Life Sciences 2026 Outlook: Why FamiCord and Revvity Diverge on Capital Allocation Amid Shifting Demographics and Regional Regulation

Date : 2026-05-14

Reading : 146

Facing a severe drop in the European birth rate to 1.35 and tightening diagnostic policies in Asia, FamiCord AG and Revvity deploy divergent capital defenses. Revvity leverages B2B technology stacks for global recurring revenue, while FamiCord shifts its center of gravity from Western Europe to Poland and the GCC. For institutional LPs, the core risk is not fully captured in the income statement, but hidden within surging contract assets and geographic collection delays driven by business model transitions and macroeconomic headwinds.

Figure Strategic Analysis of Global Stem Cell Banking & Life Sciences (FY2025)

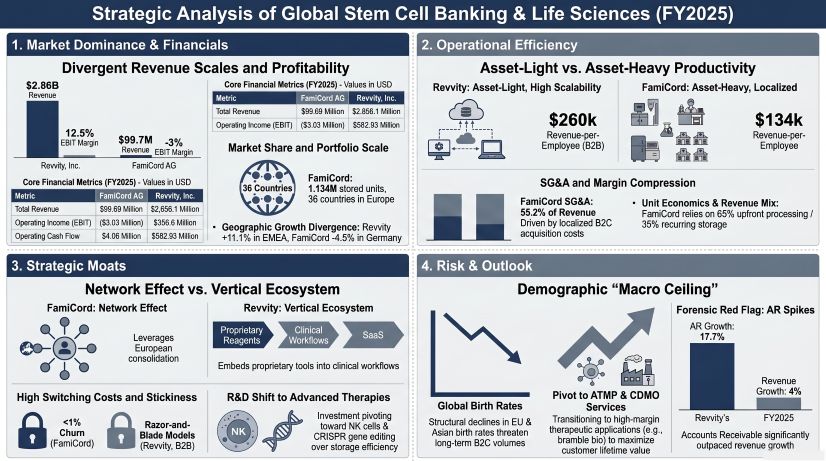

Forensic Financials & Segmental Inventory

Forensic Financials & Segmental Inventory

Based on a Forensic Analysis of the 2025 fiscal disclosures, the unit economics and operational leverage of the two entities reveal a structural schism. Revvity exhibits a high-leverage software and consumables model, whereas FamiCord remains constrained within a capital-intensive B2C framework burdened by high fixed costs and elevated customer acquisition costs (CAC).

Table : FY2025 Quantitative Inventory

(Amounts in USD Millions, FamiCord converted at 1 EUR = 1.1306 USD)

Dynamic Financial Structure Breakdown:

* Price-Mix Variance: FamiCord AG experienced a massive 45% surge in Contract Assets to $34.46M, alongside a 13% increase in trade receivables to $17.87M. This directly reflects management's strategy to force-migrate clients from prepaid contracts to an annual subscription model. With an estimated CAC of $428 per new B2C storage contract across 68,000 new units, heavy sales expenditures ($29.14M) continue to suppress EBIT.

* Regional Accounts Receivable Anomalies: While NYSE: RVTY posted a modest 4% top-line growth, its Accounts Receivable (AR) spiked by 17.7% to $744.67M. Management explicitly attributed this $96.8M working capital drain to collection delays in China (part of the broader APAC region which contracted by -1.8% to $775.1M).

* Internal Capitalization Tactics: Revvity’s capitalized internal-use software jumped 32.7% to $134.31M. This accounting treatment smooths current-period expenses and demands rigorous scrutiny, especially considering the firm recorded a $22.8M impairment on internal-use software in 2024.

Supply Chain Audit & Geo-Economic Moat

The geographic footprint of physical infrastructure and clinical nodes dictates each company's resilience against geopolitical volatility and localized demand shocks.

FamiCord AG: Regional Pivot & Physical Asset Network

FamiCord operates a dense network of 15 proprietary laboratories across 11 countries. Its geo-economic dominance is shifting drastically: as the German market contracted by -4.5% to $16.32M, Poland has officially usurped the DACH region as its primary revenue anchor, generating $28.06M (+22.1%).

* Facility-Level Engineering Optimization: At its Türkiye facility, FamiCord executed targeted HVAC airflow optimizations. By recalibrating variable air volume (VAV) dampers and variable frequency drives (VFDs), the company eliminated climate-related lab downtime and reduced system alarms by 70%, actively fortifying its cryogenic liquid nitrogen dependency.

