Parrot S.A.: Fabless Defense Pivot Near South Korean EMS Hub as $54.16M Hardware Backlog Signals Structural Profitability Reversal

Date : 2026-05-12

Reading : 128

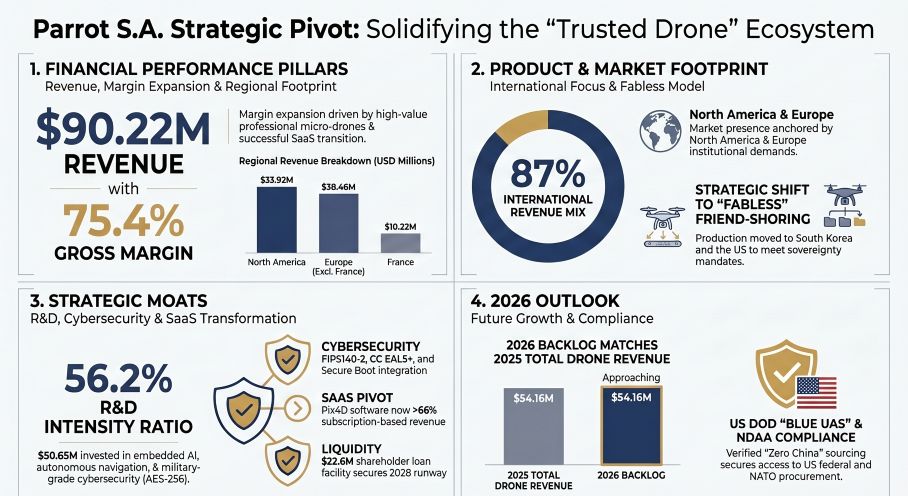

Parrot S.A.'s FY2025 disclosures reveal a calculated margin bifurcation. While public markets may penalize the widened -$14.36 million operating loss and -$8.59 million cash burn, institutional LPs must contextualize this within a front-loaded $50.65 million R&D cycle. Driven by US NDAA compliance and sovereign decoupling from China, Parrot’s strategic fabless pivot has secured an unprecedented 2026 institutional backlog. This temporary working capital drag masks a highly resilient, dual-use structural moat, positioning the firm to capture defense rearmament tailwinds alongside a high-margin SaaS transition.

Figure Parrot SA Strategic Pivot" Solidifying the “Trusted Drone” Ecosystem

Forensic Analysis: Segmental Inventory & R&D-to-Moat Translation

Forensic Analysis: Segmental Inventory & R&D-to-Moat Translation

A granular audit of Parrot’s FY2025 balance sheet and income statement reveals a classic transitional financial profile: depressed short-term profitability deliberately engineered to construct long-term recurring revenue and sovereign market share. Parrot expenses 100% of its R&D, artificially weighing down current operating margins while masking the capitalization of next-generation Intellectual Property.

Table Quantitative Inventory & Margin Bifurcation

Unit Economics & Internal Capital Allocation:

Parrot’s structural R&D expenditure is highly concentrated. With R&D personnel jumping to 68% of the total headcount (280 employees) and the sales force contracting to 12%, the firm has optimized its OPEX for B2G (Business-to-Government) defense procurement rather than consumer marketing. This technical labor concentration directly financed the CHUCK 3.0 autopilot module and the ANAFI UKR, resulting in a 2026 hardware order book that already matches the entirety of the segment's 2025 revenue ($54.16 million). Concurrently, the Pix4D division's transition from perpetual licenses to SaaS defers top-line revenue recognition but locks in a highly predictable, high-margin Annual Recurring Revenue (ARR) base for FY2026.

Supply Chain Audit & Geo-Economic Moat

To satisfy stringent US Department of Defense (DoD) "Blue UAS" and NATO requirements, Parrot executed a severe geopolitical friend-shoring strategy, deliberately establishing a "Zero China" architecture.

