Global Seed 2026 Outlook: Why Corteva and Longping Diverge on Trait Monetization Amid Supply Chain Destocking

Date : 2026-05-13

Reading : 474

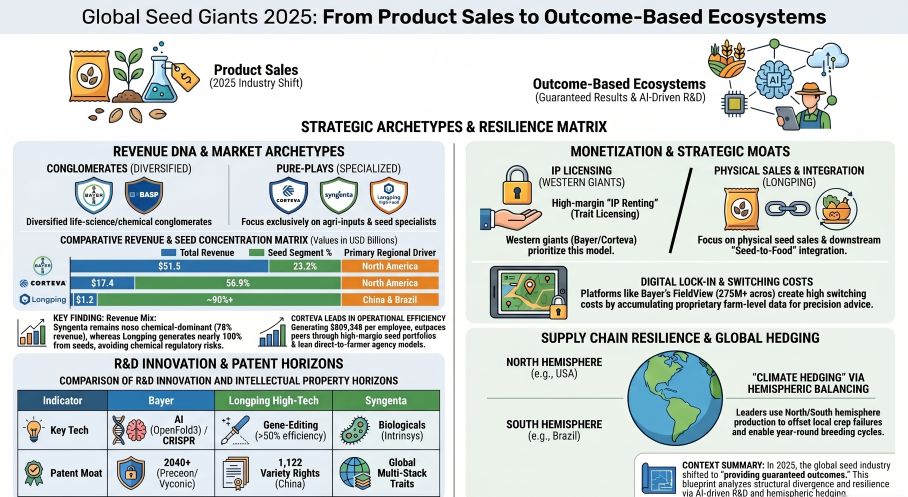

The 2025 agricultural filings reveal a structural bifurcation in seed capitalization. While NASDAQ: CTVA and ETR: BAYN mitigate generic patent cliffs by transitioning to pure-play IP licensing models—evidenced by Bayer’s $3.4B in crop science royalty revenue—emerging players like SZSE: 000998 remain tethered to physical inventory, facing a 6.7% impairment hit on massive domestic corn stockpiles. For institutional LPs, the convergence of EU Deforestation Directives and extreme weather events redefines germplasm as a critical geo-economic hedge, prioritizing asset-light trait portfolios over traditional physical distribution.

Figure Global Seed Giants 2025: From Product Sales to Outcome-Based Ecosystems

2025 Segmental Financials & Operating Leverage Matrix

2025 Segmental Financials & Operating Leverage Matrix

*(Note: Data normalized to 2025 average rates: 1 EUR = 1.1306 USD; 1 USD = 7.1875 CNY)*

A forensic analysis of the 2025 reporting season exposes critical divergence in working capital management and cash conversion cycles across the top five seed and agrochemical conglomerates.

Table FY2025 Global Seed Industry Financial, R&D & Inventory Benchmarking

Unit Economics & Specialization Variances:

* IP Royalties vs. Physical Sales: ETR: BAYN generated an immense $4,318.9M from corporate licenses ($3,406.5M exclusively from crop science) and secured a $506.5M soybean trait settlement. Syngenta booked $352.0M in third-party royalties ($349.0M from seed). Conversely, SZSE: 000998 relies on physical volumes, collecting a negligible $46K in IP fees, while facing high sales returns ($24.0M from its top 10 corn varieties alone).

* High-Margin Specialty Run-Rates: To buffer row-crop cyclicality, DeRuiter™ and Seminis™ drove Bayer’s vegetable seed division to $890.9M (+7.5% in volume/price). Syngenta’s vegetables segment grew 5% to $835.0M, though its flower division contracted 1% to $190.0M (+3% price, -4% volume). Longping’s Xiangyan (pepper) and Deruite (cucumber) vegetable revenues dipped 7.24% to $41.5M, offset by its Sanrui sunflower division, which saw a 21.79% net profit surge on $41.3M in revenue despite a 39.82% inventory volume spike.

* Employee Productivity: NASDAQ: CTVA leads sector efficiency generating $809,348 per employee (21,500 staff), compared to BASF ($623,072 / 108,251 staff), Bayer ($584,982 / 88,078 FTEs), and Longping ($279,488 / 4,220 staff).

