Semiconductor 2026 Outlook: Why Qualcomm, MediaTek Diverge on ASIC Customization Amid US-China Export Controls

Date : 2026-05-12

Reading : 655

A Forensic Analysis of FY2025 filings reveals a stark architectural divergence masking highly correlated labor productivity. While Qualcomm and MediaTek both generate roughly $840k in revenue-per-employee, Qualcomm's 45% statutory net income collapse is a non-cash artifact of the incoming 2026 One Big Beautiful Bill (OBBB) Act. For institutional LPs, the critical divergence is strategic: Qualcomm is internalizing core architectures amid severe US export controls, while MediaTek hedges geopolitical friction by pivoting to custom ASICs via ecosystem partnerships, bypassing the rigid constraints of proprietary IP licensing.

Figure Qualcomm vs MediaTek: 2025 Strategic Divergence and Competitive Alpha

Forensic Financials & Segmental Inventory

Forensic Financials & Segmental Inventory

To establish relative value and peer-group ROIC spreads, we deconstruct the FY2025 capital allocation and unit economics. Despite aggressive scaling into heterogeneous computing, both entities exhibited strict working capital discipline with no evidence of cyclical inventory bloating.

Qualcomm (NASDAQ: QCOM) Quantitative Inventory:

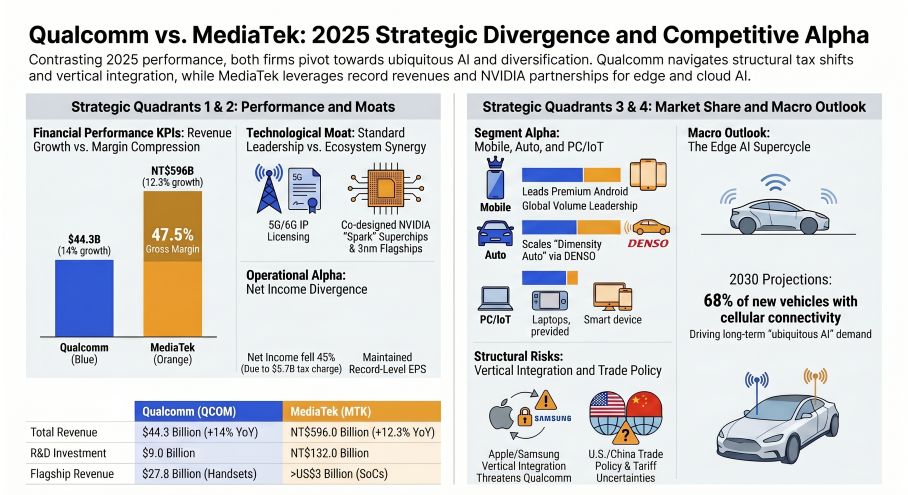

* Top-Line & Margins: Total revenue of $44.28B (+13.6% YoY). Operating income expanded +22.6% YoY to $12.36B, driving an operating margin expansion of +210 bps (from 25.8% to 27.9%). Gross unit economics were driven by QCT Handsets reaching $27.79B (+$2.93B YoY), with $2.5B directly derived from Average Selling Price (ASP) and mix expansion, versus only $423M from volume growth.

* Segmental Breakdown: Automotive revenue hit $3.957B (+36% YoY, adding $1.047B). IoT generated $6.62B. The high-margin QTL (Licensing) division reported between $5.58B and $6.41B, sustaining a 72% EBT margin.

* Cash Flow & CAPEX: Statutory Net Income plummeted 45% to $5.54B, entirely due to a $5.72B valuation allowance charge linked to the 15% alternative minimum tax under the OBBB Act effective in 2026. Adjusted Net Income stands at $11.26B. Operating Cash Flow (OCF) grew 15% YoY to $14.01B. CAPEX was $1.19B, yielding a massive Free Cash Flow (FCF) of $12.82B (2.31x statutory NI; 1.14x Adj. NI).

* Working Capital & Labor: DSO sits at a highly efficient 34 days (Average AR $4.12B, +9.8% YoY). Average Inventory is $6.47B (+1.6% YoY against COGS of $19.74B), implying ~120 Days in Inventory (DII). R&D spend was $9.04B (20% of revenue). Human capital efficiency: $851,615 revenue per employee (52,000 global headcount).

* M&A Pipeline: The pending $2.4B acquisition of Alphawave IP Group targets high-speed wired connectivity.

MediaTek (TPE: 2454) Quantitative Inventory:

*(Note: Converted at FY25 mandate: 1 USD = 31.1663 TWD)*

* Top-Line & Margins: Total revenue of $19.12B / TWD 595.965B (+12.3% YoY), maintaining a gross margin of 47.5%. Operating income settled at $3.32B / TWD 103.469B. Due to intense competitive pricing, operating costs rose 17% YoY ($10.04B / TWD 312.89B) and operating expenses rose 12%, causing operating margin compression of -190 bps (from 19.3% to 17.4%).

