Sunshine Biopharma: Survival Capital Pivot Near Canadian Commercial Hub as $75M Deficit Signals Acute Delisting Risk

Date : 2026-05-15

Reading : 1296

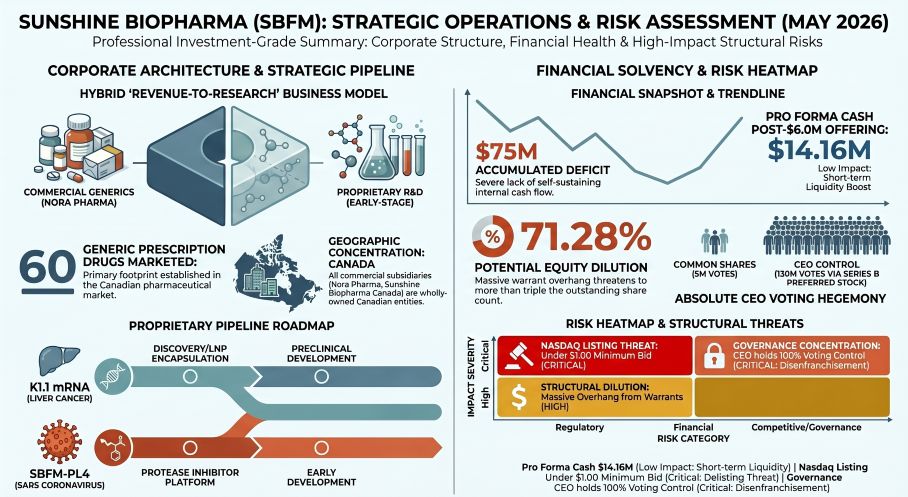

Sunshine Biopharma’s May 2026 S-1 filing reveals a structural liquidity crisis, masking corporate sustenance as a $6.0 million working capital raise. Despite operating a Canadian commercial hub with 60 generic assets, the consolidated entity’s $75 million accumulated deficit highlights an inability to translate generic cash flows into sustainable proprietary R&D runway. For institutional LPs, the immediate threat lies in absolute CEO voting control and a highly dilutive Series C warrant structure that virtually guarantees a "death spiral" anti-dilution event if the impending Nasdaq $1.00 minimum bid requirement forces a reverse split.

Figure SUNSHINE BIOPHARMA (SBFM) :STRATEGIC OPERATIONS & RISK ASSESSMENT

Forensic Analysis of Pro Forma Capitalization and Dilution Mechanics

Forensic Analysis of Pro Forma Capitalization and Dilution Mechanics

The capital structure of NASDAQ: SBFM reveals a severe misalignment with minority shareholder interests, driven by an emergency liquidity injection and an aggressive warrant overhang. The May 2026 S-1 filing omits historical operating cash flows, shifting the analytical focus entirely to balance sheet survival and extreme dilution metrics.

* Pro Forma Liquidity & Baseline Deficit: As of December 31, 2025, the company reported $9,123,308 in cash against a massive accumulated deficit of $75,015,126. The current offering seeks approximately $5.0 million in net proceeds (via 5,825,242 Common Units at $1.03), pushing pro forma cash to $14,163,122. Management explicitly states funds will be allocated for "working capital," confirming the raise is an operational lifeline rather than a strategic R&D deployment.

* The 71.28% Dilution Threat: The issuance of 11,650,484 new Series C Warrants brings the total potential common shares underlying warrants to 26,879,328. If exercised, the fully diluted share count expands to 37,710,515, mathematically triggering a 71.28% reduction in proportional ownership for existing common equity holders.

* Anti-Dilution "Death Spiral" Trigger: The Board has authorized a 1-for-10 reverse stock split to maintain Nasdaq minimum bid compliance. However, executing this split triggers a "Share Combination Event." If the volume-weighted average price drops post-split, Series C warrants automatically adjust downward (with a floor of $0.535, or 50% of the initial offering price) and the issuable share count increases proportionately, exposing common equity to compounded structural erosion.

* Absolute Governance Disenfranchisement: In a highly irregular March 2024 related-party transaction, CEO Dr. Steve N. Slilaty purchased 130,000 shares of Series B Preferred Stock for a nominal $10,000. Carrying 1,000 votes per share, this grants the CEO an insurmountable 130,000,000 votes, stripping institutional and retail investors of any mathematical influence over capital allocation or board composition.

Canadian Commercial Footprint and Third-Party IP Dependency

While the S-1 limits operational disclosures, the geographic and physical supply chain footprint of the enterprise relies heavily on third-party intellectual property and a localized commercial presence.

* Canadian Generics & OTC Distribution: The company’s revenue generation is geographically concentrated in Canada through two wholly-owned subsidiaries. Nora Pharma Inc. manages a portfolio of 60 marketed generic prescription drugs, while Sunshine Biopharma Canada Inc. develops and commercializes OTC supplements.