Supply Chain Audit & Geo-Economic Moat: The Cross-Hemisphere Hedge

The physicality of the global seed trade requires a "Northern Hemisphere Spring / Southern Hemisphere Autumn" capacity hedge to mitigate biological degradation.

* Logistics & Germplasm Hubs: NASDAQ: CTVA operates 61 exclusive seed hubs (38 in North America, 8 in LatAm, 12 in EMEA, 3 in APAC). ETR: BAS concentrates biological formulation at its Ludwigshafen facility, while ETR: BAYN expands its Monheim R&D facility. SZSE: 000998 manages 900,000 *mu* of domestic bases (concentrated in Gansu, Xinjiang, and the Hainan Ledong Base Phase II), but derived $509.0M (47.6% of sales) from its LongPing Brazil subsidiary in Mato Grosso to capture the *Safrinha* subtropical corn cycle.

* Inventory Destocking & Quality Decay: Seed is a decaying biological asset. Syngenta holds a massive $6.31B seed inventory (37% of sales) with a $584.0M total provision balance ($173.0M specific to 2025 physical deterioration and market obsolescence). SZSE: 000998 carries a $360.0M domestic corn inventory load, forcing an 8.72% impairment ($31.4M) due to acute oversupply in the Chinese row-crop market.

Regulatory Backlogs, Patent Expiries & Defensive Litigation

Global asynchronously timed regulatory frameworks present the highest barrier to capital returns (ROCE).

* Litigation & Compliance Provisions: ETR: BAYN's net loss is entirely driven by a staggering $11.3B provision for legacy Roundup/PCB suits, expensing $5.52B in 2025 alone. Syngenta booked a $792.0M litigation settlement provision (Paraquat/VIPTERA MIR162). Emerging market risks are severe: SZSE: 000998's Brazilian subsidiary faces a $191.0M LatAm tax penalty risk and expensed a direct $6.01M loss to professional cyber fraud.

* The 2028-2043 Patent Cliff: ETR: BAYN’s legacy SmartStax™ patent expires in 2028. To counter this, it is deploying the Preceon™ Smart Corn System (patent protected to 2042) and Vyconic™ soybeans (protected to 2043). In LatAm, Brazil’s Supreme Court restricted patent limits to 20 years, threatening Intacta RR2 PRO margins. NASDAQ: CTVA actively defends its Enlist E3® and Conkesta E3® platforms, utilizing its 16,100 active patents to fight generic Roundup Ready® Corn 2 encroachment.

* China’s IP Protection Pivot: Benefiting from the new Essential Derivation Variety (EDV) system, SZSE: 000998 secured a landmark $3.2M (CNY 23M) infringement victory. The firm holds 1,122 plant variety rights, 125 patents, and 14 national GM safety certificates (driving 19 approved GM corn varieties).

ESG Carbon Monetization & Next-Gen Digital Breeding

Digital platforms have evolved from agronomic tools into pure-play data exfiltration and carbon monetization engines.

* Carbon Subscriptions & Data Lock-In: ETR: BAYN's Climate FieldView™ tracks 275 million acres globally. Through its PRO Carbono program, Bayer monetized 170,000 tons of CO2 equivalent in 2025, dropping its GHG intensity by 20% (to 581kg CO2e/ton). ETR: BAS targets 400 million digital hectares, currently generating 48.5% of sales from sustainable TripleS product lines. SZSE: 000998's Cloud Ag platform registers 9.7 million users (100,000 DAU), boosting yield by 100 *jin/mu*.

* Gene Editing (BT+DT): Bayer leverages the OpenFold3 AI model to bypass traditional screening, planning to scale Preceon™ from 86,000 US acres in 2025 to 200,000 US acres and 32,000 European hectares by 2026. SZSE: 000998 deployed a DH-GS (Whole Genome Selection) system, increasing haploid gene editing efficiency to >50% and advancing 128 Phase 3 (L3) combinations.

