Global Premium Auto 2026 Outlook: Why Volkswagen Group, Ferrari, and Lotus Diverge on Capital Allocation Amid US-China Trade Fragmentation

Date : 2026-05-13

Reading : 264

The 2025 automotive filings expose a brutal divergence in capital efficiency. While Ferrari leverages absolute scarcity to achieve a 147% cash conversion ratio, legacy stalwarts like Volkswagen Group and Mercedes-Benz face severe margin compression from US-China tariffs and European ELV antitrust fines. For institutional LPs, the critical narrative is cash leakage. With Lotus masking cash burn via Geely-linked receivables and Aston Martin utilizing off-balance-sheet dealer financing, the transition to Software-Defined Vehicles is aggressively vaporizing historical ROIC spreads.

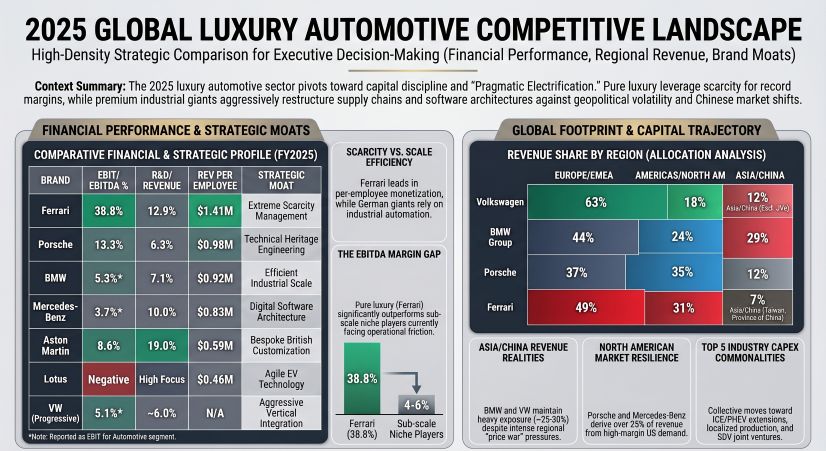

Figure 2025 GLOBAL LUXURY AUTOMOTIVE COMPETITIVE LANDSCAPE

Ferrari’s Scarcity vs. Volkswagen Group’s Scale

Ferrari’s Scarcity vs. Volkswagen Group’s Scale

The 2025 fiscal data reveals a strict stratification between "Pure Luxury" human-capital monetization, "Premium Industrial" capex rationalization, and "Sub-Scale" balance sheet distress.

Table FY2025 Global Luxury & Performance Automotive Financial Benchmarking

Unit Economics, Earnings Management & Pricing Power:

* The Scarcity Premium & Repurchase Rates: Ferrari capped output at 13,640 units, achieving extreme pricing power. Algorithmic allocation prioritized existing clients, yielding an 84% repurchase rate. Aston Martin drove its core ASP to $244,052, supported by the hyper-personalization of its *Q Commissions* and a build-to-order transition.

* Agency vs. Wholesale Margins: Mercedes-Benz and BMW Group successfully deployed the Agency Model across Europe, retaining direct terminal pricing control and optimizing SG&A (Mercedes-Benz reduced selling expenses to $10.98B). BMW Group plans to fully transition its main brand to this model by 2027. Conversely, Lotus reversed its D2C strategy back to a legacy dealer model, triggering massive wholesale discounting that compressed gross margins from 15.0% to 3.2%.

* Channel Stuffing & Liquidity Red Flags: Forensic auditing exposes severe earnings management among sub-scale players. Lotus recorded $114.1M in related-party Accounts Receivable (96.2% of total AR, heavily tied to the Geely Group), signaling artificial channel stuffing rather than end-consumer demand. Aston Martin utilizes off-balance-sheet wholesale finance facilities via CAAB/Stellantis to shield $207.2M of dealer inventory risk, masking liquidity shortfalls with $52.2M in "inventory repurchase arrangements."

* R&D Capitalization & Impairments: Porsche AG proactively flushed its balance sheet, cutting its R&D capitalization rate from 62.6% to 42.0%. This triggered a $1.21B non-cash development impairment as it postponed its new electric vehicle platform into the 2030s, alongside a $791M impairment on the halted *Cellforce Group* battery expansion, protecting future ROIC at the expense of FY25 net income.

Geopolitical Supply Chain Audit: BMW Group's Localized Fortification vs. Lotus's Fragile Ecosystem

The transition to electrification has forced a polarization between absolute vertical integration and fragile, asset-light ecosystem reliance amidst hardening regulatory environments.

