive geographic dispersion strategy, pivoting sharply to Southeast Asia and North American nearshoring.

* The Southeast Asian Migration: Capital expenditures are heavily concentrated in the "China+1" corridor. Eoptolink officially activated its Phase II facility in Thailand in early 2025. SHSE: 603083 (CIG Shanghai) explicitly doubled its output at its Malaysia hub to evade reciprocal tariffs while launching new Chip-on-Board (COB) and SMT workshops for 1.6T production. Nazhen Tech targets mid-2026 for commercial activation of its new Thai manufacturing base.

* US Nearshoring & Upstream Sovereignty: NASDAQ: AAOI (Applied Optoelectronics) is aggressively directing a 46.1% CapEx-to-Revenue ratio ($210.2 million) toward its Texas-based Molecular Beam Epitaxy (MBE) and MOCVD laser fabrication facilities to service its dominant US hyperscaler client (Microsoft, comprising 28.8% of AOI revenue). Meanwhile, Nazhen Tech injected $139.1 million into a high-end laser chip R&D and manufacturing base in Xiamen to mitigate reliance on restricted Western rare earths (gallium, germanium) and 3nm DSP imports.

* Architectural Transitions: To bypass power constraints and legacy DSP bottlenecks, Chinese fast-movers are monopolizing the Linear-drive Pluggable Optics (LPO) and Silicon Photonics (SiPh) transition. Lumentum explicitly discontinued in-house coherent DSP and RFIC development in 2025, ceding ground to agile JDM players who dominate the 800G ZR and 3.2T NPO/CPO prototyping schedules.

HDIN Institutional Perspective

While the Street continues to blindly price optical component manufacturers as a unified proxy for AI computing growth, the underlying asset structures dictate a starkly different reality. NASDAQ: AAOI claims an aggressive vertical integration moat with its Texas fabs, but a 209-day inventory turnover cycle combined with a formally disclosed "Material Weakness" in internal accounting controls signals severe execution risk that consensus estimates are currently ignoring.

Conversely, Eoptolink’s ability to generate 188.1% top-line growth with a negligible 1.0% CapEx-to-Revenue ratio ($33.4 million) challenges the thesis that 1.6T architectures require massive, heavy-asset foundries. By mastering pure-play LPO assembly and advanced Silicon Photonics packaging, Eoptolink and InnoLight have effectively decoupled from the capital-intensive InP/GaAs wafer constraints burdening Western incumbents like NYSE: COHR (Coherent), securing superior Return on Invested Capital (ROIC) spreads as the sector races toward the 2026 deployment cycle.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Global Optical Transceiver Landscape 2025: The Al-Driven Great Divergence

Segmental Financials & Inventory ObsolescenceA forensic extraction of FY2025 segmental data proves the optical communications market operates on two mutually exclusive vectors: AI-driven hyper-growth and legacy telecom stagnation. Top-tier suppliers are structurally inflating raw material inventories to guarantee capacity for hyperscalers, while legacy telecom players face massive write-downs on finished goods.

* The High-Leverage Pure-Plays: SZSE: 300502 (Eoptolink) registered a 188.1% year-over-year optical segment surge to $3,446.4 million. The firm generated an industry-leading $404,837 in revenue per employee, supported by a 2.97x current ratio. Similarly, SZSE: 300308 (InnoLight) defended its #1 global position with $5,211.3 million in segment revenue (+74.2%), backing its 1.6T OSFP DR8 mass delivery with a 2,169-person R&D force that secured 44 new patents in 2025.

* The JDM Contenders: Nazhen Tech reported a 97.0% datacom spike ($760.9 million), driven heavily by its embedding into HKG: 0700 (Tencent) and ByteDance ecosystems. The firm compressed its inventory turnover to a hyper-agile 118.9 days.