* Physicality & Geographic Footprint: The firm completely excised Chinese components and manufacturing from its supply chain. Final assembly for the ANAFI UKR is now exclusively hubbed through a Tier-1 Electronic Manufacturing Services (EMS) partner in South Korea, overseen by a specialized 13-person team at Parrot Korea Ltd. Meanwhile, the ANAFI USA is manufactured in the United States by OnCore. The company’s European revenue base remains anchored by a $33.80 million framework agreement with the French Defense Procurement Agency (DGA), driving domestic sales ($10.22 million) alongside strong throughput in Germany ($5.66 million) and the Netherlands ($5.51 million).

* Component Volatility & Working Capital Risk: Operating under a fabless model exposes Parrot to severe global component inflation. The AI-driven surge in memory chip demand has triggered price hikes between 35% and 100% for passive electronic components. Because Parrot depleted its net inventory by 31.2% in 2025 (dropping to $8.16 million), management faces an aggressive working capital replenishment cycle in H1 2026 to buffer against extended thermal camera lead times and secure safety stocks.

* Regulatory & Temporal Moats: Parrot's compliance with the US National Defense Authorization Act (NDAA) acts as a formidable regulatory barrier to entry for commercial competitors like DJI. Crucially, while the US Federal Communications Commission (FCC) expanded restrictions on foreign drones, Parrot secured a specific US Department of War (DoW) waiver valid until January 1, 2027. However, this waiver explicitly demands adherence to the "Buy American" standard, requiring that 65% of the drone's total cost consists of domestic US components—a strict parameter that will heavily dictate 2026 procurement routing.

HDIN Institutional Perspective

While a static DCF model might interpret the 2025 operating cash burn (-$8.59 million) as deteriorating fundamentals, HDIN's Forensic Analysis confirms this is a lagging indicator of a completed R&D investment cycle. The 2026 defense backlog acts as a synthetic forward contract, ensuring that subsequent revenue tranches will drop directly to the bottom line with minimal incremental R&D required. Furthermore, Horizon S.A.S.'s $22.61 million loan facility (maturing February 2028) guarantees operational continuity without shareholder dilution.

The Unpriced Tail Risk: Conversely, the Street is ignoring a critical contingent liability. While the active US Non-Practicing Entity (NPE) patent troll litigation will merely inflate legal OPEX, the ongoing French customs (DNRED) investigation regarding "exports without declaration" remains entirely unprovisioned on the 2025 balance sheet. Should this escalate to a formal penalty, the resulting fines and potential risk to Parrot's Authorized Economic Operator (AEO) status represent a severe, unquantified exogenous shock to FY2026 net profit margins.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Parrot SA Strategic Pivot" Solidifying the “Trusted Drone” Ecosystem

Forensic Analysis: Segmental Inventory & R&D-to-Moat TranslationA granular audit of Parrot’s FY2025 balance sheet and income statement reveals a classic transitional financial profile: depressed short-term profitability deliberately engineered to construct long-term recurring revenue and sovereign market share. Parrot expenses 100% of its R&D, artificially weighing down current operating margins while masking the capitalization of next-generation Intellectual Property.

Table Quantitative Inventory & Margin Bifurcation

| Metric (FY2025) | Recorded Value (USD) | YoY Variance / Margin | Strategic Context |

|---|---|---|---|

| Consolidated Revenue | $90.22 Million | +2% (+6% constant FX) | Hardware (60%), Software (40%). |

| Micro-Drones (Hardware) | $54.16 Million | +2% constant FX | Propelled by ANAFI UKR, representing 66% of unit volume. |

| Photogrammetry (Pix4D) | $35.95 Million | +11% constant FX | Two-thirds of segment revenue now converted to SaaS subscriptions. |

| Gross Margin | $67.95 Million | 75.4% (up from 74.1%) | Price-mix optimization through institutional hardware routing. |

| Operating Loss | -$14.36 Million | -15.9% margin | Expanded due to a $50.65M R&D cycle, equal to 56.2% of total revenue. |

| Operating Cash Flow | -$8.59 Million | Reversal from +$7.58M | Partially offset by a $3.50M working-capital benefit from inventory drawdown. |

| Intangible R&D Capital | $0.00 | N/A | Conservative accounting policy with 100% of development costs expensed. |

