Jiangsu X-chip Semiconductor: Automating Testing CAPEX Near Nanjing Yuhuatai Hub as Collapsing FCF Conversion Signals Severe Working Capital Strain

Date : 2026-05-12

Reading : 103

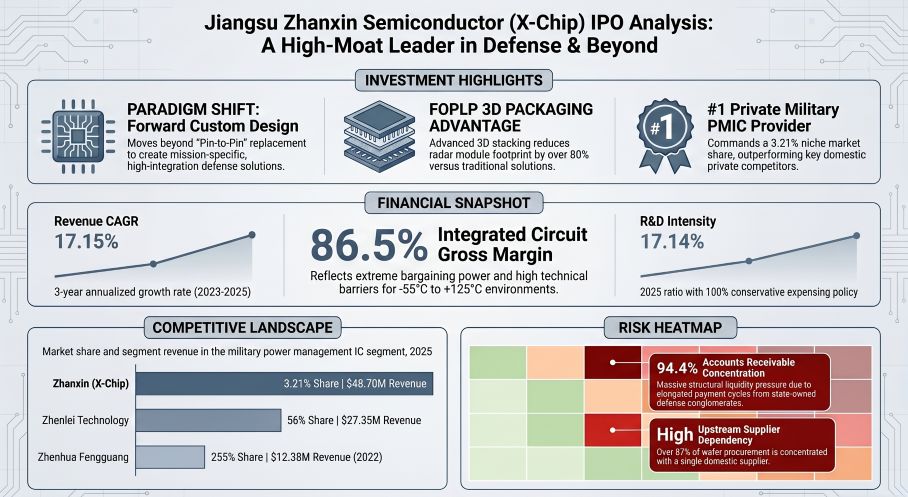

Jiangsu X-chip Semiconductor’s FY25 filings reveal a stark paradox: while net profit hit $31.74 million, operating cash flow collapsed to a mere $0.32 million. This extreme free cash flow (FCF) conversion failure is structurally tethered to China's sovereign defense procurement cycles. Institutional LPs must recognize that despite generating an 86.51% gross margin in its core IC segment, the 94.38% Accounts Receivable-to-revenue ratio exposes severe working capital capture by downstream SOEs like CETC and AVIC. Geopolitical export controls guarantee domestic top-line growth, but liquidity realization remains beholden to state budgetary constraints.

Forensic Financials & Segmental Inventory

A Forensic Analysis of X-chip’s FY23–FY25 operational metrics indicates a classic high-margin, high-friction defense contracting profile. The company utilizes a "Forward Custom Design" paradigm, completely expensing 100% of its R&D ($15.24 million in 2025, 17.14% of revenue), which anchors the high quality of its reported accounting earnings while masking acute liquidity friction.

Figure Jiangsu X-Chip lPO Analysis

Price-Mix Variance and Unit Economics (FY25):

Price-Mix Variance and Unit Economics (FY25):

* Integrated Circuits (The "Cash Cow"): Generated 54.99% of total revenue ($48.70 million). Production hit 174.95 million units, driving a 47.6% YoY sales volume surge. Crucially, while top-down military procurement reforms compressed ASP from $43.99 (2023) to $36.96 (2025), economies of scale slashed unit cost to just $4.98 (CNY 35.82). This operating leverage sustained an exceptional 86.51% segmental gross margin.

* Micro-modules (The "Star"): Representing 34.53% of revenue, this segment operates as the technological moat. Sales volume rebounded to 55.52 million units in 2025. Leveraging proprietary Panel-Level Fan-Out 3D SIP technology to bypass traditional PCB/ceramic substrates, the segment commanded a premium ASP of $55.08 and achieved a 76.91% gross margin.

* Discrete Devices: Maintained a stable volume of 35.23 million units with an ASP of $13.03.

Internal Capital Allocation & 2026-2028 Projections:

X-chip is directing $123.76 million of its $135.07 million IPO CAPEX toward structural capacity and R&D. Specifically, $59.11 million is allocated for a 4-year industrialization project (targeting new-generation LDO chips and operational amplifiers) projecting a 20.43% Internal Rate of Return (IRR) and a 7.14-year payback period. Another $16.70 million is earmarked strictly for working capital replenishment to buffer the escalating $83.93 million Accounts Receivable backlog.

Supply Chain Audit & Geo-Economic Moat

X-chip operates a highly concentrated, localized Fabless ecosystem heavily insulated from Western export controls (e.g., Wassenaar Arrangement) by generating 0% overseas revenue. However, the physical architecture of its supply chain presents acute oligopolistic bottlenecks.

* Oligopolistic Upstream Reliance: The company holds minimal bargaining power against its Tier-1 domestic foundries. In 2025, Supplier Y accounted for 87.89% of all wafer purchases, while Silmai Micro commanded 93.51% of outsourced packaging volume.

* The Yuhuatai Testing Hub Moat: To capture the premium associated with military-grade reliability (GJB-7400 standards), X-chip does not outsource final screening. The company is actively deploying $22.45 million (including $7.85 million in hardware) to construct a highly automated "Smart Factory" Testing Center in the Nanjing Yuhuatai District. By utilizing CEPREI-certified protocols, -70°C to +200°C thermoelectric temperature controls, and Automated Guided Vehicles (AGVs), X-chip is shifting its fixed-cost base to eliminate human error and scale processing capacity into the tens of millions.