HDIN Institutional Perspective

While the Street treats pure-play seed companies like Longping as rapid beneficiaries of China's GM commercialization, the forensic balance sheet tells a different story. Longping's $23.1M reported net income is optically inflated by $17.2M in government grants, $12.3M in direct subsidies, and $1.1M in asset disposals. Furthermore, its $371.1M in accounts receivable, tied heavily to dealer credit, paired with heavy related-party transactions (requesting $70M in deposits and $47M in loans via CITIC Finance) signals severe channel congestion. Comparatively, the Western oligopoly's transition to an "IP Licensing + Carbon Credit" SaaS model ensures a long-term ROCE expansion that hardware-heavy domestic producers cannot currently match.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Global Seed Giants 2025: From Product Sales to Outcome-Based Ecosystems

2025 Segmental Financials & Operating Leverage Matrix*(Note: Data normalized to 2025 average rates: 1 EUR = 1.1306 USD; 1 USD = 7.1875 CNY)*

A forensic analysis of the 2025 reporting season exposes critical divergence in working capital management and cash conversion cycles across the top five seed and agrochemical conglomerates.

Table FY2025 Global Seed Industry Financial, R&D & Inventory Benchmarking

FY2025 Global Seed Industry Financial, R&D & Inventory Benchmarking

| Entity / Ticker | Total / Seed Revenue ($M) | Seed R&D / CapEx ($M) | Operating Cash Flow ($M) | Net Income / Loss ($M) | Inventory Provisioning & Impairments ($M) |

|---|---|---|---|---|---|

| Bayer (ETR: BAYN) | $51,527.1 / $11,976.4 | $2,275.9 / $1,140.8 | $6,700.0 | -$4,092.8 | ROCE deteriorated to -1.4%. |

| Corteva (NASDAQ: CTVA) | $17,401.0 / $9,898.0 | $1,474.0 / $377.0 | $3,460.0 | $1,105.0 | FIFO accounting implemented across 60% of seed inventory. |

| Syngenta | $16,999.0 / $3,747.0 | $427.0 / $535.0 | $1,530.0 | -$152.0 | Seed inventory reached $6.31B; seed-related impairments totaled $173.0M. |

| BASF (ETR: BAS) | $67,448.2 / $2,290.6 | $1,119.3 / $396.8 | $6,340.0 | $1,830.4 | Agricultural impairment charges totaled $10.2M. |

| Yuan Longping High-tech Agriculture Co., Ltd. (SZSE: 000998) | $1,179.4 / $1,058.6 | $106.2 / $39.6 | $104.6 | $23.1 | Gross inventory stood at $642.9M with $43.0M impairment provisions. |

Unit Economics & Specialization Variances:

* IP Royalties vs. Physical Sales: ETR: BAYN generated an immense $4,318.9M from corporate licenses ($3,406.5M exclusively from crop science) and secured a $506.5M soybean trait settlement. Syngenta booked $352.0M in third-party royalties ($349.0M from seed). Conversely, SZSE: 000998 relies on physical volumes, collecting a negligible $46K in IP fees, while facing high sales returns ($24.0M from its top 10 corn varieties alone).

* High-Margin Specialty Run-Rates: To buffer row-crop cyclicality, DeRuiter™ and Seminis™ drove Bayer’s vegetable seed division to $890.9M (+7.5% in volume/price). Syngenta’s vegetables segment grew 5% to $835.0M, though its flower division contracted 1% to $190.0M (+3% price, -4% volume). Longping’s Xiangyan (pepper) and Deruite (cucumber) vegetable revenues dipped 7.24% to $41.5M, offset by its Sanrui sunflower division, which saw a 21.79% net profit surge on $41.3M in revenue despite a 39.82% inventory volume spike.

* Employee Productivity: NASDAQ: CTVA leads sector efficiency generating $809,348 per employee (21,500 staff), compared to BASF ($623,072 / 108,251 staff), Bayer ($584,982 / 88,078 FTEs), and Longping ($279,488 / 4,220 staff).

Supply Chain Audit & Geo-Economic Moat: The Cross-Hemisphere Hedge

The physicality of the global seed trade requires a "Northern Hemisphere Spring / Southern Hemisphere Autumn" capacity hedge to mitigate biological degradation.

