Quantinuum: Enterprise Hardware Pivot Near Colorado Headquarters as 45-Month Lease Signals Shift in Commercial Qubit Economics

Date : 2026-05-13

Reading : 613

Quantinuum’s FY2025 Form S-1 reveals a definitive structural pivot from cloud-based exploration to dedicated hardware leasing, driven by a 45-month enterprise deployment that generated $16.53 million in upfront revenue. For institutional LPs, the critical narrative is the company's 535% R&D-to-revenue burn rate and the looming talent stock-based compensation shock post-IPO. Operating under strict CFIUS constraints, Quantinuum’s path to 2029 commercial fault-tolerance hinges on mitigating severe customer concentration—where Japanese and U.S. sovereign entities accounted for over 75% of revenue—while scaling production amidst tightening global export controls on dual-use technology.

Figure Quantinuum: Scaling the Frontier of Fault-Tolerant Quantum Computing

Forensic Analysis of FY2024–Q1 2026 Financial Data

Forensic Analysis of FY2024–Q1 2026 Financial Data

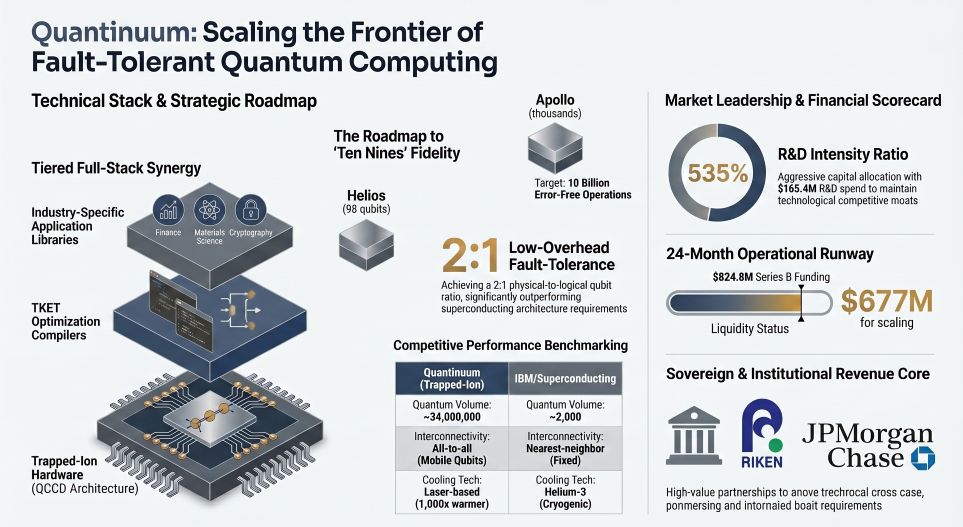

Quantinuum’s transition from theoretical physics to enterprise commercialization is evident in its internal capital allocation and extreme price-mix variance. The revenue base is highly volatile, driven by capital-intensive, outcome-oriented IP deployments rather than predictable recurring Software-as-a-Service (SaaS) subscriptions.

* Top-Line & Segmental Inventory (FY2025): Total net revenue reached $30.93 million (+34.6% YoY). The mix heavily favored Specialized Quantum Computing Hardware at 53.4% ($16.53 million), generated entirely by a single 45-month sales-type lease. Cloud Platform & Support Services (Software & Cyber) accounted for 47.8% ($14.78 million), a sharp drop from $23.26 million in FY2024 as a major client cannibalized cloud spend in favor of dedicated hardware.

* Operating Leverage & Unit Economics: The company exhibits extreme technology-driven cost structures. FY2025 R&D expenditures hit $165.42 million (535% of total revenue), driven by the transition from the *Helios* architecture (98 physical qubits) to the upcoming 2027 *Sol* system (192 physical qubits).

* GTM & Capital Conversion: S&M expenditures spiked 305% YoY in Q1 2026 to $13.74 million, signaling an aggressive commercial ramp-up. Despite a quarterly cash burn of $85.56 million in Q1 2026, a massive $824.8 million Series B financing leaves the company with $677.01 million in liquidity, providing an estimated 23.7-month runway without further dilution.

