Hon Hai Precision Industry: AI Infrastructure Pivot Near Vietnam and India Hubs as 3.20% Operating Margin Signals Structural CDMS Realignment

Date : 2026-05-12

Reading : 464

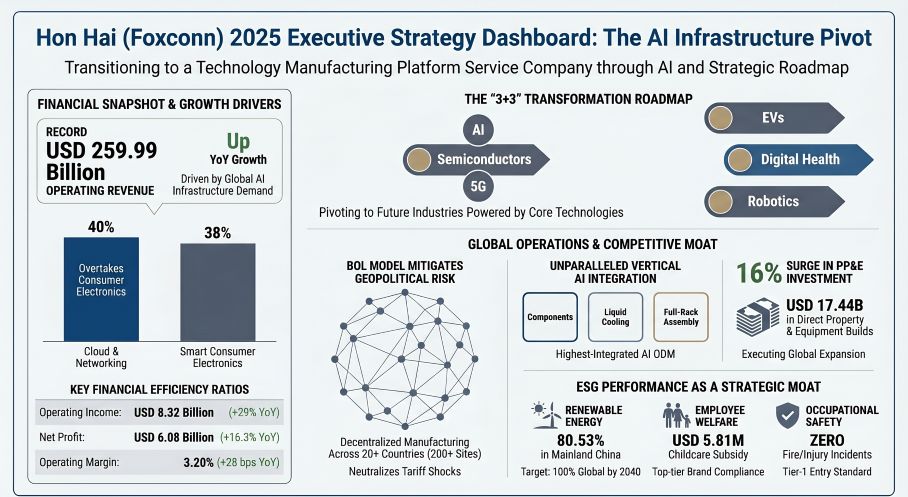

Hon Hai Precision Industry Co., Ltd. (TWSE: 2317) has structurally transcended its legacy EMS identity. In FY2025, Cloud and Networking (40% of total revenue) officially eclipsed Consumer Electronics, driving total revenue to a historic $259.99 billion. Institutional LPs must note the strategic margin divergence: while expensive AI silicon compressed gross margins to 6.15%, operating margins expanded 27 bps to 3.20%. Driven by the BOL (Build, Operate, Localize) mandate, Hon Hai is aggressively mitigating U.S.-China tariff risks by front-loading CAPEX across its Vietnam and India facilities.

Figure Hon Hai (Foxconn) 2025 Executive Strategy Dashboard: The Al Infrastructure Pivot

Forensic Financials & Segmental Inventory: Scale Economics & AI Rack-Level Integration

Forensic Financials & Segmental Inventory: Scale Economics & AI Rack-Level Integration

A forensic review of Hon Hai’s FY2025 balance sheet reveals a calculated transition from a high-volume assembly model to a highly vertically integrated Contract Design and Manufacturing Service (CDMS) framework. Management is exchanging top-line optical gross margin compression for absolute gross profit and operating margin expansion, leveraging proprietary Smart Manufacturing 3.0 infrastructure.

Table FY2025 Quantitative Inventory (USD Conversion Rate: 1 USD = 31.1663 TWD)

Margin Divergence & Operating Leverage:

The 10 bps contraction in gross margin is an illusion of product mix; integrating high-cost third-party processors into AI server racks artificially inflates the revenue denominator. The true indicator of Hon Hai's pricing power lies in the 27 bps expansion in operating margin and a robust ROE trajectory targeting 12% by 2030. The issuance of a $700 million overseas 0% convertible bond (5-year term) provides ultra-low-cost working capital to fund working capital needs for explosive AI orders without cannibalizing operating cash flow.

The Physical BOL Framework

Hon Hai’s capital deployment confirms a hard physical realignment rather than mere financial engineering. Long-Term Equity Investments actually declined by 1% to $6.34 billion, while direct Property, Plant, and Equipment (PP&E) surged 16% to $17.44 billion. The BOL footprint actively neutralizes impending geopolitical frictions and carbon border adjustments:

* Vietnam Operations: Accelerated transition toward high-value tech components. Facilities successfully completed PVT and safety structural reviews for 5.5 kW AI Power Supply Units (PSU) and 140W PD3.1 chargers.

* India Node: Formed India Chip Private Limited (40:60 JV) for technology licensing and is launching the localized Konan robotic vacuum cleaner project in Q1 2026, alongside Android 12 satellite TVs.

* Americas Hub: Expansion of Foxconn Baja California S.A. de C.V. in Mexico and Foxconn Brasil Industria e Comercio Ltda. secures local EV and server integration capacities, circumventing trans-Pacific logistics bottlenecks.

* Taiwan, Province of China (Command Center): Establishment of a sovereign supercomputing center and validation of proprietary Flo SBD dual-gun AC and 180 kW DC charging stations.

* Energy & ESG Infrastructure: Achieved an 80.53% renewable energy penetration rate in Mainland China (7.50 billion kWh out of 9.31 billion kWh). Supported by $5.81 million in childcare subsidies and strict ISO 45001 enforcement yielding zero occupational injuries in 2025, effectively acting as an ESG firewall for top-tier clients like Apple Computer, Inc.

HDIN Institutional Perspective

While the market correctly identifies TWSE: 2317 as a primary beneficiary of the AI data center build-out, the Street is mispricing the capital structure of this transition. The drop in the Cash Flow Adequacy Ratio from 64.57% to 45.52% and the 48% surge in the Cash Reinvestment Ratio (reaching 4.84%) have been superficially interpreted as an aggressive cash burn.

