Global Agrochemicals 2026 Outlook: Why Bayer, Corteva & Syngenta Diverge on CAPEX Allocation Amid APAC Destocking and EU CBAM Regulations

Date : 2026-05-13

Reading : 542

The 2025 reporting cycle reveals a structural fracture in the $80 billion agrochemical space. While originators like NYSE: Corteva and FRA: Bayer deploy billions in litigation provisions against U.S. PFAS and legacy chemical claims, agile generic platforms such as SZSE: 301035 (Rainbow) are systematically capturing downstream margins. For institutional LPs, the risk calculus must shift: the 2026–2028 active ingredient patent cliff is rapidly transferring profit pools toward integrated manufacturing. Leveraged balance sheets masking underlying cash burn via accounting accruals now face terminal value erosion.

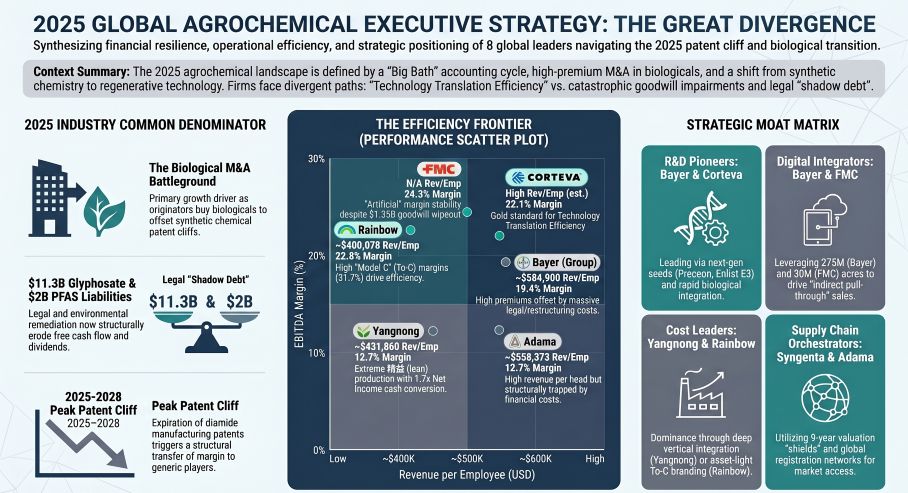

Figure 2025 GLOBAL AGROCHEMICAL EXECUTIVE STRATEGY

Margin Polarization and 'Big Bath' Profit Disguises

Margin Polarization and 'Big Bath' Profit Disguises

In FY2025, agrochemical operating leverage fractured along patent vs. generic fault lines, heavily obfuscated by "Big Bath" accounting and channel destocking anomalies. Our forensic extraction of absolute dollar amounts, percentage changes, and specific provisions reveals stark divergences in cash conversion and unit economics (converted at 2025 average rates: 1 EUR = 1.1306 USD; 1 CNY = 0.1391 USD).

Table Quantitative Inventory & Temporal Matrix (FY2025)

Geo-Economic Supply Chain Audit: Capacity Rationalization and 'Asset-Light' Arbitrage

The physicality of the agrochemical industry is shifting defensively. FRA: Bayer is consolidating R&D at the Monheim facility, relocating operations in St. Louis, and slating the Frankfurt chemical site for closure by 2028. NYSE: Corteva is executing its Crop Protection Operations Strategy Restructuring Program by closing its Pittsburg, California facility, while navigating PFAS liability investigations across four municipalities near Dordrecht, Netherlands. FRA: BASF is allocating heavy CAPEX toward the new Zhanjiang Verbund site in China, absorbing restructuring at the Ludwigshafen site, and acquiring Brisbane-based AgBiTech in H1 2026. Conversely, SHSE: 600486 (Yangnong) is structurally relocating away from the Yangtze River via the Dalian Road closure to dominate pyrethroid synthesis via the Liaoning Youchuang facility.

