Virtuix: Hardware-as-a-Platform Pivot Near Zhuhai Assembly Hub as Draconian Covenants Signal Q4 2026 Liquidity Cliff

Date : 2026-05-14

Reading : 103

Despite a 49% YoY revenue surge driven by the Omni One hardware cycle, Virtuix faces a critical December 2026 cash cliff. The company operates under an active auditor "going concern" warning with an accumulated deficit of $69.38 million. Institutional viability relies entirely on a heavily conditioned $50 million Streeterville equity facility mandating a strict $95 million market capitalization minimum. With all intellectual property pledged as collateral and a high-risk supply chain centralized in Guangdong, China, LPs must weigh 73.52% founder-controlled governance against the theoretical $128.3 million maximum-capacity revenue threshold of its proprietary active-VR ecosystem.

Figure Virtuix (VTlX) Investment Case: The Omni Ecosystem

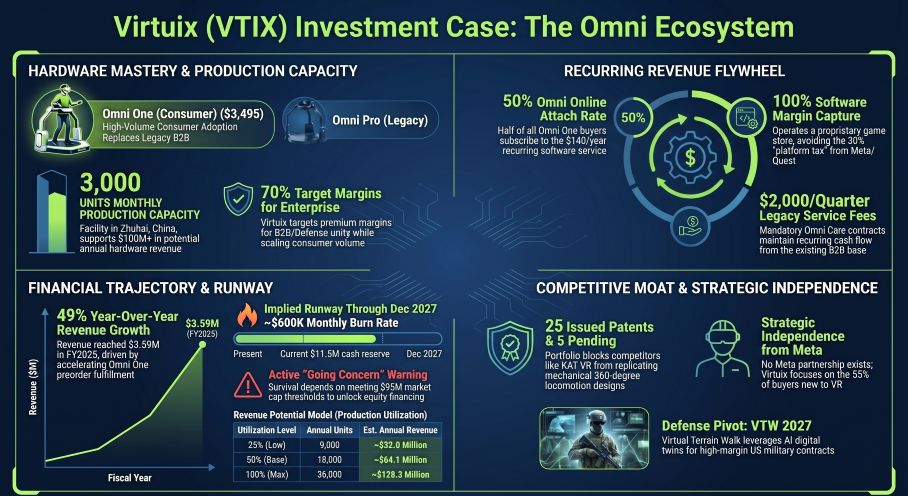

Segmental Inventory & Unit Economics Architecture

Segmental Inventory & Unit Economics Architecture

A structural audit of the FY25 and TTM financial disclosures reveals a transition from legacy B2B hardware (Omni Pro, Omni Arena) to a consumer-facing, high-margin software annuity model. However, operating leverage remains constrained by high Customer Acquisition Costs (CAC) and related-party capital obligations.

1. Quantitative Performance & Capital Runway

* FY25 Core Metrics: Total Revenue printed at $3,590,438. Net Loss stood at $(14,648,792).

* FY25 EBITDA Bridge: $(13,719,400), calculated as $(14,648,792) Net Loss + $369,420 Interest Expense - $1,372 Interest Income + $78,955 Tax Provision + $482,389 D&A.

* TTM 2025 Improvement: TTM Revenue expanded to $4,460,314. TTM Net Loss narrowed to $(9,517,026), generating a TTM EBITDA of $(7,389,938), primarily reflecting the roll-off of ~$4.7 million in stock-based compensation and fulfilled discounted unit deliveries.

* Runway Paradox: Post-listing cash of ~$11.5 million against a ~$600,000 monthly burn mathematically implies a 19.16-month runway (sustaining operations to December 2027). However, management explicitly caps guaranteed runway at December 31, 2026, due to structurally embedded covenant drains and debt redemptions.

2. Unit Economics & Ecosystem Monetization

* Consumer Hardware Margin: The flagship Omni One retails at $3,495 (targeting a 40% gross margin), with a headset-free "Core" variant at $2,595.

* Enterprise/Commercial Margin: The B2B variant retails at $4,995 (targeting a 70% gross margin). Legacy systems harvest an annuity via Omni Care maintenance ($2,000/quarter) and gameplay credits ($0.10/minute).

* Software Attach Rate: 50% of consumers acquire the Omni Online subscription ($14/month or $140/year). Proprietary platform games run $19.99 to $44.99 per title. Total addressable market benchmarks 17 million console-owning US households earning over $75,000.

3. Maximum Capacity Yield Scenarios (2026–2027)

Operating at a 3,000-unit/month (36,000 annually) production ceiling dictates the following cohort revenue models:

* Scenario A (25% Utilization / 9,000 units): $31.4M hardware + $630k software = $32.0M Total.

* Scenario B (50% Utilization / 18,000 units): $62.9M hardware + $1.26M software = $64.1M Total.

* Scenario C (100% Utilization / 36,000 units): $125.8M hardware + $2.52M software = $128.3M Total.

