Huajian Future: Supply Chain De-Risking Near Chengdu Wenjiang Hub as Peak 2026 R&D Burn Signals Pivot Toward Late-Stage Commercialization

Date : 2026-05-15

Reading : 393

Huajian Future’s pre-IPO filings reveal a structurally entrenched leadership under Dr. Ji Jianxin, whose 57.50% voting control and CEO/Chairman duality ensure strategic velocity but introduce distinct governance friction for institutional LPs like SDIC Shanghai (9.20%) and Legend Capital (7.08%). As the firm absorbs a $12.44 million operating cash burn to fund its TSD-IAS driven pipeline, its highly localized Chengdu supply chain insulates it from macro biosecurity and geopolitical scrutiny. However, the aggressive timeline for 2026 FDA IND submissions against a backdrop of zero proprietary manufacturing capacity permanently transitions the corporate risk profile from early-stage discovery to late-stage commercial execution.

Figure Huajian Future (Chengdu) lPO Analysis: A New Era for Small Molecule Innovation

Internal Capital Allocation & Clinical Unit Economics

A forensic audit of Huajian Future’s capital allocation reveals a pre-revenue clinical entity aggressively utilizing treasury strategies to offset a structurally expanding R&D burn. In 2025, operating cash burn reached $12.44 million (CNY 89.43 million), mitigated marginally by a $0.91 million (CNY 6.545 million) net fair value gain extracted from converting matured term deposits into highly liquid wealth management products.

The corporate governance framework points to standard historical related-party transactions (RPTs), with a minimal $45,635 (CNY 328,000) payable to Dr. Ji for corporate vehicles, which was fully settled in August 2025. To secure talent through the volatile 2026–2028 NDA windows, the company deployed a Pre-IPO Share Incentive Plan capping at 2,093,400 shares (3.49% of pre-IPO capital) via platforms including Suzhou Jishitang, utilizing a staggered 30%-30%-40% three-year vesting cliff.

R&D Unit Economics & Personnel Density

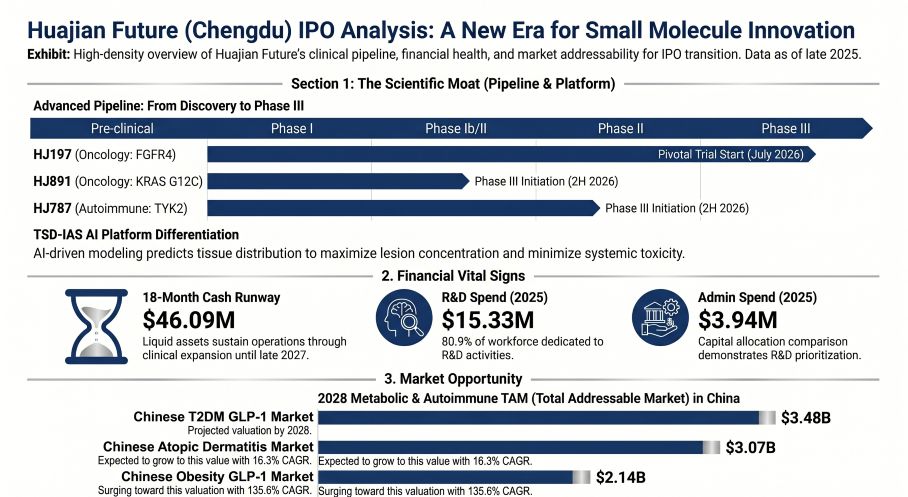

* Total R&D Workforce: 93 personnel (80.9% of total 115-headcount staff).

* Academic Distribution: Heavy reliance on mid-level degrees, with 25.0% holding Master’s degrees (23 staff) and only 4.3% holding PhDs (4 staff).

* Cost per Unit: Total 2025 R&D staff costs amounted to $5.35 million (CNY 38.45 million), translating to an average R&D compensation of ~$57,526 (CNY 413,483) per capita, a metric likely inflated by the structural booking of the pre-IPO ESOP distribution rather than pure base salaries.

Table Pipeline Efficacy & Patent Expiration Matrix

Note: The global IP moat comprises 58 patents (29 granted, 29 pending) with full Freedom to Operate (FTO) clearance across all primary assets.*

The Chengdu-Chongqing Axis

Huajian Future operates with zero proprietary commercial manufacturing capacity, exposing the firm to critical vendor dynamics as clinical trials scale. The geo-economic footprint is heavily concentrated in the Wenjiang District of Chengdu, Sichuan. The company holds 17 undisputed property ownership certificates covering 57,699.4 square meters of land and 3,047.4 square meters of gross floor area, supplemented by a 903.0-square-meter leased R&D space. A longer-term strategic hedge exists via a 2023 lease/purchase right agreement at the Jiangjin Industrial Park in Chongqing, though activation remains dormant for the next 12 months.

