Exyn Technologies: SaaS Pivot Near Philadelphia Headquarters as Severe Liquidity Constraints Signal Urgent Need for Recapitalization

Date : 2026-05-14

Reading : 461

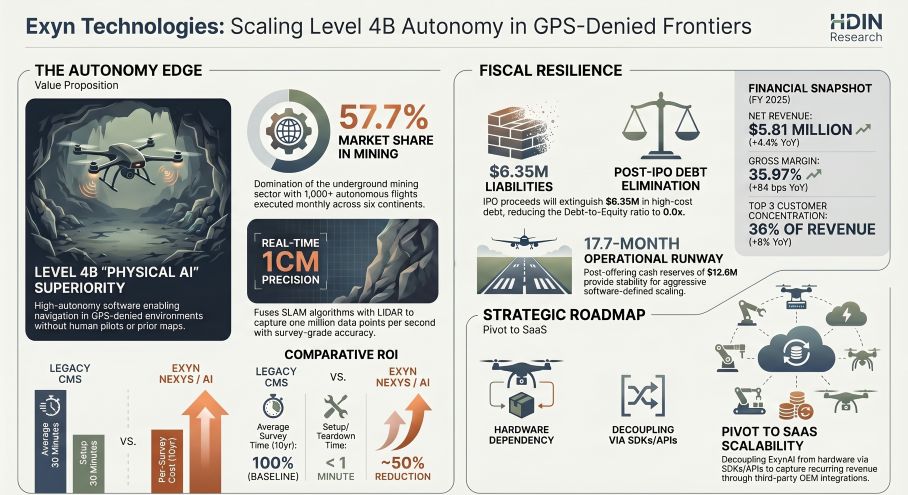

Exyn Technologies faces a critical insolvency threat, entering 2026 with a depleted $0.81 million cash reserve against $6.12 million in accelerated short-term debt. While the proposed IPO promises a 17.7-month runway extension, institutional LPs must weigh the company’s transition toward higher-margin software licensing against acute geopolitical vulnerabilities. Over 20% of its core physical supply chain relies on Chinese entities facing imminent U.S. regulatory bans. This forces a binary outcome: successfully execute a hardware-agnostic SaaS pivot or face debilitating supply chain paralysis.

Figure Exyn Technologies: Scaling Level 4B Autonomy in GPS-Denied Frontiers

Segmental Inventory & Operating Leverage

Segmental Inventory & Operating Leverage

An audit of the consolidated statements reveals a distressed capital structure highly dependent on the public markets for immediate debt extinguishment. While Exyn aggressively markets its Level 4B ExynAI software, the reality of its revenue mix remains overwhelmingly tethered to physical hardware sales.

* Segmental Breakdown (FY2025): Hardware and bundled software (Systems) drove 87.5% of total revenue ($5.08 million). Services accounted for 6.5%, and Subscription Leases contributed a marginal 6.0%.

* Operating Leverage: The company exhibits high cash consumption with an implied operating burn rate of $706,446 per month.

* Capitalization Dynamics: Post-IPO, new investors face an immediate net tangible book value dilution of $6.76 per share. The issuance of 2.5 million EXYNW warrants (exercisable at a 125% premium) creates a massive structural overhang, capping potential equity upside for NASDAQ: EXYN shareholders.

Table FY2024 vs. FY2025 Financial Performance and Liquidity Overview

Supply Chain Audit & Geo-Economic Moat

Exyn operates from its primary R&D center at 2118 Washington Avenue, Suite 1000, in Philadelphia, Pennsylvania. Despite its domestic IP generation stemming from the UPenn GRASP Laboratory, the company’s physical supply chain lacks a defensible geo-economic moat, introducing fatal-tail risks ahead of 2026 federal deadlines.

* Tier-1 Supplier Concentration: Exyn relies on an asset-light, outsourced model. Roughly 29% of fabrication is tied to SuNPe Limited, 15% of critical LiDAR scanning technology is sourced from Hesai Technology Co., Ltd., and 5% of drone structural components come from DJI.

* Regulatory & Geopolitical Hurdles: The reliance on Hesai and DJI exposes Exyn to acute legislative friction. The Countering CCP Drones Act (mandating security reviews by December 2025) and the American Security Drone Act (restricting federal procurement by January 2026) threaten to paralyze Exyn’s hardware delivery pipeline, forcing expensive, margin-compressing redesigns.

* Geographic Revenue & Compliance Risks: While 33.1% of revenue originates in the U.S., Canada generates 18.3%. A critical internal control failure resulted in unremitted Canadian indirect taxes (GST, HST, PST), creating an unquantified off-balance-sheet liability that will further drain the limited post-IPO liquidity.

HDIN Institutional Perspective

The Street is likely to misprice Exyn Technologies by valuing it as an AI-native SaaS platform. Our Forensic Analysis confirms it is currently a low-growth hardware distributor executing a distressed recapitalization.

