Global Animal Health 2026 Outlook: Why Zoetis, Merck & Elanco Diverge on Operational Leverage Amid Asian Import Substitution

Date : 2026-05-14

Reading : 484

The structural humanization of pets has permanently decoupled companion animal therapeutics from cyclical agricultural economics. As the 2026–2030 patent cliff threatens legacy blockbuster cash flows, multinational incumbents are deploying massive capital into monoclonal antibodies and smart biomanufacturing to defend premium pricing. Concurrently, regional challengers in mainland China are exploiting severe commodity deflation to fortify raw-material-to-formulation integration, aggressively capturing domestic market share. For institutional LPs, this sharp divergence in balance sheet leverage and geographic concentration signals a fundamental repricing of sector risk premiums ahead of Vietnam's 2026 antibiotic ban.

Figure Global Animal Health 2025: Strategic Divergence and the Battle for Market Sovereignty

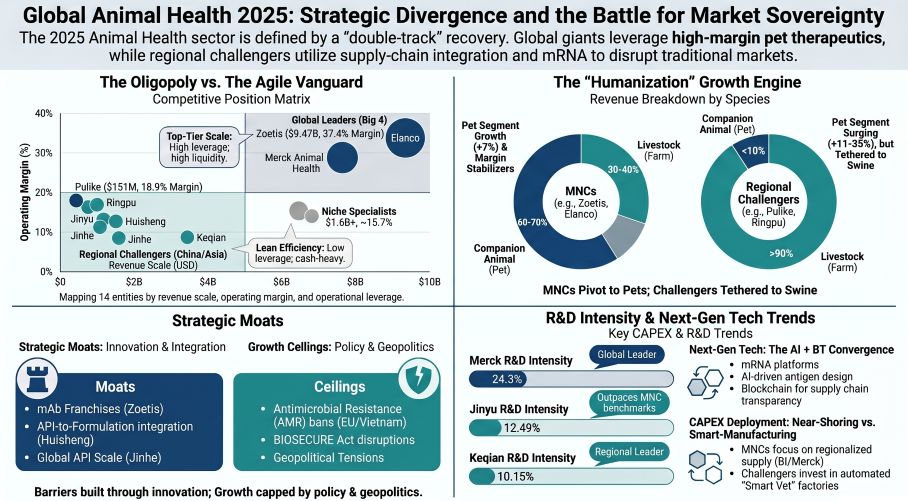

Forensic Analysis of Segmental Profitability & Margin Architecture

Forensic Analysis of Segmental Profitability & Margin Architecture

The 2025 financial disclosures reveal a stark stratification in operational leverage and human capital efficiency. Multinational giants generating over 50% of revenue from companion animals exhibit pristine earnings conversion, whereas heavily livestock-exposed entities face severe margin compression.

* Zoetis (NYSE: ZTS) generated $9,467 million in total revenue, deriving an outsized 70% ($6,587 million) from companion animals. Driven by highly inelastic demand for Apoquel and Simparica Trio, Zoetis achieved a sector-leading 37.4% core operating margin and an earnings quality ratio of 1.09x (OCF of $2,904 million vs. Net Income of $2,673 million).

* Merck & Co. (NYSE: MRK) Animal Health posted $6,354 million in revenue, supported by the $1.1 billion Bravecto franchise. Operating at a 33.5% margin, the division leverages its massive $15.79 billion group-level R&D engine (24.3% of total revenue) to sustain market dominance.

* Elanco (NYSE: ELAN) reflects severe negative operational leverage. Despite $4,715 million in revenue, heavy amortization ($543 million) and persistent restructuring charges ($237 million) resulted in a $232 million net loss.

* Pulike Biological Engineering (SHA: 603566) demonstrates the high-margin potential of localized import substitution. While operating from a smaller $151.6 million base, its pet vaccine gross margins reached an exceptional 64.37%, converting net income to cash seamlessly at 0.99x.

Table Segmental Financial & Innovation Inventory (FY2025)

Physical Supply Chain Audit & Geo-Economic Moats

To mitigate geopolitical fragmentation and climate-induced disruptions, the sector is aggressively regionalizing its manufacturing footprint. However, the over-reliance on concentrated Active Pharmaceutical Ingredients (APIs) and fragile Contract Manufacturing Organizations (CMOs) exposes severe operational vulnerabilities.