The Physicality & Sourcing Topography:

* "Local-for-Local" Fortification: To neutralize US-China 100% tariffs, BMW Group has erected high-voltage battery assembly facilities directly adjacent to vehicle plants in *Debrecen, Irlbach-Straßkirchen, Woodruff, San Luis Potosí*, and *Shenyang*. Volkswagen Group vertically integrated upstream by acquiring a 9.9% stake in *Patriot Battery Metals* (Canada) and a 24% stake in *Gotion* ($2.37B valuation) to secure IRA-compliant lithium and bypass Chinese mineral chokepoints.

* Asset-Light Geopolitical Fragility: Lotus operates with critical fragility. Heavily reliant on US-origin silicon (*NVIDIA Orin X, Qualcomm 8155*) but geographically tethered to Geely’s Tier-1 facility in *Wuhan*, the company is caught between US Bureau of Industry and Security (BIS) technology export controls and EU anti-subsidy EV tariffs (up to 18.8%). Similarly, Ferrari explicitly flags its single-source dependency for hybrid electronic components as a critical vulnerability to production continuity.

* Contingent Liabilities & Compliance Backlog: European compliance costs are bleeding operating cash flow. Volkswagen Group carries a $4.52B emission litigation provision (including a $4.29B KapMuG exposure) and absorbed a $144M EU ELV antitrust fine. Mercedes-Benz added hundreds of millions in provisions for the UK FCA finance probe and US environmental settlements. These penalties are projected to convert into substantial operating cash outflows between 2026 and 2027. Furthermore, thermal window rulings by the KBA have forced Porsche AG and BMW Group to prepare for imminent hardware/software retrofitting costs.

HDIN Institutional Perspective

While the industry narrative aggressively pitches Software-Defined Vehicles (SDVs) and Feature-on-Demand (FoD) as the ultimate margin panacea, our forensic analysis indicates the Street is mispricing the actual B2C monetization trajectory.

The data confirms that software B2C revenue remains statistically negligible in the current fiscal year. Lotus's $56.3M in service revenue constitutes merely ~10.8% of total top-line, and Volkswagen Group's *CARIAD* unit—despite claiming $2.0B in revenue—is entirely intra-group while operating at a $2.46B loss. Automakers are not currently generating accretive SaaS margins; rather, they are executing defensive, multi-billion-dollar joint ventures (Volkswagen Group committing $5.8B to *Rivian* to target 2035 AD-MaaS rollouts, BMW Group localizing via *Alibaba/DeepSeek*) simply to prevent legacy electrical architectures from becoming obsolete. The required localized capital expenditure, combined with GDPR and Chinese data compliance, functions as an aggressive capex sink rather than an immediate revenue multiplier.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure 2025 GLOBAL LUXURY AUTOMOTIVE COMPETITIVE LANDSCAPE

Ferrari’s Scarcity vs. Volkswagen Group’s ScaleThe 2025 fiscal data reveals a strict stratification between "Pure Luxury" human-capital monetization, "Premium Industrial" capex rationalization, and "Sub-Scale" balance sheet distress.

Table FY2025 Global Luxury & Performance Automotive Financial Benchmarking

| Entity | FY2025 Revenue (USD) | EBIT / EBITDA Margin | Operating Cash Flow (USD) | R&D / CAPEX Profile (USD) | Revenue per Employee (USD) |

|---|---|---|---|---|---|

| Ferrari | $8,079.3M | 38.8% EBITDA | $2,656.0M | $1.04B R&D / $311M CAPEX | $1.41M (5,718 HC) |

| Porsche AG | $41,009.1M | 13.3% EBIT | $4,086.0M | $2.59B R&D | $0.98M (41,780 HC) |

| Volkswagen Group | $363.95B | 5.1% (Progressive) | $35.5B | $21.95B R&D / $16.96B CAPEX | N/A |

| BMW Group | $150.88B | 5.3% Automotive EBIT | N/A | $9.40B R&D | $0.92M (143,691 HC) |

| Mercedes-Benz Group | $149.48B | 3.7% Cars EBIT | N/A | $10.94B R&D / $6.20B CAPEX | $0.83M (131,895 HC) |

| Aston Martin | $1,659.6M | 8.6% EBITDA | $97.7M | $316.0M R&D / $450M CAPEX | $0.59M (2,807 HC) |

| Lotus Cars | $519.1M | Negative | -$848.5M | N/A (51% of headcount allocated to R&D) | $0.46M (1,132 HC) |

* The Scarcity Premium & Repurchase Rates: Ferrari capped output at 13,640 units, achieving extreme pricing power. Algorithmic allocation prioritized existing clients, yielding an 84% repurchase rate. Aston Martin drove its core ASP to $244,052, supported by the hyper-personalization of its *Q Commissions* and a build-to-order transition.