While management’s strategy to modularize ExynAI via SDKs and APIs into third-party OEM ecosystems is the correct strategic pivot, the execution timeline is misaligned with the company’s capital constraints. The immediate use of IPO proceeds is defensively allocated to extinguish $6.35 million in toxic, accelerated debt (including Western Alliance Bank and Maximcash loans). Furthermore, the extreme customer concentration—three clients account for 36% of total 2025 revenue—coupled with a 9-to-11 month enterprise sales cycle, indicates that the projected 17.7-month post-IPO cash runway leaves zero margin for execution error. The 44.1% concentrated voting bloc held by early insiders (Reliance, North America University Innovation) further strips public market participants of governance leverage.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Exyn Technologies: Scaling Level 4B Autonomy in GPS-Denied Frontiers

Segmental Inventory & Operating LeverageAn audit of the consolidated statements reveals a distressed capital structure highly dependent on the public markets for immediate debt extinguishment. While Exyn aggressively markets its Level 4B ExynAI software, the reality of its revenue mix remains overwhelmingly tethered to physical hardware sales.

* Segmental Breakdown (FY2025): Hardware and bundled software (Systems) drove 87.5% of total revenue ($5.08 million). Services accounted for 6.5%, and Subscription Leases contributed a marginal 6.0%.

* Operating Leverage: The company exhibits high cash consumption with an implied operating burn rate of $706,446 per month.

* Capitalization Dynamics: Post-IPO, new investors face an immediate net tangible book value dilution of $6.76 per share. The issuance of 2.5 million EXYNW warrants (exercisable at a 125% premium) creates a massive structural overhang, capping potential equity upside for NASDAQ: EXYN shareholders.

Table FY2024 vs. FY2025 Financial Performance and Liquidity Overview

FY2025 Financial Performance and Liquidity Overview

| Financial Metric | FY 2024 | FY 2025 | YoY Variance | Institutional Notes |

|---|---|---|---|---|

| Net Revenue | $5,568,280 | $5,810,504 | +4.4% | Stagnant top-line growth; heavy reliance on the Nexys product line |

| Gross Profit | $1,956,430 | $2,090,281 | +6.8% | Gross margin expanded by 84 bps to 35.97% |

| R&D Expenses | $6,487,224 | $4,730,789 | -27.1% | Decline driven by the roll-off of legacy ExynAero and ExynPak program costs |

| Net Loss | $(12,810,117) | $(12,191,687) | -4.8% | Continued unprofitability; accumulated deficit reached $75.9M |

| Cash Reserves | $1,981,564 | $812,534 | -59.0% | Decline triggered auditor “Going Concern” warning |

Exyn operates from its primary R&D center at 2118 Washington Avenue, Suite 1000, in Philadelphia, Pennsylvania. Despite its domestic IP generation stemming from the UPenn GRASP Laboratory, the company’s physical supply chain lacks a defensible geo-economic moat, introducing fatal-tail risks ahead of 2026 federal deadlines.

* Tier-1 Supplier Concentration: Exyn relies on an asset-light, outsourced model. Roughly 29% of fabrication is tied to SuNPe Limited, 15% of critical LiDAR scanning technology is sourced from Hesai Technology Co., Ltd., and 5% of drone structural components come from DJI.

* Regulatory & Geopolitical Hurdles: The reliance on Hesai and DJI exposes Exyn to acute legislative friction. The Countering CCP Drones Act (mandating security reviews by December 2025) and the American Security Drone Act (restricting federal procurement by January 2026) threaten to paralyze Exyn’s hardware delivery pipeline, forcing expensive, margin-compressing redesigns.

* Geographic Revenue & Compliance Risks: While 33.1% of revenue originates in the U.S., Canada generates 18.3%. A critical internal control failure resulted in unremitted Canadian indirect taxes (GST, HST, PST), creating an unquantified off-balance-sheet liability that will further drain the limited post-IPO liquidity.

HDIN Institutional Perspective

The Street is likely to misprice Exyn Technologies by valuing it as an AI-native SaaS platform. Our Forensic Analysis confirms it is currently a low-growth hardware distributor executing a distressed recapitalization.

While management’s strategy to modularize ExynAI via SDKs and APIs into third-party OEM ecosystems is the correct strategic pivot, the execution timeline is misaligned with the company’s capital constraints. The immediate use of IPO proceeds is defensively allocated to extinguish $6.35 million in toxic, accelerated debt (including Western Alliance Bank and Maximcash loans). Furthermore, the extreme customer concentration—three clients account for 36% of total 2025 revenue—coupled with a 9-to-11 month enterprise sales cycle, indicates that the projected 17.7-month post-IPO cash runway leaves zero margin for execution error. The 44.1% concentrated voting bloc held by early insiders (Reliance, North America University Innovation) further strips public market participants of governance leverage.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."