Vendor Consolidation & API Dependency

The supplier network exhibits a material shift toward singular CDMO dependency. While aggregate Top 5 supplier concentration fell slightly from 38.8% in 2024 to 37.0% ($4.83 million) in 2025, procurement from Supplier B (CDMO for API and clinical supply) surged 293% YoY. Supplier B expanded from $0.57 million (7.2% of total spend) in 2024 to $2.24 million (17.2%) in 2025. Conversely, clinical and SMO services heavily fragmented, relying on a dispersed pool of 51 CROs in 2025 (up from 41 in 2024), with new vendors like Supplier I (Raw Materials, 7.2%, $0.94 million) and Supplier A (Pre-clinical CRO, 3.8%, $0.50 million) entering the top 5.

ESG Liability & Clinical Waste Escalation

Adherence to China's Data Security Law and Biosecurity Law mandates strict multi-tiered governance. Clinical trial data is restricted via Electronic Data Capture (EDC) systems with mandatory deletion five years post-market approval. Environmentally, rapid clinical scaling has strained waste management; hazardous solid waste generation more than doubled YoY from 29.5 tons (0.4 tons per million RMB of R&D) to 63.1 tons (0.6 tons per million RMB). Management’s pledge to reduce emissions by 5% over three years will require strict vendor tracking, especially considering a historical, albeit fully rectified, occupational safety violation that carried a ~$70,000 (CNY 500,000) fine exposure.

HDIN Institutional Perspective: Challenging the "AI-Driven" Valuation Premium

While the prospectus aggressively champions its proprietary TSD-IAS (Tissue-Specific Distribution Intelligent Analysis System) and a pristine 58-patent IP moat as evidence of a highly differentiated, tech-forward biotech platform, the internal structural metrics suggest a reality that requires careful pricing by institutional capital.

The most glaring discrepancy lies within the R&D workforce architecture. For an oncology and metabolic discovery engine relying on complex machine learning (TSD-IAS) to predict organ distribution, a PhD density of merely 4.3% (4 out of 93 R&D staff) is anomalous. This suggests that the foundational IP is either heavily reliant on the legacy outputs of the Chinese Academy of Sciences (CAS)—from which Dr. Ji Jianxin, Dr. Guo Na, and Dr. Du Fengtian hail—or that high-end computational chemistry is being functionally outsourced. Furthermore, the abrupt 293% surge in capital allocation toward a singular API manufacturer (Supplier B) indicates that Huajian Future is already transitioning into a traditional, capital-intensive late-stage hardware/manufacturing burn phase. The Street must discount the "AI-discovery" multiple and instead price Huajian Future as a late-stage clinical executor entirely dependent on securing external CDMO capacity ahead of its critical 2H 2026 Phase III readouts.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Huajian Future (Chengdu) lPO Analysis: A New Era for Small Molecule Innovation

Internal Capital Allocation & Clinical Unit Economics

A forensic audit of Huajian Future’s capital allocation reveals a pre-revenue clinical entity aggressively utilizing treasury strategies to offset a structurally expanding R&D burn. In 2025, operating cash burn reached $12.44 million (CNY 89.43 million), mitigated marginally by a $0.91 million (CNY 6.545 million) net fair value gain extracted from converting matured term deposits into highly liquid wealth management products.

The corporate governance framework points to standard historical related-party transactions (RPTs), with a minimal $45,635 (CNY 328,000) payable to Dr. Ji for corporate vehicles, which was fully settled in August 2025. To secure talent through the volatile 2026–2028 NDA windows, the company deployed a Pre-IPO Share Incentive Plan capping at 2,093,400 shares (3.49% of pre-IPO capital) via platforms including Suzhou Jishitang, utilizing a staggered 30%-30%-40% three-year vesting cliff.

R&D Unit Economics & Personnel Density

* Total R&D Workforce: 93 personnel (80.9% of total 115-headcount staff).

* Academic Distribution: Heavy reliance on mid-level degrees, with 25.0% holding Master’s degrees (23 staff) and only 4.3% holding PhDs (4 staff).

* Cost per Unit: Total 2025 R&D staff costs amounted to $5.35 million (CNY 38.45 million), translating to an average R&D compensation of ~$57,526 (CNY 413,483) per capita, a metric likely inflated by the structural booking of the pre-IPO ESOP distribution rather than pure base salaries.

