Pharmacy Automation 2026 Outlook: Why BDX, OMCL, and 68898.SS Diverge on AI-Driven CapEx Amid U.S. OBBBA Cuts and Global Labor Deficits

Date : 2026-05-12

Reading : 120

U.S. hospitals face an 88% pharmacy technician deficit and a looming $910 billion Medicaid reduction under the One Big Beautiful Bill Act (OBBBA). In response, healthcare providers are radically pivoting from static CapEx to OpEx-driven "As-a-Service" automation to preserve liquidity. FY2025 disclosures reveal a sharply bifurcated sector: while NYSE: BDX leverages its $21.8 billion scale to absorb volume-based pricing shocks, regional players like SHA: 68898 and NASDAQ: OMCL are aggressively reallocating CapEx toward AI-native software and intralogistics robotics to monetize the strict compliance mandates of the U.S. DSCSA and China’s Volume-Based Procurement (VoBP).

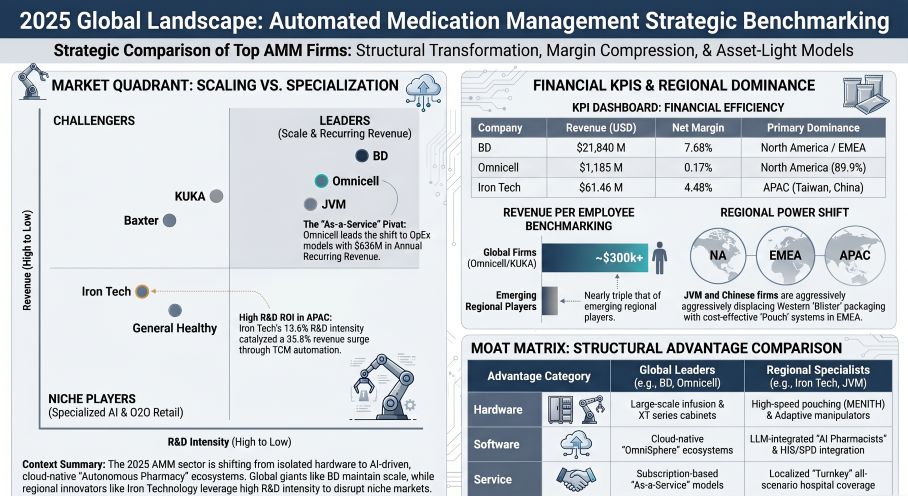

Figure 2025 Global Landscape: Automated Medication Management Strategic Benchmarking

Forensic Analysis: Sector Financials & Segmental Inventory

Forensic Analysis: Sector Financials & Segmental Inventory

The FY2025 operating environment forced a structural realignment in capital allocation. Institutional pricing pressure (GPOs/IDNs) and regional competitive bidding programs (CBP) have brutally compressed hardware margins, shifting enterprise value creation to Software-as-a-Service (SaaS) and Maintenance, Repair, and Operations (MRO).

Table Global Peer-Group Profitability & Human Capital Efficiency (FY2025)

Working Capital & Unit Economic Anomalies:

* A/R and Revenue Quality: Shanghai General Healthy (SHA: 605186) reported an 8.52% YoY revenue increase alongside a 2.64% contraction in Accounts Receivable (to $55.80M), driving Operating Cash Flow up 447.16% to $13.46M. Conversely, Suzhou Iron Tech (SHA: 68898) matched its 35.81% revenue surge with a rational 29.80% A/R expansion (to $38.65M). Both firms maintain inventory levels roughly $12.5M–$12.8M, though General Healthy carries structural "Acceptance and Impairment Risk" for delayed hospital infrastructure deployments.

* R&D-to-Moat Translation: Iron Tech registered the highest ROIC on R&D. An $8.36M investment in large language models (Alibaba Tongyi/DeepSeek) and Traditional Chinese Medicine (TCM) automation directly catalyzed a 1,959.52% surge in smart TCM product revenue, turning a net loss in 2024 into a $2.76M net profit.

* Consolidated Pharmacy Service Center (CPSC) Leverage: KOSDAQ: 054950 (JVM) commits 5.9% of revenue to R&D, actively deploying its high-throughput *MENITH* system (120 pouches/min) and *COUNTMATE* infrastructure to cannibalize traditional blister packaging market share in Europe.

Supply Chain Audit & Geo-Economic Moat

The physical footprints of these entities dictate their vulnerability to geopolitical tariffs, extreme weather (e.g., Hurricane Helene), and localized health policies.