* Downstream Concentration: The top five customers—dominated by defense conglomerates CETC, AVIC, CASIC, and NORINCO—accounted for 62.52% of FY25 revenue, geographically distributed primarily across East China (24.28%), Southwest China (24.18%), and North China (22.90%).

HDIN Institutional Perspective

While the prospectus aggressively markets a horizontal TAM expansion into civilian AI compute boards and automotive electric drives via its PSRR (Power Supply Rejection Ratio) IP, we challenge the near-term commercial viability of this pivot. X-chip's economic reality remains entirely captured by the Chinese defense apparatus.

The most critical latent risk is the execution of the $22.45 million Yuhuatai Testing Center. Defense procurement cycles are notoriously non-linear, as evidenced by the company's 11.41% revenue contraction in FY24 due to delayed state approvals. Building massive, automated rigid capacity risks severe fixed asset depreciation and under-utilization if downstream defense spending hits a cyclical air pocket. Institutional investors must price X-chip not as a hyper-growth commercial semiconductor entity, but as a sovereign defense toll-road where stellar 80.81% aggregate gross margins are permanently offset by high Accounts Receivable friction and multi-year cash conversion delays.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Forensic Financials & Segmental Inventory

A Forensic Analysis of X-chip’s FY23–FY25 operational metrics indicates a classic high-margin, high-friction defense contracting profile. The company utilizes a "Forward Custom Design" paradigm, completely expensing 100% of its R&D ($15.24 million in 2025, 17.14% of revenue), which anchors the high quality of its reported accounting earnings while masking acute liquidity friction.

Figure Jiangsu X-Chip lPO Analysis

Price-Mix Variance and Unit Economics (FY25):* Integrated Circuits (The "Cash Cow"): Generated 54.99% of total revenue ($48.70 million). Production hit 174.95 million units, driving a 47.6% YoY sales volume surge. Crucially, while top-down military procurement reforms compressed ASP from $43.99 (2023) to $36.96 (2025), economies of scale slashed unit cost to just $4.98 (CNY 35.82). This operating leverage sustained an exceptional 86.51% segmental gross margin.

* Micro-modules (The "Star"): Representing 34.53% of revenue, this segment operates as the technological moat. Sales volume rebounded to 55.52 million units in 2025. Leveraging proprietary Panel-Level Fan-Out 3D SIP technology to bypass traditional PCB/ceramic substrates, the segment commanded a premium ASP of $55.08 and achieved a 76.91% gross margin.

* Discrete Devices: Maintained a stable volume of 35.23 million units with an ASP of $13.03.

Internal Capital Allocation & 2026-2028 Projections:

X-chip is directing $123.76 million of its $135.07 million IPO CAPEX toward structural capacity and R&D. Specifically, $59.11 million is allocated for a 4-year industrialization project (targeting new-generation LDO chips and operational amplifiers) projecting a 20.43% Internal Rate of Return (IRR) and a 7.14-year payback period. Another $16.70 million is earmarked strictly for working capital replenishment to buffer the escalating $83.93 million Accounts Receivable backlog.

Supply Chain Audit & Geo-Economic Moat

X-chip operates a highly concentrated, localized Fabless ecosystem heavily insulated from Western export controls (e.g., Wassenaar Arrangement) by generating 0% overseas revenue. However, the physical architecture of its supply chain presents acute oligopolistic bottlenecks.

* Oligopolistic Upstream Reliance: The company holds minimal bargaining power against its Tier-1 domestic foundries. In 2025, Supplier Y accounted for 87.89% of all wafer purchases, while Silmai Micro commanded 93.51% of outsourced packaging volume.

* The Yuhuatai Testing Hub Moat: To capture the premium associated with military-grade reliability (GJB-7400 standards), X-chip does not outsource final screening. The company is actively deploying $22.45 million (including $7.85 million in hardware) to construct a highly automated "Smart Factory" Testing Center in the Nanjing Yuhuatai District. By utilizing CEPREI-certified protocols, -70°C to +200°C thermoelectric temperature controls, and Automated Guided Vehicles (AGVs), X-chip is shifting its fixed-cost base to eliminate human error and scale processing capacity into the tens of millions.

* Downstream Concentration: The top five customers—dominated by defense conglomerates CETC, AVIC, CASIC, and NORINCO—accounted for 62.52% of FY25 revenue, geographically distributed primarily across East China (24.28%), Southwest China (24.18%), and North China (22.90%).

HDIN Institutional Perspective

While the prospectus aggressively markets a horizontal TAM expansion into civilian AI compute boards and automotive electric drives via its PSRR (Power Supply Rejection Ratio) IP, we challenge the near-term commercial viability of this pivot. X-chip's economic reality remains entirely captured by the Chinese defense apparatus.

The most critical latent risk is the execution of the $22.45 million Yuhuatai Testing Center. Defense procurement cycles are notoriously non-linear, as evidenced by the company's 11.41% revenue contraction in FY24 due to delayed state approvals. Building massive, automated rigid capacity risks severe fixed asset depreciation and under-utilization if downstream defense spending hits a cyclical air pocket. Institutional investors must price X-chip not as a hyper-growth commercial semiconductor entity, but as a sovereign defense toll-road where stellar 80.81% aggregate gross margins are permanently offset by high Accounts Receivable friction and multi-year cash conversion delays.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."