* Near-Shoring vs. CMO Insolvency: Elanco’s heavy reliance on a 140+ CMO network materialized as a severe downside risk when its Tier-1 UK partner, TriRx Speke, entered trading administration. To avert a catastrophic supply collapse, Elanco was forced to deploy $36 million in unplanned capital to acquire the facility outright. Furthermore, Elanco is executing a strategic footprint optimization, completely shutting down its Kansas City Tier-1 Facility by 2026.

* Tariff Defense & Localization: Merck reached a strategic agreement with the U.S. Department of Commerce to delay Section 232 tariffs, allowing it to reshore manufacturing to its Rahway, New Jersey Headquarters. Concurrently, Virbac is expanding its Carros Bio 5 factory in France to protect its European margins from severe FX volatility in emerging markets.

* The Chinese Cost-Leadership Moat: Domestic firms are exploiting plunging domestic agricultural commodity prices to build insurmountable raw-material cost advantages. Jinhe Biotechnology leveraged its footprint in Inner Mongolia to capitalize on a 5.03% drop in corn prices and a 20.64% drop in coal prices, effectively dominating the global Chlortetracycline supply chain. Similarly, Wuhan Huisheng relies on a vertically integrated API-to-formulation infrastructure across its Wuhan, Yingcheng, and Changsha facilities to shield its macrolide pipeline from external price shocks.

HDIN Institutional Perspective: The Inventory Trap & Synthesized Liquidity

While the Street largely praises the structural pivot toward companion animals, our forensic audit of the 2025 balance sheets reveals a critical divergence between reported liquidity and core operational cash generation that consensus estimates have not priced in.

We actively challenge the management narratives surrounding "forecasted demand" used to justify massive working capital bloat. Zoetis and Elanco reported extreme inventory expansions to $2,430 million and $1,737 million, respectively. In a sector where biological products possess strict expiration dates, this is a leading indicator of future obsolescence write-downs. We view Virbac’s $11.08 million net inventory write-down in 2025 as the canary in the coal mine for the broader industry.

Furthermore, Elanco’s reported $560 million in operating cash flow is an accounting mirage; this liquidity was heavily subsidized by a $295 million cash injection from Blackstone in exchange for selling future royalty rights to the human medical treatment XDEMVY through 2033. Sacrificing future high-margin assets to service current debt loads indicates a structural cash strain. Compounded by the looming implementation of the U.S. BIOSECURE Act—which threatens to sever access to cost-efficient Chinese CROs—multinational margins remain highly vulnerable to supply-side exogenous shocks over the next 24 months.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Global Animal Health 2025: Strategic Divergence and the Battle for Market Sovereignty

Forensic Analysis of Segmental Profitability & Margin ArchitectureThe 2025 financial disclosures reveal a stark stratification in operational leverage and human capital efficiency. Multinational giants generating over 50% of revenue from companion animals exhibit pristine earnings conversion, whereas heavily livestock-exposed entities face severe margin compression.

* Zoetis (NYSE: ZTS) generated $9,467 million in total revenue, deriving an outsized 70% ($6,587 million) from companion animals. Driven by highly inelastic demand for Apoquel and Simparica Trio, Zoetis achieved a sector-leading 37.4% core operating margin and an earnings quality ratio of 1.09x (OCF of $2,904 million vs. Net Income of $2,673 million).

* Merck & Co. (NYSE: MRK) Animal Health posted $6,354 million in revenue, supported by the $1.1 billion Bravecto franchise. Operating at a 33.5% margin, the division leverages its massive $15.79 billion group-level R&D engine (24.3% of total revenue) to sustain market dominance.

* Elanco (NYSE: ELAN) reflects severe negative operational leverage. Despite $4,715 million in revenue, heavy amortization ($543 million) and persistent restructuring charges ($237 million) resulted in a $232 million net loss.

* Pulike Biological Engineering (SHA: 603566) demonstrates the high-margin potential of localized import substitution. While operating from a smaller $151.6 million base, its pet vaccine gross margins reached an exceptional 64.37%, converting net income to cash seamlessly at 0.99x.