* Segmental Breakdown: The flagship Dimensity 9-Series directly generated >$3.0B in premium revenue.

* Cash Flow & CAPEX: Net Income saw a nominal -1% YoY contraction to $3.40B / TWD 106.12B. Cash conversion remains excellent with OCF at $5.22B / TWD 162.79B (1.53x NI). Total CAPEX of $815.6M / NT$25.42B was aggressively deployed: $483.2M / NT$15.06B for land/R&D equipment, and $332.4M / NT$10.36B for software/IP/patents.

* Labor & R&D: R&D intensity outpaced Qualcomm at 25% of revenue ($4.76B / NT$148.31B). Human capital efficiency: $836,159 revenue per employee (22,869 headcount).

Supply Chain Audit & Geo-Economic Moat

The geographic footprints of both firms expose differing vulnerabilities to OEM vertical integration and geopolitical localization mandates.

* The Fabless/Foundry Divide: MediaTek relies on 100% external manufacturing, executing critical 3nm and 2025 2nm tape-outs exclusively via TSMC in the Taiwan semiconductor infrastructure. Conversely, Qualcomm operates a hybrid model: while its primary computing silicon is outsourced, it explicitly insources the physical manufacturing of Radio Frequency Front-End (RFFE) and RF filter modules across internal proprietary facilities in Germany, Singapore, and Mainland China.

* Geographic Revenue Constraints: Qualcomm faces an acute "policy ceiling." 46% of its global revenue ($20.34B) is anchored in Mainland China/HK, and 24% ($10.51B) in the United States. This concentration was immediately penalized when the U.S. Department of Commerce revoked its export license for Huawei in May 2024. MediaTek mitigates this via a 94.26% export ratio ($18.02B) across Greater China, the U.S., Europe, Japan, Korea, and SEA, with only 5.74% ($1.097B) classified as domestic sales. Its top three unnamed clients account for concentrated risk nodes of $2.96B, $2.31B, and $2.17B respectively.

* Architectural Deployment: Qualcomm is combating internal ARM-based OEM silicon by aggressively pushing the proprietary Qualcomm Oryon CPU, Adreno GPU, and Hexagon NPU across the Snapdragon Digital Chassis and AI PC platforms. MediaTek utilizes an agile "all-big-core" ARM architecture for its Dimensity 9500, while circumventing PC OS wars by co-designing the GB10 Grace Blackwell Superchip and Dimensity Auto Cockpit Platform C-X1 with NVIDIA.

HDIN Institutional Perspective

While consensus models view Qualcomm’s $9.04B R&D pivot to proprietary architectures as a necessary margin-accretive moat against Apple’s modem replacement, we hold a differentiated viewpoint. Qualcomm's escalating legal friction with ARM over Architecture License Agreements, coupled with escalating Chinese semiconductor self-sufficiency mandates, threatens its highest-margin volumes.

Conversely, MediaTek’s "collaborative disruption" strategy is systematically underpriced by the Street. By leveraging its 400G SerDes IP, 10G-PON, and Wi-Fi 7/8 footprint into Custom ASICs rather than fighting for standalone server CPU dominance, MediaTek neutralizes the threat of in-house OEM silicon. Its ability to absorb the heavy upfront R&D (25% of revenue) to co-develop personal AI supercomputing infrastructure with Tier-1 partners like NVIDIA and DENSO offers a superior, risk-adjusted hedge against the structural demand destruction facing merchant silicon providers.

Presentation Download & Video Access:

* Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

* Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Qualcomm vs MediaTek: 2025 Strategic Divergence and Competitive Alpha

Forensic Financials & Segmental InventoryTo establish relative value and peer-group ROIC spreads, we deconstruct the FY2025 capital allocation and unit economics. Despite aggressive scaling into heterogeneous computing, both entities exhibited strict working capital discipline with no evidence of cyclical inventory bloating.

Qualcomm (NASDAQ: QCOM) Quantitative Inventory:

* Top-Line & Margins: Total revenue of $44.28B (+13.6% YoY). Operating income expanded +22.6% YoY to $12.36B, driving an operating margin expansion of +210 bps (from 25.8% to 27.9%). Gross unit economics were driven by QCT Handsets reaching $27.79B (+$2.93B YoY), with $2.5B directly derived from Average Selling Price (ASP) and mix expansion, versus only $423M from volume growth.

* Segmental Breakdown: Automotive revenue hit $3.957B (+36% YoY, adding $1.047B). IoT generated $6.62B. The high-margin QTL (Licensing) division reported between $5.58B and $6.41B, sustaining a 72% EBT margin.