* Customer Concentration: Extreme fragility exists in the revenue base. A single client (RIKEN) generated 60% of FY2025 revenue ($18.76 million), while the U.S. Government accounted for 16%. Consequently, Q1 2026 revenue contracted 73% YoY to $5.24 million following the exhaustion of upfront hardware revenue recognition in the prior year.

*(Note: Quantinuum benefits structurally from a "subsidy" via parent company Honeywell (NASDAQ: HON), which retains a 55% pre-IPO stake and handles ion-trap fabrication at cost plus 15% markup).*

Physical Infrastructure & Regulatory Choke Points

Quantinuum operates a highly distributed hardware and intellectual property footprint across 13 global hubs. However, its geo-economic moat is constrained by single-source supplier bottlenecks and stringent U.S. Export Administration Regulations (EAR).

* Primary Production Footprint: Hardware assembly is anchored in Broomfield, Colorado. To meet a target of manufacturing "multiple systems per year," the company recently dedicated an additional 17,000 square feet specifically for commercial capacity expansion.

* APAC Deployment Ecosystem: The Asia-Pacific region is the dominant commercial engine, generating 68.1% of FY2025 revenue. Operations are anchored by the Wako, Japan facility on the RIKEN campus, with a fifth global system slated for deployment in Singapore by late 2026 to capture sovereign tech demand.

* Tier-1 Dependencies & Resource Vulnerabilities: The Quantum Charge-Coupled Device (QCCD) architecture fundamentally relies on liquid helium for cryogenic liquefaction and a specific, isotopically enriched atomic element procured solely through the U.S. Department of Energy Isotope Program. Additionally, core ion-trap manufacturing relies on licensed IP from Leonardo DRS (NASDAQ: DRS); any breach of this license could instantly halt hardware production.

* Geopolitical Talent Constraints: Operating under a Committee on Foreign Investment in the United States (CFIUS) National Security Agreement (NSA), Quantinuum faces indefinite restrictions on hiring foreign nationals, severely limiting its access to the global quantum physics labor pool.

HDIN Institutional Perspective: Project-Based Sovereign Consulting Disguised as SaaS

While the S-1 prospectus attempts to frame Quantinuum as a "software-enabled hybrid computing platform" integrated with mega-cap ecosystems like Microsoft Azure (NASDAQ: MSFT) and NVIDIA (NASDAQ: NVDA), the financial forensics reveal a different reality. The 73% revenue collapse in Q1 2026 and the 90% concentration with RIKEN in Q1 2025 suggest a business model heavily dependent on erratic, massive sovereign pilot projects rather than sustainable enterprise SaaS adoption.

However, Quantinuum possesses a highly asymmetrical advantage in its "negative Customer Acquisition Cost (CAC)" dynamic. Through Cooperative Research and Development Agreements (CRADAs) with government entities, institutional clients effectively subsidize the $2 billion historical R&D burn rate. While commercial scale-up poses severe liquidity risks, the company’s technical moat is unassailable: achieving a 99.921% two-qubit gate fidelity and a 2:1 physical-to-logical error-correction ratio on the *Helios* system mathematically validates their QCCD trajectory toward commercial fault-tolerance by the 2029 *Apollo* deployment.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Quantinuum: Scaling the Frontier of Fault-Tolerant Quantum Computing

Forensic Analysis of FY2024–Q1 2026 Financial DataQuantinuum’s transition from theoretical physics to enterprise commercialization is evident in its internal capital allocation and extreme price-mix variance. The revenue base is highly volatile, driven by capital-intensive, outcome-oriented IP deployments rather than predictable recurring Software-as-a-Service (SaaS) subscriptions.

* Top-Line & Segmental Inventory (FY2025): Total net revenue reached $30.93 million (+34.6% YoY). The mix heavily favored Specialized Quantum Computing Hardware at 53.4% ($16.53 million), generated entirely by a single 45-month sales-type lease. Cloud Platform & Support Services (Software & Cyber) accounted for 47.8% ($14.78 million), a sharp drop from $23.26 million in FY2024 as a major client cannibalized cloud spend in favor of dedicated hardware.