Table Segmental Financial & Innovation Inventory (FY2025)

| Entity | 2025 Revenue (USD) | Operating Margin | Revenue per Employee (USD) | Core Growth Vector & Proprietary Technology |

|---|---|---|---|---|

| Zoetis | $9,467M | 37.4% | $652,896 | AI Diagnostics (Vetscan Imagyst); monoclonal antibodies (Librela, Solensia) |

| Merck & Co. | $6,354M (Animal Health) | 33.5% | $866,813 (Group) | Annual injectables (Bravecto Quantum); JAK inhibitors (Numelvi) |

| Boehringer Ingelheim | $5,512M (Animal Health) | N/A | $577,319 | Parasiticides (NexGard COMBO); Quantum AI R&D Lab (BI X) |

| Elanco Animal Health | $4,715M | 16.9% | $476,262 | Broad-spectrum oral therapeutics (Credelio Quattro); omnichannel distribution |

| Virbac | $1,656M | 15.7% | $257,063 | Niche therapeutics (Thyronorm); clinical pet food (Vikaly) |

| Ringpu Biology | $472.8M | N/A | N/A | Downstream integration (Ruipai Pet Hospitals); mRNA platforms |

Physical Supply Chain Audit & Geo-Economic Moats

To mitigate geopolitical fragmentation and climate-induced disruptions, the sector is aggressively regionalizing its manufacturing footprint. However, the over-reliance on concentrated Active Pharmaceutical Ingredients (APIs) and fragile Contract Manufacturing Organizations (CMOs) exposes severe operational vulnerabilities.

* Near-Shoring vs. CMO Insolvency: Elanco’s heavy reliance on a 140+ CMO network materialized as a severe downside risk when its Tier-1 UK partner, TriRx Speke, entered trading administration. To avert a catastrophic supply collapse, Elanco was forced to deploy $36 million in unplanned capital to acquire the facility outright. Furthermore, Elanco is executing a strategic footprint optimization, completely shutting down its Kansas City Tier-1 Facility by 2026.

* Tariff Defense & Localization: Merck reached a strategic agreement with the U.S. Department of Commerce to delay Section 232 tariffs, allowing it to reshore manufacturing to its Rahway, New Jersey Headquarters. Concurrently, Virbac is expanding its Carros Bio 5 factory in France to protect its European margins from severe FX volatility in emerging markets.

* The Chinese Cost-Leadership Moat: Domestic firms are exploiting plunging domestic agricultural commodity prices to build insurmountable raw-material cost advantages. Jinhe Biotechnology leveraged its footprint in Inner Mongolia to capitalize on a 5.03% drop in corn prices and a 20.64% drop in coal prices, effectively dominating the global Chlortetracycline supply chain. Similarly, Wuhan Huisheng relies on a vertically integrated API-to-formulation infrastructure across its Wuhan, Yingcheng, and Changsha facilities to shield its macrolide pipeline from external price shocks.

HDIN Institutional Perspective: The Inventory Trap & Synthesized Liquidity

While the Street largely praises the structural pivot toward companion animals, our forensic audit of the 2025 balance sheets reveals a critical divergence between reported liquidity and core operational cash generation that consensus estimates have not priced in.

We actively challenge the management narratives surrounding "forecasted demand" used to justify massive working capital bloat. Zoetis and Elanco reported extreme inventory expansions to $2,430 million and $1,737 million, respectively. In a sector where biological products possess strict expiration dates, this is a leading indicator of future obsolescence write-downs. We view Virbac’s $11.08 million net inventory write-down in 2025 as the canary in the coal mine for the broader industry.

Furthermore, Elanco’s reported $560 million in operating cash flow is an accounting mirage; this liquidity was heavily subsidized by a $295 million cash injection from Blackstone in exchange for selling future royalty rights to the human medical treatment XDEMVY through 2033. Sacrificing future high-margin assets to service current debt loads indicates a structural cash strain. Compounded by the looming implementation of the U.S. BIOSECURE Act—which threatens to sever access to cost-efficient Chinese CROs—multinational margins remain highly vulnerable to supply-side exogenous shocks over the next 24 months.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."