* North American & European Hubs: Baxter faces severe regulatory overhang, underscored by FDA Official Action Indicated (OAI) and Warning Letters at its India facilities, directly threatening long-lived asset impairment. Omnicell and BD are actively executing multi-sourcing and offshore secondary facility validations to buffer against U.S. domestic supply shocks and inflation on raw materials (resins, electromechanical components).

* The Chinese Hardware-Software Divide:

* *General Healthy* is aggressively committing $12.81M in CapEx to its *Zhongxiang Intelligent Manufacturing Base* to build out proprietary AGV logistics. However, a critical supply chain red flag persists: the company is heavily dependent on its German minority shareholder, *Willach*, for its core H-type module procurement and trademark authorization.

* *Iron Tech* utilizes an asset-light "Independent Production + OEM" model. It externally procures standardized components but retains 100% in-house control over its 4π Full-Dimensional Spherical Scanning System algorithms and core control hardware.

* Global Export Nodes: Facing saturated domestic markets, Chinese operators are executing precise geopolitical expansions. *General Healthy* partnered with the Ajlan Brothers to penetrate Saudi Arabia’s Ministry of Health public hospital network. *Iron Tech* established *SIN-IRON INNOVATION TECHNOLOGY PTE. PTD.* in Singapore and deployed localized TCM automated boiling lines at the *Hong Kong Chinese Medicine Hospital*, *Hong Kong Kwong Wah Hospital*, and *Rama Hospital* in Thailand, establishing the "Hong Kong Model" for international TCM compliance.

* South Korean Autonomy: JVM operates a highly insulated, localized supply chain, procuring its ~5,000 ATDPS system components from roughly 40 domestic South Korean suppliers, shielding it from broader trans-Pacific tariff volatility.

HDIN Institutional Perspective: The Critical Edge

The Street is currently pricing these companies as traditional hardware vendors transitioning to software multiples. We challenge this consensus. The 2026 growth vector is not mere software integration; it is "Physical AI"—the deployment of autonomous mobile robots (AMRs) and AI-driven predictive logistics that break out of the central pharmacy and overtake enterprise-wide hospital logistics.

While the market rewards Omnicell for its $636M ARR via the cloud-native *OmniSphere* ecosystem, it is underpricing the structural risk of "Therapeutic Disruption" highlighted by both BD and Omnicell. The proliferation of novel alternative therapies—such as oral GLP-1 agonists—has the potential to obliterate the clinical requirement for specific medical delivery devices entirely, creating a zero-demand environment that no amount of AI optimization can fix.

Furthermore, from a geographic and capital allocation standpoint, Iron Tech offers a highly differentiated risk-reward profile compared to General Healthy. Iron Tech’s integration of AI directly into localized edge hardware (minimizing cloud latency) and its lack of reliance on foreign IP for core modules (unlike General Healthy’s Willach dependency) provides a substantially more robust technological moat amid rising trans-national trade friction.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure 2025 Global Landscape: Automated Medication Management Strategic Benchmarking

Forensic Analysis: Sector Financials & Segmental InventoryThe FY2025 operating environment forced a structural realignment in capital allocation. Institutional pricing pressure (GPOs/IDNs) and regional competitive bidding programs (CBP) have brutally compressed hardware margins, shifting enterprise value creation to Software-as-a-Service (SaaS) and Maintenance, Repair, and Operations (MRO).

Table Global Peer-Group Profitability & Human Capital Efficiency (FY2025)

| Entity | Total Revenue (USD) | Operating Margin | Net Margin | Revenue per Employee (USD) | R&D / CapEx Dynamics |

|---|---|---|---|---|---|

| Becton Dickinson (NYSE: BDX) | $21,840.00M | 11.81% | 7.68% | N/A | Large-scale absorption efficiencies offset Value-Based Procurement (VoBP) headwinds through geographic diversification. |

| Baxter (NYSE: BAX) | $11,244.00M | -2.74% | -8.51% | $299,840 | Impacted by a -$105M Novum LVP ship-and-install hold charge; R&D spending totaled $518M. |

| KUKA / Swisslog (FRA: KU2) | $4,406.17M | 1.51% | -0.20% | $302,996 | Strategic transition toward “Physical AI,” with $241.04M invested in AMRs and collaborative robotics R&D. |

| Omnicell (NASDAQ: OMCL) | $1,184.85M | 0.44% | 0.17% | $330,964 | Generated $636M ARR through OmniSphere platform; 89.9% of revenue concentrated in the U.S. market. |

| Iron Tech (SHA: 68898) | $61.46M | 3.78% | 4.48% | $79,611 | R&D intensity reached 13.6% of revenue ($8.36M), supporting 35.81% top-line growth. |

| General Healthy (SHA: 605186) | $48.07M | 9.13% | 7.45% | $142,641 | Maintenance services contributed 16.4% of revenue ($7.89M); operating cash flow surged 447.16%. |

