INNIO: Aggressive Capacity Expansion Near Trenton and Waukesha as 2.8x Book-to-Bill Ratio Signals Structural Boom in North American AI Data Center Microgrids

Date : 2026-05-14

Reading : 83

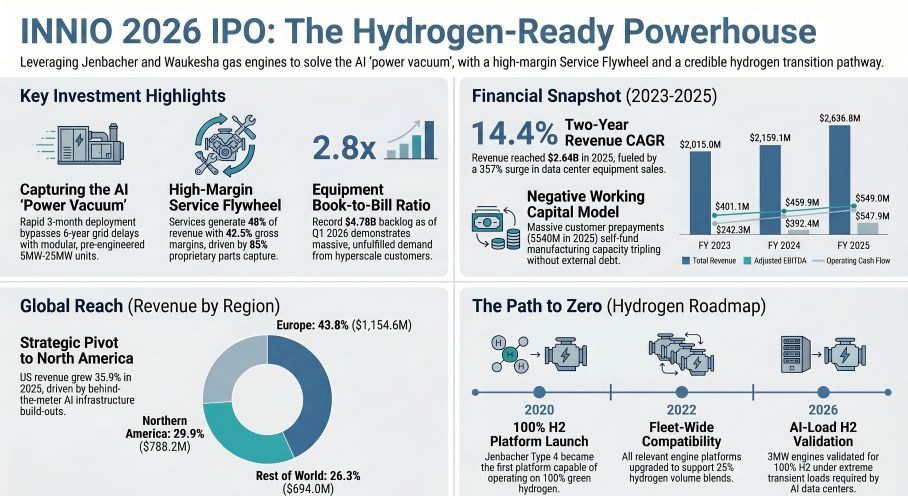

INNIO’s massive $723.8 million FY2025 dividend recapitalization via its private equity sponsors (Advent/ADIA) exposes this IPO as a liquidity-driven exit. Yet, institutional LPs cannot ignore the underlying fundamentals: with US and European grid interconnection delays exceeding six years, AI data centers are aggressively pivoting to behind-the-meter microgrids. The company's 2.8x book-to-bill ratio, $4.78 billion backlog, and 100% hydrogen-ready engine platforms construct a formidable capital barrier and a highly insulated, high-margin service flywheel that the Street is currently mispricing.

Figure INNIO 2026 lPO: The Hydrogen-Ready Powerhouse

Forensic Financials & Segmental Inventory

Forensic Financials & Segmental Inventory

Through a Forensic Analysis of INNIO’s balance sheet and income statements, the business model exhibits a textbook "razor and blade" logic. Front-end equipment sales are aggressively capturing market share during the AI infrastructure power vacuum, while true profit retention relies on high-friction Long-Term Service Agreements (LTSAs).

Revenue & Operating Leverage

* Total FY2025 Revenue: $2,636.8 million (+22.1% YoY, 14.4% 2-year CAGR).

* Adjusted EBITDA: $549.0 million (+19.4% YoY) with a 20.8% margin. Margins structurally compressed from 21.3% in 2024 (and further to 18.3% in Q1 2026) driven by capacity ramp-up costs and a higher equipment revenue mix.

* Cash Conversion: Decelerated from 81.2% in 2024 to 68.8% in 2025 (and 57.9% in Q1 2026), reflecting a deliberate $171.2 million self-funded CapEx spike to triple global manufacturing capacity.

* Free Cash Flow (FCF): Absolute FCF remains robust at $376.7 million, heavily sustained by $540.2 million in surging contract liabilities (customer pre-payments) as data centers rush to secure production slots.

Segmental Economics & Unit Profitability

Table FY2025 Segment Revenue Breakdown, Margin Profile, and Growth Drivers of Distributed Energy & Engine Solutions Business

* Capital Structure & Debt Leverage

* As of December 2025, Total Debt spiked to $2,658.8 million, pushing the Net Debt to Adjusted EBITDA ratio to an elevated 3.59x. Interest coverage remains secure at 3.36x.

* Core debt instruments include a €1,100.0 million Term Loan B, a $589.5 million Term Loan B-USD, and a newly syndicated $750.0 million Term Loan B2-USD specifically raised to fund the sponsor dividend recapitalization.

Supply Chain Audit & Geo-Economic Moat

INNIO executes a strict "local-for-local" manufacturing strategy across an approximately 7 million sq. ft. physical footprint to circumvent geopolitical friction (e.g., up to 200% US steel/aluminum tariffs and potential export controls on rare earth minerals from Taiwan, China, and mainland China).

