GMR Solutions: Capital Restructuring Near Lewisville Hub as 160% Cash Flow Surge Signals Aggressive 2026 Margin Expansion

Date : 2026-05-15

Reading : 276

GMR Solutions is executing a radical capital optimization strategy, funneling 100% of its $415.2 million IPO proceeds toward debt and high-yield preferred stock redemption. While a deliberate mix-shift drove a 10.9% organic core transport revenue expansion in 2025, structural overhangs persist. The company’s Texas-led clinical triage innovations yield unprecedented operating leverage, yet KKR's 60.9% equity pledge for margin loans introduces severe systemic volatility. For institutional LPs, the thesis hinges on whether self-funded 2026 rural footprint expansion can outpace the friction of legacy leverage and strict single-source aviation supply chain vulnerabilities.

Segmental Incremental Margins & Capital Allocation

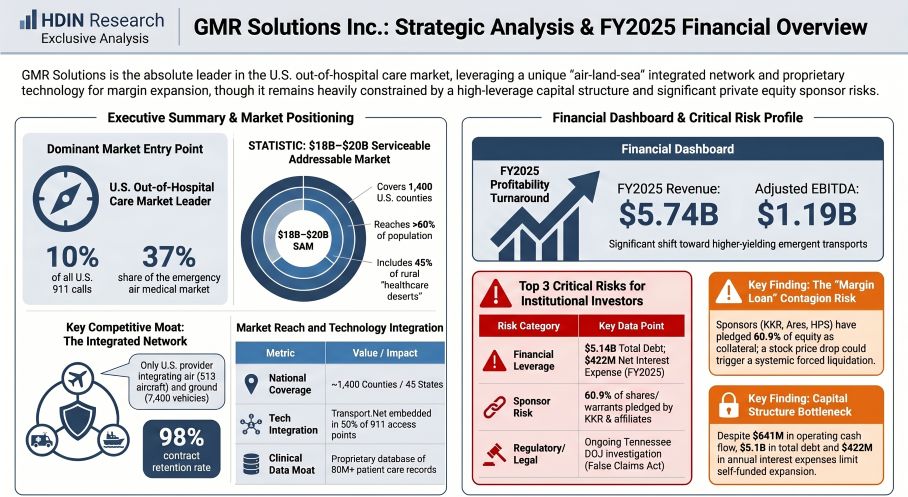

A forensic audit of the 2025 Form S-1 reveals a highly cash-generative operational core masked by a divestiture-driven top-line contraction. Total 2025 revenue contracted 4.0% to $5,739.8 million due to the strategic divestiture of non-core units, yet the underlying organic transport yield expanded aggressively.

Figure GMR Solutions Inc: Strategic Analysis & FY2025 Financial Overview

Financial Inventory & Operational KPIs (FY 2023 – FY 2025)

Financial Inventory & Operational KPIs (FY 2023 – FY 2025)

* Net Transport Revenue: Reached $5,559.6 million in 2025 (96.8% of total revenue), driven by an 11.8% surge in net transport revenue per ambulance to $1,332.

* Operating Leverage: Operating income expanded to $751.6 million, pushing margins to 13.1% in 2025 (up from 6.5% in 2023). Adjusted EBITDA grew at a 25.8% CAGR from 2023 to reach $1,186.2 million.

* Free Cash Flow Conversion: Operating Cash Flow (OCF) surged 160% year-over-year to $641.1 million, comfortably covering the highly disciplined $258.5 million in localized CAPEX.

* Internal Capital Allocation: 0% of the projected $415.2 million IPO proceeds are earmarked for direct R&D or expansion. Instead, $299.4 million is allocated to redeem the 15%-yielding Series B Preferred Stock, while the remaining ~$115.8 million, combined with $500 million from a concurrent Private Placement, will retire $665.8 million of the 2032 First Lien Term Loan (SOFR + 3.50%).