Unit Economics & Internal Capital Allocation:

Parrot’s structural R&D expenditure is highly concentrated. With R&D personnel jumping to 68% of the total headcount (280 employees) and the sales force contracting to 12%, the firm has optimized its OPEX for B2G (Business-to-Government) defense procurement rather than consumer marketing. This technical labor concentration directly financed the CHUCK 3.0 autopilot module and the ANAFI UKR, resulting in a 2026 hardware order book that already matches the entirety of the segment's 2025 revenue ($54.16 million). Concurrently, the Pix4D division's transition from perpetual licenses to SaaS defers top-line revenue recognition but locks in a highly predictable, high-margin Annual Recurring Revenue (ARR) base for FY2026.

Supply Chain Audit & Geo-Economic Moat

To satisfy stringent US Department of Defense (DoD) "Blue UAS" and NATO requirements, Parrot executed a severe geopolitical friend-shoring strategy, deliberately establishing a "Zero China" architecture.

* Physicality & Geographic Footprint: The firm completely excised Chinese components and manufacturing from its supply chain. Final assembly for the ANAFI UKR is now exclusively hubbed through a Tier-1 Electronic Manufacturing Services (EMS) partner in South Korea, overseen by a specialized 13-person team at Parrot Korea Ltd. Meanwhile, the ANAFI USA is manufactured in the United States by OnCore. The company’s European revenue base remains anchored by a $33.80 million framework agreement with the French Defense Procurement Agency (DGA), driving domestic sales ($10.22 million) alongside strong throughput in Germany ($5.66 million) and the Netherlands ($5.51 million).

* Component Volatility & Working Capital Risk: Operating under a fabless model exposes Parrot to severe global component inflation. The AI-driven surge in memory chip demand has triggered price hikes between 35% and 100% for passive electronic components. Because Parrot depleted its net inventory by 31.2% in 2025 (dropping to $8.16 million), management faces an aggressive working capital replenishment cycle in H1 2026 to buffer against extended thermal camera lead times and secure safety stocks.

* Regulatory & Temporal Moats: Parrot's compliance with the US National Defense Authorization Act (NDAA) acts as a formidable regulatory barrier to entry for commercial competitors like DJI. Crucially, while the US Federal Communications Commission (FCC) expanded restrictions on foreign drones, Parrot secured a specific US Department of War (DoW) waiver valid until January 1, 2027. However, this waiver explicitly demands adherence to the "Buy American" standard, requiring that 65% of the drone's total cost consists of domestic US components—a strict parameter that will heavily dictate 2026 procurement routing.

HDIN Institutional Perspective

While a static DCF model might interpret the 2025 operating cash burn (-$8.59 million) as deteriorating fundamentals, HDIN's Forensic Analysis confirms this is a lagging indicator of a completed R&D investment cycle. The 2026 defense backlog acts as a synthetic forward contract, ensuring that subsequent revenue tranches will drop directly to the bottom line with minimal incremental R&D required. Furthermore, Horizon S.A.S.'s $22.61 million loan facility (maturing February 2028) guarantees operational continuity without shareholder dilution.

The Unpriced Tail Risk: Conversely, the Street is ignoring a critical contingent liability. While the active US Non-Practicing Entity (NPE) patent troll litigation will merely inflate legal OPEX, the ongoing French customs (DNRED) investigation regarding "exports without declaration" remains entirely unprovisioned on the 2025 balance sheet. Should this escalate to a formal penalty, the resulting fines and potential risk to Parrot's Authorized Economic Operator (AEO) status represent a severe, unquantified exogenous shock to FY2026 net profit margins.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."