Regulatory Moats & The Digital/Patent Nexus

Chinese manufacturers are navigating a domestic market pumping out 4 million tons of chemical pesticides (+12% YoY capacity) by pivoting to "zero-carbon factories" to survive the "15th Five-Year Plan" restrictions. Concurrently, EU CBAM, REACH, and CLP regulations, alongside US EPA CERCLA and ESA constraints, act as regional physical ceilings. High-toxicity AIs like Paraquat, Chlorpyrifos, Chlorothalonil, Neonicotinoids, Omethoate, and Dibromoethane face severe bans.

To bridge this, originators are deploying digital agriculture and layering patents:

* Digital Reach: FRA: Bayer’s Climate FieldView spans 275 million acres, serving as an implicit retention tool for its Preceon Smart Corn System (protected through 2042) and Vyconic soybeans (2043), having issued 359,000 carbon certificates in 2024. NYSE: FMC’s Arc intelligence platform covers 20 million acres across 25 countries. Partnerships with Ginkgo Bioworks and Elemental Enzymes (Bayer) and Albaugh, Atticus, and Sharda USA (FMC) dominate external R&D/licensing.

* The 2026-2028 Cliff: FMC’s Rynaxypyr (~$0.8B) and Cyazypyr (~$0.4B) lost critical process patents in Dec 2025. Bayer’s Spidoxamat expires in Brazil/Canada/UK/EU in 2026 and the US in 2027; Bixafen SPCs expire in Russia in 2027; Isoflucypram expires in the US in 2028 (2030 in BR/CA/EU); SmartStax/SmartStax PRO run through 2028. In Pharma, Xarelto expired Jan 2026 (EU) and hits the US in 2027; Stivarga expires in Japan in 2026 and EU in 2028; Eylea formulations expire in the EU in Jun 2027. Registration lags (Brazil 5-8 years; EU/Russia/India 4-6 years; Argentina/Mexico/China 3-5 years) and 15-year US EPA re-evaluations favor agile generic platforms modeling continuous clean-tech production routes (e.g., aryloxyphenoxypropionate).

HDIN Institutional Perspective

HDIN unequivocally challenges the "macro channel destocking" narrative shielding originators like NYSE: FMC and Syngenta. A Forensic Analysis of working capital reveals systemic 'channel stuffing'. FMC’s assertion of a 2025 "inventory build to meet projected demand" fundamentally contradicts its -18% revenue collapse and catastrophic 217-day AR cycle. Similarly, Syngenta’s use of 9-month return policies—ballooning its right-of-return asset to $167M and rebate accruals to $2,415M—acts as a balance-sheet subsidy for LatAm distributors facing tight liquidity.

Furthermore, FRA: Bayer's highly irregular $2.08B impairment reversal, precisely executed to offset $8.57B in legal charges, functions as aggressive earnings-smoothing. In reality, structural value is migrating to the 'Asset-Light' To-C models. SZSE: 301035 proactively cancelling its 25,000-ton heavy-asset glyphosate project to focus capital entirely on capturing EU/NA downstream margins via its 8,900 registrations is a strategic masterstroke that the Street has not adequately priced into originator terminal values.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure 2025 GLOBAL AGROCHEMICAL EXECUTIVE STRATEGY

Margin Polarization and 'Big Bath' Profit DisguisesIn FY2025, agrochemical operating leverage fractured along patent vs. generic fault lines, heavily obfuscated by "Big Bath" accounting and channel destocking anomalies. Our forensic extraction of absolute dollar amounts, percentage changes, and specific provisions reveals stark divergences in cash conversion and unit economics (converted at 2025 average rates: 1 EUR = 1.1306 USD; 1 CNY = 0.1391 USD).