* European Hubs (Centers of Excellence):

* Jenbach, Austria: The 2.1 million sq. ft. campus (1 million sq. ft. building) serves as the primary R&D, assembly, and testing epicenter for Jenbacher engines.

* Hall and Kapfenberg, Austria: Dedicated satellite facilities handling specialized components (69,000 sq. ft.) and spark plug manufacturing (45,000 sq. ft.).

* North American AI Compute Supply Chain:

* Welland, Ontario: Features 3.4 million sq. ft. of land housing massive spare capacity and assembly operations.

* Waukesha, Wisconsin: The 1.7 million sq. ft. site operates as the US corporate headquarters and primary engine remanufacturing hub.

* Strategic Chokepoints (Containerization): Newly launched, dedicated packaging centers in Trenton, New Jersey (93,000 sq. ft.) and Waller, Texas (65,000 sq. ft.) are optimized specifically for the rapid deployment of containerized data center solutions, drastically reducing "time-to-power."

* Physical Supply Chain Vulnerabilities: The firm relies on single-source suppliers for highly engineered components like cylinder head castings and heat exchangers. Furthermore, the myplant digital moat faces severe regulatory exposure under the EU AI Act (potential fines up to $39.57 million) and GDPR.

HDIN Institutional Perspective: An exceptionally high-quality asset executing a highly leveraged private equity exit disguised as a pure-play energy transition and AI infrastructure IPO

The Street is currently pricing INNIO as a "hydrogen-ready" derivative play on AI data center microgrids. We validate this operational moat: a 2.8x book-to-bill ratio and a $4.78 billion Q1 2026 backlog confirm that its modular 5 MW to 25 MW engines are successfully bypassing utility grid queues, directly curing the "power anxiety" of Tier-1 hyperscalers.

However, utilizing a differentiated viewpoint focused on forensic capital allocation, public market buyers are primarily funding the liquidity exit of private equity sponsors (Advent/ADIA). The $723.8 million capital repayment extracted in 2025 via the new $750 million Term Loan B2 thoroughly hollowed out historical retained earnings. The "Use of Proceeds" section in the S-1 functions as a blank check, lacking explicit commitments to deleverage the current 3.59x net debt ratio.

Furthermore, current risk models have not fully priced in extreme customer concentration: a single Energy-as-a-Service partner, VoltaGrid, accounted for an outsized 41% of total 2025 equipment orders. While the myplant ecosystem effectively locks customers into a 42.5% margin aftermarket, macroeconomic spark spread volatility and regulatory headwinds (e.g., New York's 2029 natural gas ban) suggest this is a high-reward, yet structurally vulnerable, industrial bet. Executive alignment remains bottlenecked by strict pro-rata sell-down rules, requiring institutional LPs to closely monitor the actual execution of the 2026 Incentive Award Plan post-IPO.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure INNIO 2026 lPO: The Hydrogen-Ready Powerhouse

Forensic Financials & Segmental InventoryThrough a Forensic Analysis of INNIO’s balance sheet and income statements, the business model exhibits a textbook "razor and blade" logic. Front-end equipment sales are aggressively capturing market share during the AI infrastructure power vacuum, while true profit retention relies on high-friction Long-Term Service Agreements (LTSAs).

Revenue & Operating Leverage

* Total FY2025 Revenue: $2,636.8 million (+22.1% YoY, 14.4% 2-year CAGR).

* Adjusted EBITDA: $549.0 million (+19.4% YoY) with a 20.8% margin. Margins structurally compressed from 21.3% in 2024 (and further to 18.3% in Q1 2026) driven by capacity ramp-up costs and a higher equipment revenue mix.

* Cash Conversion: Decelerated from 81.2% in 2024 to 68.8% in 2025 (and 57.9% in Q1 2026), reflecting a deliberate $171.2 million self-funded CapEx spike to triple global manufacturing capacity.

* Free Cash Flow (FCF): Absolute FCF remains robust at $376.7 million, heavily sustained by $540.2 million in surging contract liabilities (customer pre-payments) as data centers rush to secure production slots.