Our Forensic Analysis indicates otherwise. The Group is deploying its $3.90 billion R&D war chest into physical vertical integration—specifically liquid-cooling thermal solutions, structural AI racks, and SiC power semiconductors. By owning the semiconductor ecosystem from upstream design to packaging, Hon Hai completely insulates Tier-1 Cloud Service Providers (CSPs) from component shortages projected for 2026. Consequently, the temporary working capital drag is actually a structural moat. The firm is dictating full-stack CDMS terms to CSPs and automakers via its MIH platform, effectively cementing an insurmountable entry barrier for legacy EMS competitors.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Hon Hai (Foxconn) 2025 Executive Strategy Dashboard: The Al Infrastructure Pivot

Forensic Financials & Segmental Inventory: Scale Economics & AI Rack-Level IntegrationA forensic review of Hon Hai’s FY2025 balance sheet reveals a calculated transition from a high-volume assembly model to a highly vertically integrated Contract Design and Manufacturing Service (CDMS) framework. Management is exchanging top-line optical gross margin compression for absolute gross profit and operating margin expansion, leveraging proprietary Smart Manufacturing 3.0 infrastructure.

Table FY2025 Quantitative Inventory (USD Conversion Rate: 1 USD = 31.1663 TWD)

| Financial Metric / Segment | FY2025 Reported Data | YoY Variance / Context |

|---|---|---|

| Total Operating Revenue | $259.99 Billion (TWD 8.10 Trillion) | +18.13% YoY |

| Cloud & Networking | 40% of Total (~$103.99 Billion) | Largest segment, driven by AI HPC demand |

| Smart Consumer Electronics | 38% of Total (~$98.79 Billion) | Declined to second-largest segment, supported by premium product mix |

| Computing Products | 15% of Total (~$38.99 Billion) | Stable performance amid 2026 memory shortage risks |

| Components & Others | 7% of Total (~$18.20 Billion) | Includes SiC semiconductors, LEO satellites, and automotive components |

| Absolute Gross Profit | $15.98 Billion | +16% YoY |

| Gross Margin | 6.15% | -10 bps YoY due to GPU-related cost dilution |

| Operating Margin | 3.20% | +27 bps YoY from SG&A discipline and scale efficiencies |

| Net Profit Margin | 2.34% (EPS: $0.44) | +11 bps YoY |

| Operating Cash Flow (OCF) | $7.28 Billion (TWD 226.9 Billion) | +$1.95 Billion YoY |

| Total Assets | $163.79 Billion (TWD 5.10 Trillion) | +16% YoY |

| Property, Plant & Equipment (PP&E) | $17.44 Billion (TWD 543.39 Billion) | +16% YoY |

| R&D Expenditure | $3.905 Billion (TWD 121.7 Billion) | Equivalent to 1.50% of total revenue |

Margin Divergence & Operating Leverage:

The 10 bps contraction in gross margin is an illusion of product mix; integrating high-cost third-party processors into AI server racks artificially inflates the revenue denominator. The true indicator of Hon Hai's pricing power lies in the 27 bps expansion in operating margin and a robust ROE trajectory targeting 12% by 2030. The issuance of a $700 million overseas 0% convertible bond (5-year term) provides ultra-low-cost working capital to fund working capital needs for explosive AI orders without cannibalizing operating cash flow.

The Physical BOL Framework

Hon Hai’s capital deployment confirms a hard physical realignment rather than mere financial engineering. Long-Term Equity Investments actually declined by 1% to $6.34 billion, while direct Property, Plant, and Equipment (PP&E) surged 16% to $17.44 billion. The BOL footprint actively neutralizes impending geopolitical frictions and carbon border adjustments:

* Vietnam Operations: Accelerated transition toward high-value tech components. Facilities successfully completed PVT and safety structural reviews for 5.5 kW AI Power Supply Units (PSU) and 140W PD3.1 chargers.

* India Node: Formed India Chip Private Limited (40:60 JV) for technology licensing and is launching the localized Konan robotic vacuum cleaner project in Q1 2026, alongside Android 12 satellite TVs.

* Americas Hub: Expansion of Foxconn Baja California S.A. de C.V. in Mexico and Foxconn Brasil Industria e Comercio Ltda. secures local EV and server integration capacities, circumventing trans-Pacific logistics bottlenecks.

* Taiwan, Province of China (Command Center): Establishment of a sovereign supercomputing center and validation of proprietary Flo SBD dual-gun AC and 180 kW DC charging stations.

* Energy & ESG Infrastructure: Achieved an 80.53% renewable energy penetration rate in Mainland China (7.50 billion kWh out of 9.31 billion kWh). Supported by $5.81 million in childcare subsidies and strict ISO 45001 enforcement yielding zero occupational injuries in 2025, effectively acting as an ESG firewall for top-tier clients like Apple Computer, Inc.

HDIN Institutional Perspective

While the market correctly identifies TWSE: 2317 as a primary beneficiary of the AI data center build-out, the Street is mispricing the capital structure of this transition. The drop in the Cash Flow Adequacy Ratio from 64.57% to 45.52% and the 48% surge in the Cash Reinvestment Ratio (reaching 4.84%) have been superficially interpreted as an aggressive cash burn.

Our Forensic Analysis indicates otherwise. The Group is deploying its $3.90 billion R&D war chest into physical vertical integration—specifically liquid-cooling thermal solutions, structural AI racks, and SiC power semiconductors. By owning the semiconductor ecosystem from upstream design to packaging, Hon Hai completely insulates Tier-1 Cloud Service Providers (CSPs) from component shortages projected for 2026. Consequently, the temporary working capital drag is actually a structural moat. The firm is dictating full-stack CDMS terms to CSPs and automakers via its MIH platform, effectively cementing an insurmountable entry barrier for legacy EMS competitors.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."