* Agency vs. Wholesale Margins: Mercedes-Benz and BMW Group successfully deployed the Agency Model across Europe, retaining direct terminal pricing control and optimizing SG&A (Mercedes-Benz reduced selling expenses to $10.98B). BMW Group plans to fully transition its main brand to this model by 2027. Conversely, Lotus reversed its D2C strategy back to a legacy dealer model, triggering massive wholesale discounting that compressed gross margins from 15.0% to 3.2%.

* Channel Stuffing & Liquidity Red Flags: Forensic auditing exposes severe earnings management among sub-scale players. Lotus recorded $114.1M in related-party Accounts Receivable (96.2% of total AR, heavily tied to the Geely Group), signaling artificial channel stuffing rather than end-consumer demand. Aston Martin utilizes off-balance-sheet wholesale finance facilities via CAAB/Stellantis to shield $207.2M of dealer inventory risk, masking liquidity shortfalls with $52.2M in "inventory repurchase arrangements."

* R&D Capitalization & Impairments: Porsche AG proactively flushed its balance sheet, cutting its R&D capitalization rate from 62.6% to 42.0%. This triggered a $1.21B non-cash development impairment as it postponed its new electric vehicle platform into the 2030s, alongside a $791M impairment on the halted *Cellforce Group* battery expansion, protecting future ROIC at the expense of FY25 net income.

Geopolitical Supply Chain Audit: BMW Group's Localized Fortification vs. Lotus's Fragile Ecosystem

The transition to electrification has forced a polarization between absolute vertical integration and fragile, asset-light ecosystem reliance amidst hardening regulatory environments.

The Physicality & Sourcing Topography:

* "Local-for-Local" Fortification: To neutralize US-China 100% tariffs, BMW Group has erected high-voltage battery assembly facilities directly adjacent to vehicle plants in *Debrecen, Irlbach-Straßkirchen, Woodruff, San Luis Potosí*, and *Shenyang*. Volkswagen Group vertically integrated upstream by acquiring a 9.9% stake in *Patriot Battery Metals* (Canada) and a 24% stake in *Gotion* ($2.37B valuation) to secure IRA-compliant lithium and bypass Chinese mineral chokepoints.

* Asset-Light Geopolitical Fragility: Lotus operates with critical fragility. Heavily reliant on US-origin silicon (*NVIDIA Orin X, Qualcomm 8155*) but geographically tethered to Geely’s Tier-1 facility in *Wuhan*, the company is caught between US Bureau of Industry and Security (BIS) technology export controls and EU anti-subsidy EV tariffs (up to 18.8%). Similarly, Ferrari explicitly flags its single-source dependency for hybrid electronic components as a critical vulnerability to production continuity.

* Contingent Liabilities & Compliance Backlog: European compliance costs are bleeding operating cash flow. Volkswagen Group carries a $4.52B emission litigation provision (including a $4.29B KapMuG exposure) and absorbed a $144M EU ELV antitrust fine. Mercedes-Benz added hundreds of millions in provisions for the UK FCA finance probe and US environmental settlements. These penalties are projected to convert into substantial operating cash outflows between 2026 and 2027. Furthermore, thermal window rulings by the KBA have forced Porsche AG and BMW Group to prepare for imminent hardware/software retrofitting costs.

HDIN Institutional Perspective

While the industry narrative aggressively pitches Software-Defined Vehicles (SDVs) and Feature-on-Demand (FoD) as the ultimate margin panacea, our forensic analysis indicates the Street is mispricing the actual B2C monetization trajectory.

The data confirms that software B2C revenue remains statistically negligible in the current fiscal year. Lotus's $56.3M in service revenue constitutes merely ~10.8% of total top-line, and Volkswagen Group's *CARIAD* unit—despite claiming $2.0B in revenue—is entirely intra-group while operating at a $2.46B loss. Automakers are not currently generating accretive SaaS margins; rather, they are executing defensive, multi-billion-dollar joint ventures (Volkswagen Group committing $5.8B to *Rivian* to target 2035 AD-MaaS rollouts, BMW Group localizing via *Alibaba/DeepSeek*) simply to prevent legacy electrical architectures from becoming obsolete. The required localized capital expenditure, combined with GDPR and Chinese data compliance, functions as an aggressive capex sink rather than an immediate revenue multiplier.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."