* External R&D Moat: The internal development pipeline—specifically the K1.1 mRNA (LNP encapsulated mRNA for liver cancer) and SBFM-PL4 (SARS Coronavirus protease inhibitor)—is not supported by an internal patent moat. Instead, the company operates via external IP dependencies, anchored by patent purchase agreements with Advanomics Corporation (funded via Secured Convertible Promissory Notes) and sponsored research/license agreements with the University of Arizona and the University of Georgia. The filings omit CDMO facility names and API supplier dependencies, masking potential geopolitical or single-source vulnerabilities.

HDIN Institutional Perspective

While Sunshine Biopharma promotes a "hybrid model"—theoretically utilizing steady Canadian generic cash flows to fund high-reward oncology and antiviral R&D—the data dictates a contrary reality. The S-1 confirms that commercial generic revenues are entirely insufficient to offset the consolidated entity's burn rate. The decision to raise highly dilutive, non-earmarked public capital merely to cover "general corporate purposes" indicates that the commercial arm is failing to provide non-dilutive funding for K1.1 mRNA or SBFM-PL4. For institutional allocators, investing in this structure means injecting distressed capital into an entity where the CEO retains absolute, unassailable voting control acquired for $10,000, while minority equity absorbs 100% of the reverse-split dilution risk.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure SUNSHINE BIOPHARMA (SBFM) :STRATEGIC OPERATIONS & RISK ASSESSMENT

Forensic Analysis of Pro Forma Capitalization and Dilution MechanicsThe capital structure of NASDAQ: SBFM reveals a severe misalignment with minority shareholder interests, driven by an emergency liquidity injection and an aggressive warrant overhang. The May 2026 S-1 filing omits historical operating cash flows, shifting the analytical focus entirely to balance sheet survival and extreme dilution metrics.

* Pro Forma Liquidity & Baseline Deficit: As of December 31, 2025, the company reported $9,123,308 in cash against a massive accumulated deficit of $75,015,126. The current offering seeks approximately $5.0 million in net proceeds (via 5,825,242 Common Units at $1.03), pushing pro forma cash to $14,163,122. Management explicitly states funds will be allocated for "working capital," confirming the raise is an operational lifeline rather than a strategic R&D deployment.

* The 71.28% Dilution Threat: The issuance of 11,650,484 new Series C Warrants brings the total potential common shares underlying warrants to 26,879,328. If exercised, the fully diluted share count expands to 37,710,515, mathematically triggering a 71.28% reduction in proportional ownership for existing common equity holders.

* Anti-Dilution "Death Spiral" Trigger: The Board has authorized a 1-for-10 reverse stock split to maintain Nasdaq minimum bid compliance. However, executing this split triggers a "Share Combination Event." If the volume-weighted average price drops post-split, Series C warrants automatically adjust downward (with a floor of $0.535, or 50% of the initial offering price) and the issuable share count increases proportionately, exposing common equity to compounded structural erosion.

* Absolute Governance Disenfranchisement: In a highly irregular March 2024 related-party transaction, CEO Dr. Steve N. Slilaty purchased 130,000 shares of Series B Preferred Stock for a nominal $10,000. Carrying 1,000 votes per share, this grants the CEO an insurmountable 130,000,000 votes, stripping institutional and retail investors of any mathematical influence over capital allocation or board composition.

Canadian Commercial Footprint and Third-Party IP Dependency

While the S-1 limits operational disclosures, the geographic and physical supply chain footprint of the enterprise relies heavily on third-party intellectual property and a localized commercial presence.

* Canadian Generics & OTC Distribution: The company’s revenue generation is geographically concentrated in Canada through two wholly-owned subsidiaries. Nora Pharma Inc. manages a portfolio of 60 marketed generic prescription drugs, while Sunshine Biopharma Canada Inc. develops and commercializes OTC supplements.

* External R&D Moat: The internal development pipeline—specifically the K1.1 mRNA (LNP encapsulated mRNA for liver cancer) and SBFM-PL4 (SARS Coronavirus protease inhibitor)—is not supported by an internal patent moat. Instead, the company operates via external IP dependencies, anchored by patent purchase agreements with Advanomics Corporation (funded via Secured Convertible Promissory Notes) and sponsored research/license agreements with the University of Arizona and the University of Georgia. The filings omit CDMO facility names and API supplier dependencies, masking potential geopolitical or single-source vulnerabilities.

HDIN Institutional Perspective

While Sunshine Biopharma promotes a "hybrid model"—theoretically utilizing steady Canadian generic cash flows to fund high-reward oncology and antiviral R&D—the data dictates a contrary reality. The S-1 confirms that commercial generic revenues are entirely insufficient to offset the consolidated entity's burn rate. The decision to raise highly dilutive, non-earmarked public capital merely to cover "general corporate purposes" indicates that the commercial arm is failing to provide non-dilutive funding for K1.1 mRNA or SBFM-PL4. For institutional allocators, investing in this structure means injecting distressed capital into an entity where the CEO retains absolute, unassailable voting control acquired for $10,000, while minority equity absorbs 100% of the reverse-split dilution risk.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."