Segmental Economics & Unit Profitability

Table FY2025 Segment Revenue Breakdown, Margin Profile, and Growth Drivers of Distributed Energy & Engine Solutions Business

| Core Business Segment | FY2025 Revenue (USD) | % of Total Revenue | Gross Margin | Growth Drivers & Proprietary Technology |

|---|---|---|---|---|

| Total Equipment | $1,365.4M | 51.8% | 27.2% | Jenbacher and Waukesha engines; equipment order intake surged 187.8% YoY |

| — Data Center | $261.8M | 10.0% | N/A | Revenue skyrocketed 357.7% YoY, driving 35.9% regional revenue growth in North America |

| — Power Solutions | $892.6M | 33.8% | N/A | Grid balancing, microgrids, and Combined Heat and Power (CHP) deployments |

| — Compression | $211.0M | 8.0% | N/A | Midstream/upstream gas transport and harsh-environment processing |

| Total Services | $1,271.4M | 48.2% | 42.5% | Proprietary parts account for ~85% of Services revenue, providing insulation against labor inflation |

| — Transactional | $808.6M | 30.7% | N/A | On-demand parts and overhauls supporting an installed base of approximately 44 GW globally |

| — Contractual | $462.8M | 17.5% | N/A | 10-year Long-Term Service Agreements (LTSAs) reinforced by the myplant AI fleet management ecosystem |

* Capital Structure & Debt Leverage

* As of December 2025, Total Debt spiked to $2,658.8 million, pushing the Net Debt to Adjusted EBITDA ratio to an elevated 3.59x. Interest coverage remains secure at 3.36x.

* Core debt instruments include a €1,100.0 million Term Loan B, a $589.5 million Term Loan B-USD, and a newly syndicated $750.0 million Term Loan B2-USD specifically raised to fund the sponsor dividend recapitalization.

Supply Chain Audit & Geo-Economic Moat

INNIO executes a strict "local-for-local" manufacturing strategy across an approximately 7 million sq. ft. physical footprint to circumvent geopolitical friction (e.g., up to 200% US steel/aluminum tariffs and potential export controls on rare earth minerals from Taiwan, China, and mainland China).

* European Hubs (Centers of Excellence):

* Jenbach, Austria: The 2.1 million sq. ft. campus (1 million sq. ft. building) serves as the primary R&D, assembly, and testing epicenter for Jenbacher engines.

* Hall and Kapfenberg, Austria: Dedicated satellite facilities handling specialized components (69,000 sq. ft.) and spark plug manufacturing (45,000 sq. ft.).

* North American AI Compute Supply Chain:

* Welland, Ontario: Features 3.4 million sq. ft. of land housing massive spare capacity and assembly operations.

* Waukesha, Wisconsin: The 1.7 million sq. ft. site operates as the US corporate headquarters and primary engine remanufacturing hub.

* Strategic Chokepoints (Containerization): Newly launched, dedicated packaging centers in Trenton, New Jersey (93,000 sq. ft.) and Waller, Texas (65,000 sq. ft.) are optimized specifically for the rapid deployment of containerized data center solutions, drastically reducing "time-to-power."

* Physical Supply Chain Vulnerabilities: The firm relies on single-source suppliers for highly engineered components like cylinder head castings and heat exchangers. Furthermore, the myplant digital moat faces severe regulatory exposure under the EU AI Act (potential fines up to $39.57 million) and GDPR.

HDIN Institutional Perspective: An exceptionally high-quality asset executing a highly leveraged private equity exit disguised as a pure-play energy transition and AI infrastructure IPO

The Street is currently pricing INNIO as a "hydrogen-ready" derivative play on AI data center microgrids. We validate this operational moat: a 2.8x book-to-bill ratio and a $4.78 billion Q1 2026 backlog confirm that its modular 5 MW to 25 MW engines are successfully bypassing utility grid queues, directly curing the "power anxiety" of Tier-1 hyperscalers.

However, utilizing a differentiated viewpoint focused on forensic capital allocation, public market buyers are primarily funding the liquidity exit of private equity sponsors (Advent/ADIA). The $723.8 million capital repayment extracted in 2025 via the new $750 million Term Loan B2 thoroughly hollowed out historical retained earnings. The "Use of Proceeds" section in the S-1 functions as a blank check, lacking explicit commitments to deleverage the current 3.59x net debt ratio.

Furthermore, current risk models have not fully priced in extreme customer concentration: a single Energy-as-a-Service partner, VoltaGrid, accounted for an outsized 41% of total 2025 equipment orders. While the myplant ecosystem effectively locks customers into a 42.5% margin aftermarket, macroeconomic spark spread volatility and regulatory headwinds (e.g., New York's 2029 natural gas ban) suggest this is a high-reward, yet structurally vulnerable, industrial bet. Executive alignment remains bottlenecked by strict pro-rata sell-down rules, requiring institutional LPs to closely monitor the actual execution of the 2026 Incentive Award Plan post-IPO.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."