* Clinical Monetization Nodes: Moving beyond passive storage, FamiCord is validating its moat via clinical utility (over 8,000 patients treated). In 2025, 20 children received Expanded Access Program (EAP) treatments for ASD at the University Children’s Hospital in Lublin. The company also advanced cord blood NK cell trials for solid tumors at the Medical University of Zielona Góra, and progressed the "REPAIR" ischemic stroke project (2023-2026) alongside Universidade da Beira Interior and Universidade de Coimbra in Portugal.

* Regulatory Hard-Landing Preparation: In anticipation of the EU SoHO Regulation (EU 2024/1938) slated for full enforcement by August 2027, FamiCord is leveraging its bramble.bio CDMO brand to impose stringent ISO 14001 environmental and quality site-audits on upstream suppliers.

Revvity: Exclusive IP & The Single-Supplier Bottleneck

Revvity’s moat relies on FDA-cleared clinical workflow loops, anchored by its global Revvity Omics laboratory network and proprietary instruments like DELFIA Xpress and chemagic 360.

* Highly Locked Physical Dependencies: Because of the proprietary nature of its IP—such as the Pin-point® base editing platform and LentiBOOST® technology—Revvity is highly vulnerable to single or limited Tier-1 upstream suppliers. To hedge against geopolitical tariffs and logistical force majeure, the company is forced into heavy asset-defensive strategies, securing multi-year contracts with no minimum purchase requirements and accumulating excess safety stock of critical biomaterials.

HDIN Institutional Perspective: Liquidity Vacuums vs. Automated Receivables Risk

While FamiCord touts a sub-1% B2C customer churn rate and a 40% to 60% renewal rate on maturing 20-year prepaid contracts, these metrics mask a critical structural vulnerability: the 45% spike in Contract Assets indicates that the transition to a subscription model is severely draining near-term liquidity. Operating cash flow (OCF) collapsed to a mere $4.06M in 2025. Coupled with a $5.66M goodwill impairment, this suggests the underutilization of heavy fixed assets—driven by Western Europe’s demographic decline—is a far more pressing threat than the Street has priced in.

Conversely, the market currently awards a valuation premium to Revvity's $356.6M operating profit and its 2.4x OCF conversion rate ($582.93M / $241.20M). However, this leverage, built on high-throughput automated instruments and consumables, is encountering regional friction. With revenue growing at just 4% while AR balloons by 17.7%, Revvity's APAC distribution channels appear to be transferring their inventory destocking and collection pressures directly onto Revvity's balance sheet. For institutional capital allocating across the life sciences sector for the 2026 fiscal year, these regional collection delays and the deferred commercialization timeline of "new cell types" R&D must be aggressively factored into valuation discount models.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Strategic Analysis of Global Stem Cell Banking & Life Sciences (FY2025)

Forensic Financials & Segmental InventoryBased on a Forensic Analysis of the 2025 fiscal disclosures, the unit economics and operational leverage of the two entities reveal a structural schism. Revvity exhibits a high-leverage software and consumables model, whereas FamiCord remains constrained within a capital-intensive B2C framework burdened by high fixed costs and elevated customer acquisition costs (CAC).

Table : FY2025 Quantitative Inventory

(Amounts in USD Millions, FamiCord converted at 1 EUR = 1.1306 USD)

| Financial / Operational Metric | Revvity, Inc. | FamiCord AG |

|---|---|---|

| Total Revenue | $2,856.1M (+4.0%) | $99.69M (+7.3% / EUR 88.17M) |

| Core Segment Contribution | Life Sciences: $1,431.1M (50.1%)Reproductive Health: $555.0M (19.4%) | Cell Storage: $87.7M (88.0%)Processing: $59.77M / Storage: $32.40M |

| Gross Margin (GM) | 54.8% (contracted 104 bps) | 53.4% (Cost of Sales ratio declined to 46.6%) |

| Operating Income (EBIT) | $356.6M (12.5% margin) | -$3.03M (Operating Loss) |

| Net Income / Operating Cash Flow | $241.20M / $582.93M | -$7.59M / +$4.06M |

| SG&A Expenses | $991.9M (34.7% of Revenue) | $55.0M (55.2% of Revenue) |

| R&D Outlays | $215.84M (7.6% of Revenue) | $0.90M (0.9% of Revenue) |

| Revenue per Employee | $259,645 (approx. 11,000 employees) | $134,353 (742 employees) |

| Capital Expenditures (CapEx) | $73.5M | $14.02M (PPE: $4.64M; M&A: $9.04M) |

| Depreciation & Amortization (D&A) | $405.34M ($335.6M intangible amortization) | $15.01M (plus $5.66M goodwill impairment) |

| Deferred Revenue | $224.8M | $89.75M (Long-term: $76.17M / Short-term: $13.58M) |

* Price-Mix Variance: FamiCord AG experienced a massive 45% surge in Contract Assets to $34.46M, alongside a 13% increase in trade receivables to $17.87M. This directly reflects management's strategy to force-migrate clients from prepaid contracts to an annual subscription model. With an estimated CAC of $428 per new B2C storage contract across 68,000 new units, heavy sales expenditures ($29.14M) continue to suppress EBIT.