* Operating Leverage & Unit Economics: The company exhibits extreme technology-driven cost structures. FY2025 R&D expenditures hit $165.42 million (535% of total revenue), driven by the transition from the *Helios* architecture (98 physical qubits) to the upcoming 2027 *Sol* system (192 physical qubits).

* GTM & Capital Conversion: S&M expenditures spiked 305% YoY in Q1 2026 to $13.74 million, signaling an aggressive commercial ramp-up. Despite a quarterly cash burn of $85.56 million in Q1 2026, a massive $824.8 million Series B financing leaves the company with $677.01 million in liquidity, providing an estimated 23.7-month runway without further dilution.

* Customer Concentration: Extreme fragility exists in the revenue base. A single client (RIKEN) generated 60% of FY2025 revenue ($18.76 million), while the U.S. Government accounted for 16%. Consequently, Q1 2026 revenue contracted 73% YoY to $5.24 million following the exhaustion of upfront hardware revenue recognition in the prior year.

*(Note: Quantinuum benefits structurally from a "subsidy" via parent company Honeywell (NASDAQ: HON), which retains a 55% pre-IPO stake and handles ion-trap fabrication at cost plus 15% markup).*

Physical Infrastructure & Regulatory Choke Points

Quantinuum operates a highly distributed hardware and intellectual property footprint across 13 global hubs. However, its geo-economic moat is constrained by single-source supplier bottlenecks and stringent U.S. Export Administration Regulations (EAR).

* Primary Production Footprint: Hardware assembly is anchored in Broomfield, Colorado. To meet a target of manufacturing "multiple systems per year," the company recently dedicated an additional 17,000 square feet specifically for commercial capacity expansion.

* APAC Deployment Ecosystem: The Asia-Pacific region is the dominant commercial engine, generating 68.1% of FY2025 revenue. Operations are anchored by the Wako, Japan facility on the RIKEN campus, with a fifth global system slated for deployment in Singapore by late 2026 to capture sovereign tech demand.

* Tier-1 Dependencies & Resource Vulnerabilities: The Quantum Charge-Coupled Device (QCCD) architecture fundamentally relies on liquid helium for cryogenic liquefaction and a specific, isotopically enriched atomic element procured solely through the U.S. Department of Energy Isotope Program. Additionally, core ion-trap manufacturing relies on licensed IP from Leonardo DRS (NASDAQ: DRS); any breach of this license could instantly halt hardware production.

* Geopolitical Talent Constraints: Operating under a Committee on Foreign Investment in the United States (CFIUS) National Security Agreement (NSA), Quantinuum faces indefinite restrictions on hiring foreign nationals, severely limiting its access to the global quantum physics labor pool.

HDIN Institutional Perspective: Project-Based Sovereign Consulting Disguised as SaaS

While the S-1 prospectus attempts to frame Quantinuum as a "software-enabled hybrid computing platform" integrated with mega-cap ecosystems like Microsoft Azure (NASDAQ: MSFT) and NVIDIA (NASDAQ: NVDA), the financial forensics reveal a different reality. The 73% revenue collapse in Q1 2026 and the 90% concentration with RIKEN in Q1 2025 suggest a business model heavily dependent on erratic, massive sovereign pilot projects rather than sustainable enterprise SaaS adoption.

However, Quantinuum possesses a highly asymmetrical advantage in its "negative Customer Acquisition Cost (CAC)" dynamic. Through Cooperative Research and Development Agreements (CRADAs) with government entities, institutional clients effectively subsidize the $2 billion historical R&D burn rate. While commercial scale-up poses severe liquidity risks, the company’s technical moat is unassailable: achieving a 99.921% two-qubit gate fidelity and a 2:1 physical-to-logical error-correction ratio on the *Helios* system mathematically validates their QCCD trajectory toward commercial fault-tolerance by the 2029 *Apollo* deployment.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."