VisionSys AI: Radical BCI Pivot Near Langfang HQ as $2.92M Intangible Impairment Signals Execution Fragility

Date : 2026-05-14

Reading : 103

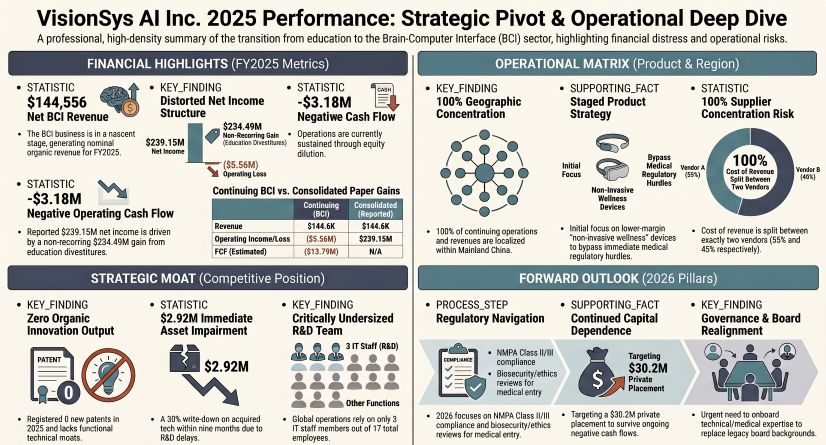

VisionSys AI has finalized its divestiture from legacy education, pivoting entirely toward Brain-Computer Interface (BCI) technology. However, an immediate $2.92 million Q4 impairment on its newly acquired $10.61 million source code underscores severe execution friction. Operating from a leased facility in Langfang, Hebei, with zero registered patents, the firm’s $234.49 million paper gain masks a deeply unprofitable core. For institutional LPs, 100% supplier concentration and sub-scale 22.0% gross margins suggest a highly speculative, cash-burning hardware-integration model severely exposed to Sino-U.S. semiconductor export controls.

Figure VisionSys Al Inc 2025 Performance: Strategic Pivot & Operational Deep Dive

Forensic Analysis of Financials & Segmental Inventory

Forensic Analysis of Financials & Segmental Inventory

The fiscal 2025 consolidated data presents a severe distortion between accounting artifacts and core operational viability. While the headline net income sits at $239.15 million, this is fundamentally an illusion driven by a $234.49 million non-cash gain from the derecognition of legacy STEM education liabilities. The continuing BCI operations exhibit the following baseline:

* Core Unit Economics: FY2025 revenue registered at a nominal $144,556 against a cost of revenues of $112,696, yielding an unscaled gross profit of $31,861 (Gross Margin: 22.0%).

* Operating Leverage Vacuum: The company operates with $0 in deferred revenue and $0 in dedicated sales and marketing expenditure. Without a subscription framework, customer acquisition costs (CAC) and net retention rates (NRR) remain unquantifiable.

* Liquidity & Burn Rate: Operating cash flow for continuing operations is deeply negative at -$3.18 million. Current liquidity is entirely sustained by equity dilution, highlighted by $25.85 million in 2025 financing cash flows and an ongoing $30.2 million proposed private placement.

* Aggressive Accounting & Impairment: VisionSys AI utilized a 100% R&D capitalization ratio in 2025, recording $0 in expensed R&D. Instead, it capitalized a $10.61 million BCI software purchase from Jeethen International. Using the Multi-Period Excess Earnings Method (MPEEM), management was forced to write down this exact asset by $2.92 million in Q4 2025 due to commercialization delays, confirming a structurally flawed initial valuation.

* Tax Posture: A 100% deferred tax valuation allowance of $366,500 signals that management anticipates zero near-term taxable income from the BCI segment.

The Langfang Fabless Architecture

VisionSys AI operates a strictly asset-light, fabless architecture from its leased headquarters in Yanjiao, Sanhe City, Langfang, Hebei Province. The balance sheet reflects $0 in Construction in Progress (CIP) and $0 in Property, Plant, and Equipment (PP&E).

* Extreme Supplier Concentration: The company’s entire hardware ecosystem—comprising signal acquisition modules, microchips, and electrodes—relies on a dangerously narrow supply corridor. In 2025, 100% of the cost of revenues was locked into two entities: Vendor A (55%) and Vendor B (45%). VisionSys AI possesses zero negotiating leverage or upstream pricing power.

* Geopolitical Vulnerability: Because BCI hardware is highly reliant on advanced microelectronics, the company's supply chain is highly exposed to tightening U.S. export controls on artificial intelligence and semiconductor technologies. Any enforcement shock could immediately halt the firm's ODM/OEM procurement capabilities.

* Regulatory Staging: Facing rigorous National Medical Products Administration (NMPA) Class III medical device regulations for invasive BCI, the company has retreated to a "staged commercialization" strategy. Current deployment is restricted to lower-margin, non-invasive general wellness products (e.g., electronic meditation and sleep support devices) to circumvent clinical trial bottlenecks. Data compliance costs remain elevated due to China's strict data localization and cross-border transfer laws regarding sensitive neural data.