* Interest Rate Sensitivity: The capital stack remains precarious; total debt sits at $5,142.7 million, with a 100-bps increase in interest rates equating to an estimated $46.6 million annual reduction in net earnings.

Unit economics are heavily supported by proprietary technology. The Nurse Navigation platform effectively diverts up to 20% of low-acuity 911 calls to alternate care settings, stripping out profit-draining "dry runs" and generating a 15% decrease in non-transport encounters. This acts as a primary catalyst for margin expansion and improves the commercial payor mix.

Physicality Audit: Supply Chain Vulnerabilities & Geo-Economic Moat

The physical infrastructure of GMR Solutions spans 45 states, covering 62% of the U.S. population with an omnichannel fleet of roughly 7,400 ground vehicles, 400 rotor-wing, and 113 fixed-wing aircraft.

* Backward Integration: Ground fleet resilience is anchored by the Mineral Wells Remount Facility in Texas. This hub enables in-house ambulance overhauls, compressing vehicle capital expenditures by up to 40% compared to new procurement.

* Aviation Sole-Source Bottleneck: Conversely, the aviation supply chain exhibits severe fragility. The company relies on a concentrated oligopoly for helicopters and dynamic engine components, explicitly noting a lack of alternative supply sources. This single-point-of-failure exposes the fleet to FAA airworthiness grounding directives and inflationary part pricing.

* Fuel & Weather Constraints: Macroeconomic variables dictate operational tempo. A 10% swing in commodity fuel prices directly impacts net cash flow by $7 million. Furthermore, 17.2% of emergent air transport requests in 2025 were canceled strictly due to weather, a direct top-line headwind.

* Geographic Expansion: Operations are scheduled to scale with the addition of 15 new rural air bases in 2026, targeting "healthcare deserts" left by the ongoing wave of rural hospital closures. Preliminary Q1 2026 estimates forecast revenue of $1,415.0 million to $1,455.0 million.

HDIN Institutional Perspective: The "Controlled Company" Dichotomy

While the prospectus highlights software-driven ecosystem lock-ins via the Transport.Net, RapidCall, and Concierge modules (currently embedded in 50% of targeted 911 access points), the structural governance of GMR Solutions presents a severe risk discount for public minority shareholders.

The most critical threat is not operational competition, but rather sponsor financial engineering. Private equity backers (KKR, Ares, HPS) are expected to pledge 60.9% of outstanding common stock (14.7 million shares and 135.7 million warrants) to secure $500 million in margin loans. A market downturn triggering an uncured margin call could force systemic market liquidation of these shares, operating entirely independently of the company's financial fundamentals.

Furthermore, the "controlled company" status (KKR holding 77.5% voting power) is heavily tilted toward wealth extraction. An 85% Tax Receivable Agreement (TRA) will relentlessly drain pre-IPO tax attribute savings to the sponsors, leaving only 15% for corporate liquidity. Simultaneously, GMR Solutions faces escalating labor inflation, with 19 collective bargaining agreements covering 3,300 employees up for renegotiation in 2026, alongside active Civil Investigative Demands (CIDs) from the U.S. Attorney’s Office for the Western District of Tennessee. The Street must price this governance and regulatory overhang against the undeniable FCF generation of its localized clinical monopoly.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Segmental Incremental Margins & Capital Allocation

A forensic audit of the 2025 Form S-1 reveals a highly cash-generative operational core masked by a divestiture-driven top-line contraction. Total 2025 revenue contracted 4.0% to $5,739.8 million due to the strategic divestiture of non-core units, yet the underlying organic transport yield expanded aggressively.

Figure GMR Solutions Inc: Strategic Analysis & FY2025 Financial Overview

Financial Inventory & Operational KPIs (FY 2023 – FY 2025)* Net Transport Revenue: Reached $5,559.6 million in 2025 (96.8% of total revenue), driven by an 11.8% surge in net transport revenue per ambulance to $1,332.