* Logistics & Germplasm Hubs: NASDAQ: CTVA operates 61 exclusive seed hubs (38 in North America, 8 in LatAm, 12 in EMEA, 3 in APAC). ETR: BAS concentrates biological formulation at its Ludwigshafen facility, while ETR: BAYN expands its Monheim R&D facility. SZSE: 000998 manages 900,000 *mu* of domestic bases (concentrated in Gansu, Xinjiang, and the Hainan Ledong Base Phase II), but derived $509.0M (47.6% of sales) from its LongPing Brazil subsidiary in Mato Grosso to capture the *Safrinha* subtropical corn cycle.

* Inventory Destocking & Quality Decay: Seed is a decaying biological asset. Syngenta holds a massive $6.31B seed inventory (37% of sales) with a $584.0M total provision balance ($173.0M specific to 2025 physical deterioration and market obsolescence). SZSE: 000998 carries a $360.0M domestic corn inventory load, forcing an 8.72% impairment ($31.4M) due to acute oversupply in the Chinese row-crop market.

Regulatory Backlogs, Patent Expiries & Defensive Litigation

Global asynchronously timed regulatory frameworks present the highest barrier to capital returns (ROCE).

* Litigation & Compliance Provisions: ETR: BAYN's net loss is entirely driven by a staggering $11.3B provision for legacy Roundup/PCB suits, expensing $5.52B in 2025 alone. Syngenta booked a $792.0M litigation settlement provision (Paraquat/VIPTERA MIR162). Emerging market risks are severe: SZSE: 000998's Brazilian subsidiary faces a $191.0M LatAm tax penalty risk and expensed a direct $6.01M loss to professional cyber fraud.

* The 2028-2043 Patent Cliff: ETR: BAYN’s legacy SmartStax™ patent expires in 2028. To counter this, it is deploying the Preceon™ Smart Corn System (patent protected to 2042) and Vyconic™ soybeans (protected to 2043). In LatAm, Brazil’s Supreme Court restricted patent limits to 20 years, threatening Intacta RR2 PRO margins. NASDAQ: CTVA actively defends its Enlist E3® and Conkesta E3® platforms, utilizing its 16,100 active patents to fight generic Roundup Ready® Corn 2 encroachment.

* China’s IP Protection Pivot: Benefiting from the new Essential Derivation Variety (EDV) system, SZSE: 000998 secured a landmark $3.2M (CNY 23M) infringement victory. The firm holds 1,122 plant variety rights, 125 patents, and 14 national GM safety certificates (driving 19 approved GM corn varieties).

ESG Carbon Monetization & Next-Gen Digital Breeding

Digital platforms have evolved from agronomic tools into pure-play data exfiltration and carbon monetization engines.

* Carbon Subscriptions & Data Lock-In: ETR: BAYN's Climate FieldView™ tracks 275 million acres globally. Through its PRO Carbono program, Bayer monetized 170,000 tons of CO2 equivalent in 2025, dropping its GHG intensity by 20% (to 581kg CO2e/ton). ETR: BAS targets 400 million digital hectares, currently generating 48.5% of sales from sustainable TripleS product lines. SZSE: 000998's Cloud Ag platform registers 9.7 million users (100,000 DAU), boosting yield by 100 *jin/mu*.

* Gene Editing (BT+DT): Bayer leverages the OpenFold3 AI model to bypass traditional screening, planning to scale Preceon™ from 86,000 US acres in 2025 to 200,000 US acres and 32,000 European hectares by 2026. SZSE: 000998 deployed a DH-GS (Whole Genome Selection) system, increasing haploid gene editing efficiency to >50% and advancing 128 Phase 3 (L3) combinations.

HDIN Institutional Perspective

While the Street treats pure-play seed companies like Longping as rapid beneficiaries of China's GM commercialization, the forensic balance sheet tells a different story. Longping's $23.1M reported net income is optically inflated by $17.2M in government grants, $12.3M in direct subsidies, and $1.1M in asset disposals. Furthermore, its $371.1M in accounts receivable, tied heavily to dealer credit, paired with heavy related-party transactions (requesting $70M in deposits and $47M in loans via CITIC Finance) signals severe channel congestion. Comparatively, the Western oligopoly's transition to an "IP Licensing + Carbon Credit" SaaS model ensures a long-term ROCE expansion that hardware-heavy domestic producers cannot currently match.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."