Table Quantitative Inventory & Temporal Matrix (FY2025)

| Entity | Revenue / Growth Profile | Profitability & Cash Flow | Balance Sheet / Working Capital | R&D / CAPEX / Legal Dynamics | Geographic & Strategic Notes |

|---|---|---|---|---|---|

| Bayer (Crop Science / Group) | Group revenue: $51.53B (€45.57B); Crop Science: $24.45B (€21.62B). Absorbed a -$1.97B FX revenue hit. | Clean EBITDA margin: 19.4%; Group GM: 58.7%; Net loss: -$4.07B. FCF: $2.36B. | Debt expanded to $33.73B; litigation provisions reached $8.57B. | R&D: $2.27B (9.31%); CAPEX: $1.14B. Included a controversial $2.08B impairment reversal. Projected 2026 legal cash outflow: $5.65B. | Regional split: NA $10.05B, LatAm $6.94B, EMEA $5.08B, APAC $2.38B. Workforce productivity: ~$584.9K revenue/FTE across 88,078 employees. |

| Corteva | Revenue rose +3% to $17.40B. APAC Seed segment +11%. | Gross margin: 47.3%; EBITDA margin: 22.1%; Net income: $1.19B. OCF: $3.45B; FCF: $2.86B. | Cash: $4.53B; Debt: $2.58B; Inventory: $5.67B; AR: $6.37B (133 days). | R&D: $1.47B (8.0%). Environmental provisions: $562M. Included $610M Bayer settlement and PFAS-related liabilities. | Revenue mix: NA 52%, LatAm 22%, EMEA 18%, APAC 8%. LatAm absorbed a $181M FX loss. |

| FMC Corporation | Revenue collapsed -18% to $3.47B; APAC down -83%. | Net loss: -$2.24B despite 24.3% adjusted EBITDA. FCF: -$165M; OCF: -$6.2M. | Debt: $4.07B; Inventory stable at $1.219B; AR surged to $2.06B (217 days). | Goodwill impairment: $1.35B; India divestment impact: $521.7M. Environmental provisions: $692.7M. R&D: $266.1M (7.67%); CAPEX: $85M. | Revenue mix: LatAm 39%, NA 32%, EMEA 25%, APAC 4%. Dividend cut to $0.08/share. |

| Syngenta | Revenue: $17.00B; Inventory at 37% of sales. | EBIT margin: 7.2%; Net loss: -$156M; OCF: $1.53B. | Net debt: $9.53B. AR gross rose to $3.77B; rebate accruals climbed to $2.42B. | Legal expenses reached $934M, primarily paraquat litigation. R&D: $1.19B (6.98%); CAPEX: $535M. Restructuring cost: $225M. | Regional mix: LatAm 36.4%, NA 23.5%, AMEA 18.2%, EU 17.6%. Biologicals CGU supported via 9-year DCF valuation. |

| BASF (Ag Solutions / Group) | Ag revenue: $10.84B (€9.59B); Group revenue: $67.5B (€59.7B). | Ag EBIT: $1.51B; EBITDA margin: 21.7%. | Environmental provisions: $1.20B. | Group R&D: $2.25B (3.34%); CAPEX: $4.55B. Restructuring costs: $1.06B. PFAS settlement: $316.5M. | Ag revenue mix: NA 39.8%, EU 25.8%, LatAm/MEA 23.7%, APAC 10.7%. Digital ag target: 400M hectares. |

| ADAMA Ltd. (SZSE: 000553) | Revenue: $4.05B; EBITDA margin: 12.7%. | Net loss: -$146M; OCF: $563M. | AR tightly managed at $991M (89 days). | R&D: $127.1M (3.16%). Land restoration provision: $29.5M. | Revenue mix balanced across EMEA, LatAm, APAC, and NA. Workforce productivity: ~$558.4K/employee across 7,255 staff. |

| Shandong Weifang Rainbow Chemical Co., Ltd. (SZSE: 301035) | Revenue: $2.04B; overseas sales: 99.18% of total. | Gross margin: 22.8%; Net income: ~$144M–149M. OCF: $298M. | AR extended to 165 days. | R&D: $61.3M (3.0%). Cancelled a 25,000-ton glyphosate project as part of asset-light transition. | To-C margin expanded to 31.68%. Holds 8,900 registrations and ~30 AI pipeline assets. |

| Jiangsu Yangnong Chemical Co., Ltd. (SHSE: 600486) | Revenue increased +13.76% to $1.65B. | EBIT margin: 12.7%; Net income: $179M; OCF: $308M. | AR remained disciplined at 92 days. | R&D: $54.7M (3.31%). CAPEX into Liaoning Youchuang: $139.3M. | Overseas revenue accounted for 57.3% of total. Workforce productivity: ~$431.9K/employee. |