4. Corporate Governance & Balance Sheet Drains

* Founder Control: CEO Jan Goetgeluk holds 4,000,000 Class B shares (20 votes per share), securing 73.52% of voting power and legally exempting Virtuix from standard independent board requirements.

* Atypical Compensation Structure: The COO holds 1,500,000 vested options featuring a highly unusual "zero-cost" cash bonus equivalent to the strike price upon exercise, structurally transferring the capital burden to the company. Base salaries for FY26 increased to $350,000, supplemented by a $50,000 listing bonus, a $70,000 performance bonus, and a 375,000 RSU grant valued at >$2.5 million.

* Historical RPT Liquidity: Pre-listing operations relied on 18% high-interest bridge notes from insiders ($50,000 from the CEO, $167,678 from his mother, and $100,000 from a board member), all cleared utilizing $3.34 million in Streeterville Debt Financing and $217,678 in related-party payoffs. Unfulfilled $200 preorders were converted into $448,087 of gift card liabilities, neutralizing future cash flow contributions from the backlog.

Supply Chain Audit & Geo-Economic Moat

Virtuix exhibits a highly asymmetric geographic footprint, heavily weighted toward US-based consumer sales and defense testing, yet utterly reliant on Asian manufacturing infrastructure.

Physical Dependencies & Tariff Defenses:

Final QA and assembly are localized at a primary facility in Zhuhai, Guangdong, China, aggregating components from a fragmented network of over 50 Tier-1 and Tier-2 suppliers. Critical bottlenecks include a single-source dependency for the integrated VR headsets. To combat margin erosion from escalating US import tariffs, Virtuix activated Virtuix Manufacturing Taiwan Ltd., establishing a strategic fail-safe capable of leveraging a reduced 15% tariff rate.

Defense Market Realignment (VTW):

The strategic entry into the B2G defense sector via the Virtual Terrain Walk (VTW) system introduces strict federal procurement frictions. While test units have successfully penetrated the US Air Force Academy, YokoWERX, West Point, and the US Marine Corps, mass deployment in FY 2027 is bound by the *Buy American Act* and the *Berry Amendment*. Scaling this high-margin vertical will forcibly mandate a partial decoupling from the Zhuhai supply chain to meet domestic sourcing quotas.

Intellectual Property Defensibility:

The firm's commercial moat is anchored by 25 granted patents, 14 trademarks, and 5 pending patents structurally blocking competitors like KAT VR from deploying low-friction concave mechanics. However, Virtuix explicitly notes a lack of sufficient cash reserves to actively litigate infringement, elevating operational risk against better-capitalized Asian hardware clones.

HDIN Institutional Perspective: The Illusory 19-Month Runway vs. Hard Debt Covenants

While rudimentary baseline math suggests post-IPO liquidity sustains operations for 19.16 months, we fundamentally challenge this duration. The financial architecture confirms a hard cash cliff at December 31, 2026. Institutional investors are mispricing the aggressive mechanisms within the Streeterville agreements.

Beginning July 1, 2026, the $2.68 million Exchange Note empowers Streeterville to unilaterally demand mandatory monthly redemptions of up to $111,738.27, severely accelerating the $600,000 monthly burn. More critically, survival requires continuous drawdown from the remaining $42 million Equity Purchase Agreement, which is instantly paralyzed if Virtuix’s market capitalization falls below $95,000,000 or if the 20/60-day median trading volume dips below $350,000. Compounded by the zero-cost executive option triggers designed to drain cash, Virtuix is operating a "drip-feed" financing model entirely contingent on flawless retail equity execution. The company is currently undercapitalized to independently reach its stated FY 2027 defense revenue inflection.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Virtuix (VTlX) Investment Case: The Omni Ecosystem

Segmental Inventory & Unit Economics Architecture A structural audit of the FY25 and TTM financial disclosures reveals a transition from legacy B2B hardware (Omni Pro, Omni Arena) to a consumer-facing, high-margin software annuity model. However, operating leverage remains constrained by high Customer Acquisition Costs (CAC) and related-party capital obligations.

1. Quantitative Performance & Capital Runway

* FY25 Core Metrics: Total Revenue printed at $3,590,438. Net Loss stood at $(14,648,792).

* FY25 EBITDA Bridge: $(13,719,400), calculated as $(14,648,792) Net Loss + $369,420 Interest Expense - $1,372 Interest Income + $78,955 Tax Provision + $482,389 D&A.

* TTM 2025 Improvement: TTM Revenue expanded to $4,460,314. TTM Net Loss narrowed to $(9,517,026), generating a TTM EBITDA of $(7,389,938), primarily reflecting the roll-off of ~$4.7 million in stock-based compensation and fulfilled discounted unit deliveries.

* Runway Paradox: Post-listing cash of ~$11.5 million against a ~$600,000 monthly burn mathematically implies a 19.16-month runway (sustaining operations to December 2027). However, management explicitly caps guaranteed runway at December 31, 2026, due to structurally embedded covenant drains and debt redemptions.