* The Telecom Contraction & Write-Down Risk: NASDAQ: LITE (Lumentum) posted $1,410.8 million in cloud/networking revenues but masked a severe core operating loss of -$180.1 million via a $198.0 million UK deferred tax benefit and a $34.9 million facility sale. Meanwhile, legacy telecom operators faced toxic finished goods bloat; KOSDAQ: 138080 (OE Solutions) swallowed a 42% write-down on gross inventory, and SZSE: 002384 (Dongshan Precision) booked $173.8 million in inventory depreciation reserves.

Table Comparative FY2025 Optical & Datacom Segment Performance Benchmarking

| Entity / Ticker | FY2025 Optical / Datacom Revenue | YoY Segment Growth | Implied Inventory Turnover | Gross Margin |

|---|---|---|---|---|

| Eoptolink (SZSE: 300502) | $3,446.4M | +188.1% | ~155 Days | 43.9% |

| InnoLight (SZSE: 300308) | $5,211.3M | +74.2% | ~208 Days | 42.6% |

| Nazhen Tech | $909.2M (Total Optics) | +77.5% | 118.9 Days | 20.0% |

| Coherent (NYSE: COHR) | $3,421.0M | +49.0% | ~139 Days | 35.0% |

| Lumentum (NASDAQ: LITE) | $1,410.8M | +30.0% | ~159 Days | 28.0% |

| Hengtong (SHSE: 600487) | $780.4M | -14.5% | N/A | 12.4% |

Supply Chain Audit & Geo-Economic Moat

To navigate the US Section 301 tariffs, EAR constraints, and potential 20% fentanyl-related surcharges, the global optical supply chain is executing a massive geographic dispersion strategy, pivoting sharply to Southeast Asia and North American nearshoring.

* The Southeast Asian Migration: Capital expenditures are heavily concentrated in the "China+1" corridor. Eoptolink officially activated its Phase II facility in Thailand in early 2025. SHSE: 603083 (CIG Shanghai) explicitly doubled its output at its Malaysia hub to evade reciprocal tariffs while launching new Chip-on-Board (COB) and SMT workshops for 1.6T production. Nazhen Tech targets mid-2026 for commercial activation of its new Thai manufacturing base.

* US Nearshoring & Upstream Sovereignty: NASDAQ: AAOI (Applied Optoelectronics) is aggressively directing a 46.1% CapEx-to-Revenue ratio ($210.2 million) toward its Texas-based Molecular Beam Epitaxy (MBE) and MOCVD laser fabrication facilities to service its dominant US hyperscaler client (Microsoft, comprising 28.8% of AOI revenue). Meanwhile, Nazhen Tech injected $139.1 million into a high-end laser chip R&D and manufacturing base in Xiamen to mitigate reliance on restricted Western rare earths (gallium, germanium) and 3nm DSP imports.

* Architectural Transitions: To bypass power constraints and legacy DSP bottlenecks, Chinese fast-movers are monopolizing the Linear-drive Pluggable Optics (LPO) and Silicon Photonics (SiPh) transition. Lumentum explicitly discontinued in-house coherent DSP and RFIC development in 2025, ceding ground to agile JDM players who dominate the 800G ZR and 3.2T NPO/CPO prototyping schedules.

HDIN Institutional Perspective

While the Street continues to blindly price optical component manufacturers as a unified proxy for AI computing growth, the underlying asset structures dictate a starkly different reality. NASDAQ: AAOI claims an aggressive vertical integration moat with its Texas fabs, but a 209-day inventory turnover cycle combined with a formally disclosed "Material Weakness" in internal accounting controls signals severe execution risk that consensus estimates are currently ignoring.

Conversely, Eoptolink’s ability to generate 188.1% top-line growth with a negligible 1.0% CapEx-to-Revenue ratio ($33.4 million) challenges the thesis that 1.6T architectures require massive, heavy-asset foundries. By mastering pure-play LPO assembly and advanced Silicon Photonics packaging, Eoptolink and InnoLight have effectively decoupled from the capital-intensive InP/GaAs wafer constraints burdening Western incumbents like NYSE: COHR (Coherent), securing superior Return on Invested Capital (ROIC) spreads as the sector races toward the 2026 deployment cycle.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."