* Cash Flow & CAPEX: Statutory Net Income plummeted 45% to $5.54B, entirely due to a $5.72B valuation allowance charge linked to the 15% alternative minimum tax under the OBBB Act effective in 2026. Adjusted Net Income stands at $11.26B. Operating Cash Flow (OCF) grew 15% YoY to $14.01B. CAPEX was $1.19B, yielding a massive Free Cash Flow (FCF) of $12.82B (2.31x statutory NI; 1.14x Adj. NI).

* Working Capital & Labor: DSO sits at a highly efficient 34 days (Average AR $4.12B, +9.8% YoY). Average Inventory is $6.47B (+1.6% YoY against COGS of $19.74B), implying ~120 Days in Inventory (DII). R&D spend was $9.04B (20% of revenue). Human capital efficiency: $851,615 revenue per employee (52,000 global headcount).

* M&A Pipeline: The pending $2.4B acquisition of Alphawave IP Group targets high-speed wired connectivity.

MediaTek (TPE: 2454) Quantitative Inventory:

*(Note: Converted at FY25 mandate: 1 USD = 31.1663 TWD)*

* Top-Line & Margins: Total revenue of $19.12B / TWD 595.965B (+12.3% YoY), maintaining a gross margin of 47.5%. Operating income settled at $3.32B / TWD 103.469B. Due to intense competitive pricing, operating costs rose 17% YoY ($10.04B / TWD 312.89B) and operating expenses rose 12%, causing operating margin compression of -190 bps (from 19.3% to 17.4%).

* Segmental Breakdown: The flagship Dimensity 9-Series directly generated >$3.0B in premium revenue.

* Cash Flow & CAPEX: Net Income saw a nominal -1% YoY contraction to $3.40B / TWD 106.12B. Cash conversion remains excellent with OCF at $5.22B / TWD 162.79B (1.53x NI). Total CAPEX of $815.6M / NT$25.42B was aggressively deployed: $483.2M / NT$15.06B for land/R&D equipment, and $332.4M / NT$10.36B for software/IP/patents.

* Labor & R&D: R&D intensity outpaced Qualcomm at 25% of revenue ($4.76B / NT$148.31B). Human capital efficiency: $836,159 revenue per employee (22,869 headcount).

Supply Chain Audit & Geo-Economic Moat

The geographic footprints of both firms expose differing vulnerabilities to OEM vertical integration and geopolitical localization mandates.

* The Fabless/Foundry Divide: MediaTek relies on 100% external manufacturing, executing critical 3nm and 2025 2nm tape-outs exclusively via TSMC in the Taiwan semiconductor infrastructure. Conversely, Qualcomm operates a hybrid model: while its primary computing silicon is outsourced, it explicitly insources the physical manufacturing of Radio Frequency Front-End (RFFE) and RF filter modules across internal proprietary facilities in Germany, Singapore, and Mainland China.

* Geographic Revenue Constraints: Qualcomm faces an acute "policy ceiling." 46% of its global revenue ($20.34B) is anchored in Mainland China/HK, and 24% ($10.51B) in the United States. This concentration was immediately penalized when the U.S. Department of Commerce revoked its export license for Huawei in May 2024. MediaTek mitigates this via a 94.26% export ratio ($18.02B) across Greater China, the U.S., Europe, Japan, Korea, and SEA, with only 5.74% ($1.097B) classified as domestic sales. Its top three unnamed clients account for concentrated risk nodes of $2.96B, $2.31B, and $2.17B respectively.

* Architectural Deployment: Qualcomm is combating internal ARM-based OEM silicon by aggressively pushing the proprietary Qualcomm Oryon CPU, Adreno GPU, and Hexagon NPU across the Snapdragon Digital Chassis and AI PC platforms. MediaTek utilizes an agile "all-big-core" ARM architecture for its Dimensity 9500, while circumventing PC OS wars by co-designing the GB10 Grace Blackwell Superchip and Dimensity Auto Cockpit Platform C-X1 with NVIDIA.

HDIN Institutional Perspective

While consensus models view Qualcomm’s $9.04B R&D pivot to proprietary architectures as a necessary margin-accretive moat against Apple’s modem replacement, we hold a differentiated viewpoint. Qualcomm's escalating legal friction with ARM over Architecture License Agreements, coupled with escalating Chinese semiconductor self-sufficiency mandates, threatens its highest-margin volumes.

Conversely, MediaTek’s "collaborative disruption" strategy is systematically underpriced by the Street. By leveraging its 400G SerDes IP, 10G-PON, and Wi-Fi 7/8 footprint into Custom ASICs rather than fighting for standalone server CPU dominance, MediaTek neutralizes the threat of in-house OEM silicon. Its ability to absorb the heavy upfront R&D (25% of revenue) to co-develop personal AI supercomputing infrastructure with Tier-1 partners like NVIDIA and DENSO offers a superior, risk-adjusted hedge against the structural demand destruction facing merchant silicon providers.

Presentation Download & Video Access:

* Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

* Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."