2. Unit Economics & Ecosystem Monetization

* Consumer Hardware Margin: The flagship Omni One retails at $3,495 (targeting a 40% gross margin), with a headset-free "Core" variant at $2,595.

* Enterprise/Commercial Margin: The B2B variant retails at $4,995 (targeting a 70% gross margin). Legacy systems harvest an annuity via Omni Care maintenance ($2,000/quarter) and gameplay credits ($0.10/minute).

* Software Attach Rate: 50% of consumers acquire the Omni Online subscription ($14/month or $140/year). Proprietary platform games run $19.99 to $44.99 per title. Total addressable market benchmarks 17 million console-owning US households earning over $75,000.

3. Maximum Capacity Yield Scenarios (2026–2027)

Operating at a 3,000-unit/month (36,000 annually) production ceiling dictates the following cohort revenue models:

* Scenario A (25% Utilization / 9,000 units): $31.4M hardware + $630k software = $32.0M Total.

* Scenario B (50% Utilization / 18,000 units): $62.9M hardware + $1.26M software = $64.1M Total.

* Scenario C (100% Utilization / 36,000 units): $125.8M hardware + $2.52M software = $128.3M Total.

4. Corporate Governance & Balance Sheet Drains

* Founder Control: CEO Jan Goetgeluk holds 4,000,000 Class B shares (20 votes per share), securing 73.52% of voting power and legally exempting Virtuix from standard independent board requirements.

* Atypical Compensation Structure: The COO holds 1,500,000 vested options featuring a highly unusual "zero-cost" cash bonus equivalent to the strike price upon exercise, structurally transferring the capital burden to the company. Base salaries for FY26 increased to $350,000, supplemented by a $50,000 listing bonus, a $70,000 performance bonus, and a 375,000 RSU grant valued at >$2.5 million.

* Historical RPT Liquidity: Pre-listing operations relied on 18% high-interest bridge notes from insiders ($50,000 from the CEO, $167,678 from his mother, and $100,000 from a board member), all cleared utilizing $3.34 million in Streeterville Debt Financing and $217,678 in related-party payoffs. Unfulfilled $200 preorders were converted into $448,087 of gift card liabilities, neutralizing future cash flow contributions from the backlog.

Supply Chain Audit & Geo-Economic Moat

Virtuix exhibits a highly asymmetric geographic footprint, heavily weighted toward US-based consumer sales and defense testing, yet utterly reliant on Asian manufacturing infrastructure.

Physical Dependencies & Tariff Defenses:

Final QA and assembly are localized at a primary facility in Zhuhai, Guangdong, China, aggregating components from a fragmented network of over 50 Tier-1 and Tier-2 suppliers. Critical bottlenecks include a single-source dependency for the integrated VR headsets. To combat margin erosion from escalating US import tariffs, Virtuix activated Virtuix Manufacturing Taiwan Ltd., establishing a strategic fail-safe capable of leveraging a reduced 15% tariff rate.

Defense Market Realignment (VTW):

The strategic entry into the B2G defense sector via the Virtual Terrain Walk (VTW) system introduces strict federal procurement frictions. While test units have successfully penetrated the US Air Force Academy, YokoWERX, West Point, and the US Marine Corps, mass deployment in FY 2027 is bound by the *Buy American Act* and the *Berry Amendment*. Scaling this high-margin vertical will forcibly mandate a partial decoupling from the Zhuhai supply chain to meet domestic sourcing quotas.

Intellectual Property Defensibility:

The firm's commercial moat is anchored by 25 granted patents, 14 trademarks, and 5 pending patents structurally blocking competitors like KAT VR from deploying low-friction concave mechanics. However, Virtuix explicitly notes a lack of sufficient cash reserves to actively litigate infringement, elevating operational risk against better-capitalized Asian hardware clones.

HDIN Institutional Perspective: The Illusory 19-Month Runway vs. Hard Debt Covenants

While rudimentary baseline math suggests post-IPO liquidity sustains operations for 19.16 months, we fundamentally challenge this duration. The financial architecture confirms a hard cash cliff at December 31, 2026. Institutional investors are mispricing the aggressive mechanisms within the Streeterville agreements.

Beginning July 1, 2026, the $2.68 million Exchange Note empowers Streeterville to unilaterally demand mandatory monthly redemptions of up to $111,738.27, severely accelerating the $600,000 monthly burn. More critically, survival requires continuous drawdown from the remaining $42 million Equity Purchase Agreement, which is instantly paralyzed if Virtuix’s market capitalization falls below $95,000,000 or if the 20/60-day median trading volume dips below $350,000. Compounded by the zero-cost executive option triggers designed to drain cash, Virtuix is operating a "drip-feed" financing model entirely contingent on flawless retail equity execution. The company is currently undercapitalized to independently reach its stated FY 2027 defense revenue inflection.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."