The physicality of the agrochemical industry is shifting defensively. FRA: Bayer is consolidating R&D at the Monheim facility, relocating operations in St. Louis, and slating the Frankfurt chemical site for closure by 2028. NYSE: Corteva is executing its Crop Protection Operations Strategy Restructuring Program by closing its Pittsburg, California facility, while navigating PFAS liability investigations across four municipalities near Dordrecht, Netherlands. FRA: BASF is allocating heavy CAPEX toward the new Zhanjiang Verbund site in China, absorbing restructuring at the Ludwigshafen site, and acquiring Brisbane-based AgBiTech in H1 2026. Conversely, SHSE: 600486 (Yangnong) is structurally relocating away from the Yangtze River via the Dalian Road closure to dominate pyrethroid synthesis via the Liaoning Youchuang facility.

Regulatory Moats & The Digital/Patent Nexus

Chinese manufacturers are navigating a domestic market pumping out 4 million tons of chemical pesticides (+12% YoY capacity) by pivoting to "zero-carbon factories" to survive the "15th Five-Year Plan" restrictions. Concurrently, EU CBAM, REACH, and CLP regulations, alongside US EPA CERCLA and ESA constraints, act as regional physical ceilings. High-toxicity AIs like Paraquat, Chlorpyrifos, Chlorothalonil, Neonicotinoids, Omethoate, and Dibromoethane face severe bans.

To bridge this, originators are deploying digital agriculture and layering patents:

* Digital Reach: FRA: Bayer’s Climate FieldView spans 275 million acres, serving as an implicit retention tool for its Preceon Smart Corn System (protected through 2042) and Vyconic soybeans (2043), having issued 359,000 carbon certificates in 2024. NYSE: FMC’s Arc intelligence platform covers 20 million acres across 25 countries. Partnerships with Ginkgo Bioworks and Elemental Enzymes (Bayer) and Albaugh, Atticus, and Sharda USA (FMC) dominate external R&D/licensing.

* The 2026-2028 Cliff: FMC’s Rynaxypyr (~$0.8B) and Cyazypyr (~$0.4B) lost critical process patents in Dec 2025. Bayer’s Spidoxamat expires in Brazil/Canada/UK/EU in 2026 and the US in 2027; Bixafen SPCs expire in Russia in 2027; Isoflucypram expires in the US in 2028 (2030 in BR/CA/EU); SmartStax/SmartStax PRO run through 2028. In Pharma, Xarelto expired Jan 2026 (EU) and hits the US in 2027; Stivarga expires in Japan in 2026 and EU in 2028; Eylea formulations expire in the EU in Jun 2027. Registration lags (Brazil 5-8 years; EU/Russia/India 4-6 years; Argentina/Mexico/China 3-5 years) and 15-year US EPA re-evaluations favor agile generic platforms modeling continuous clean-tech production routes (e.g., aryloxyphenoxypropionate).

HDIN Institutional Perspective

HDIN unequivocally challenges the "macro channel destocking" narrative shielding originators like NYSE: FMC and Syngenta. A Forensic Analysis of working capital reveals systemic 'channel stuffing'. FMC’s assertion of a 2025 "inventory build to meet projected demand" fundamentally contradicts its -18% revenue collapse and catastrophic 217-day AR cycle. Similarly, Syngenta’s use of 9-month return policies—ballooning its right-of-return asset to $167M and rebate accruals to $2,415M—acts as a balance-sheet subsidy for LatAm distributors facing tight liquidity.

Furthermore, FRA: Bayer's highly irregular $2.08B impairment reversal, precisely executed to offset $8.57B in legal charges, functions as aggressive earnings-smoothing. In reality, structural value is migrating to the 'Asset-Light' To-C models. SZSE: 301035 proactively cancelling its 25,000-ton heavy-asset glyphosate project to focus capital entirely on capturing EU/NA downstream margins via its 8,900 registrations is a strategic masterstroke that the Street has not adequately priced into originator terminal values.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."