HDIN Institutional Perspective: Capital Allocation & Governance Disconnect

While retail optics may focus on the headline profitability and the AI narrative, the underlying capital allocation mechanisms reveal a company attempting to beautify an unproven pivot. The strategy to capitalize 100% of technology acquisition costs shielded the P&L from conventional R&D burdens, artificially minimizing the $5.56 million operating loss. However, the immediate Q4 impairment proves that the acquired algorithms lack the commercial viability to justify their carrying value.

Furthermore, a critical governance mismatch exacerbates execution risk. The reconstituted Board of Directors is populated entirely by executives with backgrounds in apparel retail, real estate HR, basic education, and foreign trade. There is an absolute void of biotechnology, AI, or medical regulatory domain expertise. Coupled with an equity incentive structure that grants 120,000 options at a $0.01 exercise price over a 10-year time-based vesting schedule—completely omitting technical or regulatory KPIs—the compensation framework functions as a low-bar retention scheme rather than the milestone-driven architecture required to navigate a high-risk deep-tech commercialization cycle. With 0 registered patents and an R&D department of just 3 IT staff, VisionSys AI lacks the requisite IP moats to defend its market position.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant)*:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure VisionSys Al Inc 2025 Performance: Strategic Pivot & Operational Deep Dive

Forensic Analysis of Financials & Segmental InventoryThe fiscal 2025 consolidated data presents a severe distortion between accounting artifacts and core operational viability. While the headline net income sits at $239.15 million, this is fundamentally an illusion driven by a $234.49 million non-cash gain from the derecognition of legacy STEM education liabilities. The continuing BCI operations exhibit the following baseline:

* Core Unit Economics: FY2025 revenue registered at a nominal $144,556 against a cost of revenues of $112,696, yielding an unscaled gross profit of $31,861 (Gross Margin: 22.0%).

* Operating Leverage Vacuum: The company operates with $0 in deferred revenue and $0 in dedicated sales and marketing expenditure. Without a subscription framework, customer acquisition costs (CAC) and net retention rates (NRR) remain unquantifiable.

* Liquidity & Burn Rate: Operating cash flow for continuing operations is deeply negative at -$3.18 million. Current liquidity is entirely sustained by equity dilution, highlighted by $25.85 million in 2025 financing cash flows and an ongoing $30.2 million proposed private placement.

* Aggressive Accounting & Impairment: VisionSys AI utilized a 100% R&D capitalization ratio in 2025, recording $0 in expensed R&D. Instead, it capitalized a $10.61 million BCI software purchase from Jeethen International. Using the Multi-Period Excess Earnings Method (MPEEM), management was forced to write down this exact asset by $2.92 million in Q4 2025 due to commercialization delays, confirming a structurally flawed initial valuation.

* Tax Posture: A 100% deferred tax valuation allowance of $366,500 signals that management anticipates zero near-term taxable income from the BCI segment.

The Langfang Fabless Architecture

VisionSys AI operates a strictly asset-light, fabless architecture from its leased headquarters in Yanjiao, Sanhe City, Langfang, Hebei Province. The balance sheet reflects $0 in Construction in Progress (CIP) and $0 in Property, Plant, and Equipment (PP&E).

* Extreme Supplier Concentration: The company’s entire hardware ecosystem—comprising signal acquisition modules, microchips, and electrodes—relies on a dangerously narrow supply corridor. In 2025, 100% of the cost of revenues was locked into two entities: Vendor A (55%) and Vendor B (45%). VisionSys AI possesses zero negotiating leverage or upstream pricing power.

* Geopolitical Vulnerability: Because BCI hardware is highly reliant on advanced microelectronics, the company's supply chain is highly exposed to tightening U.S. export controls on artificial intelligence and semiconductor technologies. Any enforcement shock could immediately halt the firm's ODM/OEM procurement capabilities.

* Regulatory Staging: Facing rigorous National Medical Products Administration (NMPA) Class III medical device regulations for invasive BCI, the company has retreated to a "staged commercialization" strategy. Current deployment is restricted to lower-margin, non-invasive general wellness products (e.g., electronic meditation and sleep support devices) to circumvent clinical trial bottlenecks. Data compliance costs remain elevated due to China's strict data localization and cross-border transfer laws regarding sensitive neural data.

HDIN Institutional Perspective: Capital Allocation & Governance Disconnect

While retail optics may focus on the headline profitability and the AI narrative, the underlying capital allocation mechanisms reveal a company attempting to beautify an unproven pivot. The strategy to capitalize 100% of technology acquisition costs shielded the P&L from conventional R&D burdens, artificially minimizing the $5.56 million operating loss. However, the immediate Q4 impairment proves that the acquired algorithms lack the commercial viability to justify their carrying value.

Furthermore, a critical governance mismatch exacerbates execution risk. The reconstituted Board of Directors is populated entirely by executives with backgrounds in apparel retail, real estate HR, basic education, and foreign trade. There is an absolute void of biotechnology, AI, or medical regulatory domain expertise. Coupled with an equity incentive structure that grants 120,000 options at a $0.01 exercise price over a 10-year time-based vesting schedule—completely omitting technical or regulatory KPIs—the compensation framework functions as a low-bar retention scheme rather than the milestone-driven architecture required to navigate a high-risk deep-tech commercialization cycle. With 0 registered patents and an R&D department of just 3 IT staff, VisionSys AI lacks the requisite IP moats to defend its market position.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant)*:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."