* Operating Leverage: Operating income expanded to $751.6 million, pushing margins to 13.1% in 2025 (up from 6.5% in 2023). Adjusted EBITDA grew at a 25.8% CAGR from 2023 to reach $1,186.2 million.

* Free Cash Flow Conversion: Operating Cash Flow (OCF) surged 160% year-over-year to $641.1 million, comfortably covering the highly disciplined $258.5 million in localized CAPEX.

* Internal Capital Allocation: 0% of the projected $415.2 million IPO proceeds are earmarked for direct R&D or expansion. Instead, $299.4 million is allocated to redeem the 15%-yielding Series B Preferred Stock, while the remaining ~$115.8 million, combined with $500 million from a concurrent Private Placement, will retire $665.8 million of the 2032 First Lien Term Loan (SOFR + 3.50%).

* Interest Rate Sensitivity: The capital stack remains precarious; total debt sits at $5,142.7 million, with a 100-bps increase in interest rates equating to an estimated $46.6 million annual reduction in net earnings.

Unit economics are heavily supported by proprietary technology. The Nurse Navigation platform effectively diverts up to 20% of low-acuity 911 calls to alternate care settings, stripping out profit-draining "dry runs" and generating a 15% decrease in non-transport encounters. This acts as a primary catalyst for margin expansion and improves the commercial payor mix.

Physicality Audit: Supply Chain Vulnerabilities & Geo-Economic Moat

The physical infrastructure of GMR Solutions spans 45 states, covering 62% of the U.S. population with an omnichannel fleet of roughly 7,400 ground vehicles, 400 rotor-wing, and 113 fixed-wing aircraft.

* Backward Integration: Ground fleet resilience is anchored by the Mineral Wells Remount Facility in Texas. This hub enables in-house ambulance overhauls, compressing vehicle capital expenditures by up to 40% compared to new procurement.

* Aviation Sole-Source Bottleneck: Conversely, the aviation supply chain exhibits severe fragility. The company relies on a concentrated oligopoly for helicopters and dynamic engine components, explicitly noting a lack of alternative supply sources. This single-point-of-failure exposes the fleet to FAA airworthiness grounding directives and inflationary part pricing.

* Fuel & Weather Constraints: Macroeconomic variables dictate operational tempo. A 10% swing in commodity fuel prices directly impacts net cash flow by $7 million. Furthermore, 17.2% of emergent air transport requests in 2025 were canceled strictly due to weather, a direct top-line headwind.

* Geographic Expansion: Operations are scheduled to scale with the addition of 15 new rural air bases in 2026, targeting "healthcare deserts" left by the ongoing wave of rural hospital closures. Preliminary Q1 2026 estimates forecast revenue of $1,415.0 million to $1,455.0 million.

HDIN Institutional Perspective: The "Controlled Company" Dichotomy

While the prospectus highlights software-driven ecosystem lock-ins via the Transport.Net, RapidCall, and Concierge modules (currently embedded in 50% of targeted 911 access points), the structural governance of GMR Solutions presents a severe risk discount for public minority shareholders.

The most critical threat is not operational competition, but rather sponsor financial engineering. Private equity backers (KKR, Ares, HPS) are expected to pledge 60.9% of outstanding common stock (14.7 million shares and 135.7 million warrants) to secure $500 million in margin loans. A market downturn triggering an uncured margin call could force systemic market liquidation of these shares, operating entirely independently of the company's financial fundamentals.

Furthermore, the "controlled company" status (KKR holding 77.5% voting power) is heavily tilted toward wealth extraction. An 85% Tax Receivable Agreement (TRA) will relentlessly drain pre-IPO tax attribute savings to the sponsors, leaving only 15% for corporate liquidity. Simultaneously, GMR Solutions faces escalating labor inflation, with 19 collective bargaining agreements covering 3,300 employees up for renegotiation in 2026, alongside active Civil Investigative Demands (CIDs) from the U.S. Attorney’s Office for the Western District of Tennessee. The Street must price this governance and regulatory overhang against the undeniable FCF generation of its localized clinical monopoly.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."