Working Capital & Unit Economic Anomalies:

* A/R and Revenue Quality: Shanghai General Healthy (SHA: 605186) reported an 8.52% YoY revenue increase alongside a 2.64% contraction in Accounts Receivable (to $55.80M), driving Operating Cash Flow up 447.16% to $13.46M. Conversely, Suzhou Iron Tech (SHA: 68898) matched its 35.81% revenue surge with a rational 29.80% A/R expansion (to $38.65M). Both firms maintain inventory levels roughly $12.5M–$12.8M, though General Healthy carries structural "Acceptance and Impairment Risk" for delayed hospital infrastructure deployments.

* R&D-to-Moat Translation: Iron Tech registered the highest ROIC on R&D. An $8.36M investment in large language models (Alibaba Tongyi/DeepSeek) and Traditional Chinese Medicine (TCM) automation directly catalyzed a 1,959.52% surge in smart TCM product revenue, turning a net loss in 2024 into a $2.76M net profit.

* Consolidated Pharmacy Service Center (CPSC) Leverage: KOSDAQ: 054950 (JVM) commits 5.9% of revenue to R&D, actively deploying its high-throughput *MENITH* system (120 pouches/min) and *COUNTMATE* infrastructure to cannibalize traditional blister packaging market share in Europe.

Supply Chain Audit & Geo-Economic Moat

The physical footprints of these entities dictate their vulnerability to geopolitical tariffs, extreme weather (e.g., Hurricane Helene), and localized health policies.

* North American & European Hubs: Baxter faces severe regulatory overhang, underscored by FDA Official Action Indicated (OAI) and Warning Letters at its India facilities, directly threatening long-lived asset impairment. Omnicell and BD are actively executing multi-sourcing and offshore secondary facility validations to buffer against U.S. domestic supply shocks and inflation on raw materials (resins, electromechanical components).

* The Chinese Hardware-Software Divide:

* *General Healthy* is aggressively committing $12.81M in CapEx to its *Zhongxiang Intelligent Manufacturing Base* to build out proprietary AGV logistics. However, a critical supply chain red flag persists: the company is heavily dependent on its German minority shareholder, *Willach*, for its core H-type module procurement and trademark authorization.

* *Iron Tech* utilizes an asset-light "Independent Production + OEM" model. It externally procures standardized components but retains 100% in-house control over its 4π Full-Dimensional Spherical Scanning System algorithms and core control hardware.

* Global Export Nodes: Facing saturated domestic markets, Chinese operators are executing precise geopolitical expansions. *General Healthy* partnered with the Ajlan Brothers to penetrate Saudi Arabia’s Ministry of Health public hospital network. *Iron Tech* established *SIN-IRON INNOVATION TECHNOLOGY PTE. PTD.* in Singapore and deployed localized TCM automated boiling lines at the *Hong Kong Chinese Medicine Hospital*, *Hong Kong Kwong Wah Hospital*, and *Rama Hospital* in Thailand, establishing the "Hong Kong Model" for international TCM compliance.

* South Korean Autonomy: JVM operates a highly insulated, localized supply chain, procuring its ~5,000 ATDPS system components from roughly 40 domestic South Korean suppliers, shielding it from broader trans-Pacific tariff volatility.

HDIN Institutional Perspective: The Critical Edge

The Street is currently pricing these companies as traditional hardware vendors transitioning to software multiples. We challenge this consensus. The 2026 growth vector is not mere software integration; it is "Physical AI"—the deployment of autonomous mobile robots (AMRs) and AI-driven predictive logistics that break out of the central pharmacy and overtake enterprise-wide hospital logistics.

While the market rewards Omnicell for its $636M ARR via the cloud-native *OmniSphere* ecosystem, it is underpricing the structural risk of "Therapeutic Disruption" highlighted by both BD and Omnicell. The proliferation of novel alternative therapies—such as oral GLP-1 agonists—has the potential to obliterate the clinical requirement for specific medical delivery devices entirely, creating a zero-demand environment that no amount of AI optimization can fix.

Furthermore, from a geographic and capital allocation standpoint, Iron Tech offers a highly differentiated risk-reward profile compared to General Healthy. Iron Tech’s integration of AI directly into localized edge hardware (minimizing cloud latency) and its lack of reliance on foreign IP for core modules (unlike General Healthy’s Willach dependency) provides a substantially more robust technological moat amid rising trans-national trade friction.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."