* Regional Accounts Receivable Anomalies: While NYSE: RVTY posted a modest 4% top-line growth, its Accounts Receivable (AR) spiked by 17.7% to $744.67M. Management explicitly attributed this $96.8M working capital drain to collection delays in China (part of the broader APAC region which contracted by -1.8% to $775.1M).

* Internal Capitalization Tactics: Revvity’s capitalized internal-use software jumped 32.7% to $134.31M. This accounting treatment smooths current-period expenses and demands rigorous scrutiny, especially considering the firm recorded a $22.8M impairment on internal-use software in 2024.

Supply Chain Audit & Geo-Economic Moat

The geographic footprint of physical infrastructure and clinical nodes dictates each company's resilience against geopolitical volatility and localized demand shocks.

FamiCord AG: Regional Pivot & Physical Asset Network

FamiCord operates a dense network of 15 proprietary laboratories across 11 countries. Its geo-economic dominance is shifting drastically: as the German market contracted by -4.5% to $16.32M, Poland has officially usurped the DACH region as its primary revenue anchor, generating $28.06M (+22.1%).

* Facility-Level Engineering Optimization: At its Türkiye facility, FamiCord executed targeted HVAC airflow optimizations. By recalibrating variable air volume (VAV) dampers and variable frequency drives (VFDs), the company eliminated climate-related lab downtime and reduced system alarms by 70%, actively fortifying its cryogenic liquid nitrogen dependency.

* Clinical Monetization Nodes: Moving beyond passive storage, FamiCord is validating its moat via clinical utility (over 8,000 patients treated). In 2025, 20 children received Expanded Access Program (EAP) treatments for ASD at the University Children’s Hospital in Lublin. The company also advanced cord blood NK cell trials for solid tumors at the Medical University of Zielona Góra, and progressed the "REPAIR" ischemic stroke project (2023-2026) alongside Universidade da Beira Interior and Universidade de Coimbra in Portugal.

* Regulatory Hard-Landing Preparation: In anticipation of the EU SoHO Regulation (EU 2024/1938) slated for full enforcement by August 2027, FamiCord is leveraging its bramble.bio CDMO brand to impose stringent ISO 14001 environmental and quality site-audits on upstream suppliers.

Revvity: Exclusive IP & The Single-Supplier Bottleneck

Revvity’s moat relies on FDA-cleared clinical workflow loops, anchored by its global Revvity Omics laboratory network and proprietary instruments like DELFIA Xpress and chemagic 360.

* Highly Locked Physical Dependencies: Because of the proprietary nature of its IP—such as the Pin-point® base editing platform and LentiBOOST® technology—Revvity is highly vulnerable to single or limited Tier-1 upstream suppliers. To hedge against geopolitical tariffs and logistical force majeure, the company is forced into heavy asset-defensive strategies, securing multi-year contracts with no minimum purchase requirements and accumulating excess safety stock of critical biomaterials.

HDIN Institutional Perspective: Liquidity Vacuums vs. Automated Receivables Risk

While FamiCord touts a sub-1% B2C customer churn rate and a 40% to 60% renewal rate on maturing 20-year prepaid contracts, these metrics mask a critical structural vulnerability: the 45% spike in Contract Assets indicates that the transition to a subscription model is severely draining near-term liquidity. Operating cash flow (OCF) collapsed to a mere $4.06M in 2025. Coupled with a $5.66M goodwill impairment, this suggests the underutilization of heavy fixed assets—driven by Western Europe’s demographic decline—is a far more pressing threat than the Street has priced in.

Conversely, the market currently awards a valuation premium to Revvity's $356.6M operating profit and its 2.4x OCF conversion rate ($582.93M / $241.20M). However, this leverage, built on high-throughput automated instruments and consumables, is encountering regional friction. With revenue growing at just 4% while AR balloons by 17.7%, Revvity's APAC distribution channels appear to be transferring their inventory destocking and collection pressures directly onto Revvity's balance sheet. For institutional capital allocating across the life sciences sector for the 2026 fiscal year, these regional collection delays and the deferred commercialization timeline of "new cell types" R&D must be aggressively factored into valuation discount models.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."