Table Pipeline Efficacy & Patent Expiration Matrix

| Asset & Target Indication | Clinical Efficacy Markers | Target NMPA / FDA Milestones | IP Expiration Window |

|---|---|---|---|

| HJ787 (TYK2 Inhibitor) | Phase II achieved EASI-75 response rate of 62.5% at Week 8 (3% BID dosage) | Phase III initiation (2H 2026); NMPA NDA submission (1H 2028); FDA IND filing (March 2027) | May 2042 (Granted in Russia, Australia, and Japan) |

| HJ178 (GLP-1/GIPR Dual Agonist) | Post-prandial glucose reduction of -5.88 mmol/L at 2 hours; -1.55 kg weight loss over 28 days | Phase III initiation (1H 2027); NMPA NDA submission (2H 2028); FDA IND filing (Oct/Dec 2026) | November 2040 (Granted in China, the US, the EU, and Japan) |

| HJ891 (KRAS G12C Inhibitor) | ORR of 77.8% and DCR of 96.3% in combination with Toripalimab; TPS ≥50% subgroup achieved 92.3% ORR | Phase III program expected from 2H 2026 to 2H 2029; FDA IND filing (2H 2026) | February 2041 (Granted in China and Japan) |

| HJ197 (FGFR4 Inhibitor) | NMPA pivotal Phase III trial initiated in August 2023 | Currently advancing through pivotal Phase III development | December 2037 (Granted in China, the US, the EU, and Japan) |

The Chengdu-Chongqing Axis

Huajian Future operates with zero proprietary commercial manufacturing capacity, exposing the firm to critical vendor dynamics as clinical trials scale. The geo-economic footprint is heavily concentrated in the Wenjiang District of Chengdu, Sichuan. The company holds 17 undisputed property ownership certificates covering 57,699.4 square meters of land and 3,047.4 square meters of gross floor area, supplemented by a 903.0-square-meter leased R&D space. A longer-term strategic hedge exists via a 2023 lease/purchase right agreement at the Jiangjin Industrial Park in Chongqing, though activation remains dormant for the next 12 months.

Vendor Consolidation & API Dependency

The supplier network exhibits a material shift toward singular CDMO dependency. While aggregate Top 5 supplier concentration fell slightly from 38.8% in 2024 to 37.0% ($4.83 million) in 2025, procurement from Supplier B (CDMO for API and clinical supply) surged 293% YoY. Supplier B expanded from $0.57 million (7.2% of total spend) in 2024 to $2.24 million (17.2%) in 2025. Conversely, clinical and SMO services heavily fragmented, relying on a dispersed pool of 51 CROs in 2025 (up from 41 in 2024), with new vendors like Supplier I (Raw Materials, 7.2%, $0.94 million) and Supplier A (Pre-clinical CRO, 3.8%, $0.50 million) entering the top 5.

ESG Liability & Clinical Waste Escalation

Adherence to China's Data Security Law and Biosecurity Law mandates strict multi-tiered governance. Clinical trial data is restricted via Electronic Data Capture (EDC) systems with mandatory deletion five years post-market approval. Environmentally, rapid clinical scaling has strained waste management; hazardous solid waste generation more than doubled YoY from 29.5 tons (0.4 tons per million RMB of R&D) to 63.1 tons (0.6 tons per million RMB). Management’s pledge to reduce emissions by 5% over three years will require strict vendor tracking, especially considering a historical, albeit fully rectified, occupational safety violation that carried a ~$70,000 (CNY 500,000) fine exposure.

HDIN Institutional Perspective: Challenging the "AI-Driven" Valuation Premium

While the prospectus aggressively champions its proprietary TSD-IAS (Tissue-Specific Distribution Intelligent Analysis System) and a pristine 58-patent IP moat as evidence of a highly differentiated, tech-forward biotech platform, the internal structural metrics suggest a reality that requires careful pricing by institutional capital.

The most glaring discrepancy lies within the R&D workforce architecture. For an oncology and metabolic discovery engine relying on complex machine learning (TSD-IAS) to predict organ distribution, a PhD density of merely 4.3% (4 out of 93 R&D staff) is anomalous. This suggests that the foundational IP is either heavily reliant on the legacy outputs of the Chinese Academy of Sciences (CAS)—from which Dr. Ji Jianxin, Dr. Guo Na, and Dr. Du Fengtian hail—or that high-end computational chemistry is being functionally outsourced. Furthermore, the abrupt 293% surge in capital allocation toward a singular API manufacturer (Supplier B) indicates that Huajian Future is already transitioning into a traditional, capital-intensive late-stage hardware/manufacturing burn phase. The Street must discount the "AI-discovery" multiple and instead price Huajian Future as a late-stage clinical executor entirely dependent on securing external CDMO capacity ahead of its critical 2H 2026 Phase III readouts.

Presentation Download & Video Access

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."