Amesite: B2B Healthcare Pivot Near Detroit Base as $3.617M Net Loss Signals Urgent Capital Dilution Cycle

Date : 2026-05-15

Reading : 186

Amesite’s May 2026 S-1 filing exposes a precarious transition from legacy EdTech to a highly regulated post-acute healthcare SaaS model. Driven by an approximate $300,000 monthly cash burn and a severe Nasdaq minimum equity deficiency, management engineered an 89% structural share dilution just to maintain market access. For institutional LPs, this represents a textbook distressed pivot. While the NurseMagic platform leverages a zero-integration Product-Led Growth strategy to bypass traditional hospital procurement friction, the total absence of cybersecurity insurance in a HIPAA-governed environment presents an unhedged operational vulnerability.

Figure Amesite Inc's Healthcare Al Transformation

Capital Erosion and Segmental Margin Pivot

Capital Erosion and Segmental Margin Pivot

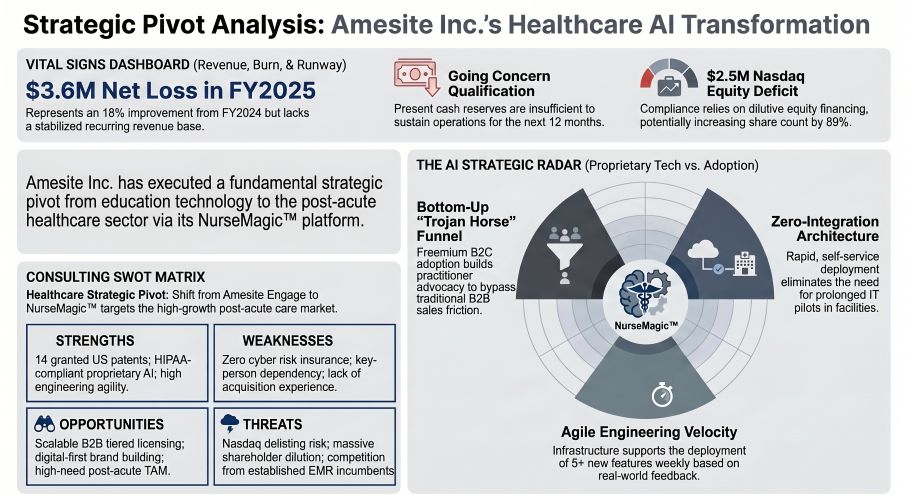

Amesite is navigating a structural operational deficit, having officially ceased growth capital allocation to its legacy "Amesite Engage" education platform in favor of its healthcare-centric "NurseMagic™" application. The following forensic inventory details the severe liquidity constraints and capital dilution mechanics outlined in the May 12, 2026, registration statement:

* Operating Leverage & Bottom-Line Contraction: The company reported a net loss of $3.617 million for FY 2025, an 18% structural improvement from the $4.403 million net loss in FY 2024. Despite this contraction, the implied monthly operational cash burn remains elevated at approximately $301,416.

* Going Concern & Regulatory Deficit: With cash reserves insufficient to fund a 12-month runway, the firm received an October 28, 2025, Nasdaq deficiency notice for failing to maintain the $2,500,000 minimum stockholders’ equity requirement.

* Cap Table Restructuring & Hyper-Dilution: To cure the Nasdaq deficit prior to the April 27, 2026 extension deadline, management executed concurrent private placements and a registered direct offering (closed April 28, 2026). This action registered 4,836,245 resale shares. Assuming full warrant exercise, total outstanding shares will inflate from 5,434,867 to 10,271,112—an 89% expansion in the outstanding share base.

* Internal Capital Allocation: Post-offering insider concentration remains high at approximately 23%, with CEO Dr. Ann Marie Sastry holding an 8.66% beneficial ownership and Director George Parmer holding 3.20%.

The Detroit Engineering Core and HIPAA Moat

Unlike traditional hardware entities, Amesite’s physical supply chain is concentrated in intellectual capital and cloud infrastructure anchored at its 607 Shelby Street, Suite 700 PMB 214, Detroit, Michigan headquarters. The operational "physicality" relies entirely on an agile engineering nexus capable of deploying more than five new platform features per week.

Amesite's geo-economic moat is built upon proprietary AI models trained on selectively curated datasets rather than generalized open-source LLMs. By focusing on the post-acute care market (skilled nursing, hospice, home health), the platform enforces strict HIPAA and CMS compliance natively. The architecture is engineered as a "zero-integration" asset—bypassing the need to interface with legacy Electronic Medical Record (EMR) systems. This self-contained operational model mitigates IT bottlenecks common in institutional healthcare deployments, turning digital workflow agility into a defensible barrier against both legacy EMR providers and mid-market AI entrants.

HDIN Institutional Perspective

While the S-1 frames the "freemium-to-enterprise" NurseMagic funnel as a highly efficient Customer Acquisition Cost (CAC) mitigant, the reality of a sub-12-month runway and zero cyber-liability coverage suggests a fragile architecture that the Street is structurally mispricing.

The strategy to use a free B2C nursing app as a bottom-up Trojan horse to bypass enterprise pilot programs is theoretically sound. However, the 18% YoY net loss reduction was primarily achieved by halting R&D for the legacy EdTech platform, not through stabilized healthcare revenue realization. The admitted lack of any existing cybersecurity risk insurance—despite handling deeply regulated, proprietary medical data—is a catastrophic "orphan risk." Ultimately, the April 2026 financing round did not fund long-term growth; it merely purchased short-term regulatory survival at the cost of massive minority shareholder dilution.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Amesite Inc's Healthcare Al Transformation

Capital Erosion and Segmental Margin PivotAmesite is navigating a structural operational deficit, having officially ceased growth capital allocation to its legacy "Amesite Engage" education platform in favor of its healthcare-centric "NurseMagic™" application. The following forensic inventory details the severe liquidity constraints and capital dilution mechanics outlined in the May 12, 2026, registration statement:

* Operating Leverage & Bottom-Line Contraction: The company reported a net loss of $3.617 million for FY 2025, an 18% structural improvement from the $4.403 million net loss in FY 2024. Despite this contraction, the implied monthly operational cash burn remains elevated at approximately $301,416.

* Going Concern & Regulatory Deficit: With cash reserves insufficient to fund a 12-month runway, the firm received an October 28, 2025, Nasdaq deficiency notice for failing to maintain the $2,500,000 minimum stockholders’ equity requirement.

* Cap Table Restructuring & Hyper-Dilution: To cure the Nasdaq deficit prior to the April 27, 2026 extension deadline, management executed concurrent private placements and a registered direct offering (closed April 28, 2026). This action registered 4,836,245 resale shares. Assuming full warrant exercise, total outstanding shares will inflate from 5,434,867 to 10,271,112—an 89% expansion in the outstanding share base.

* Internal Capital Allocation: Post-offering insider concentration remains high at approximately 23%, with CEO Dr. Ann Marie Sastry holding an 8.66% beneficial ownership and Director George Parmer holding 3.20%.

The Detroit Engineering Core and HIPAA Moat

Unlike traditional hardware entities, Amesite’s physical supply chain is concentrated in intellectual capital and cloud infrastructure anchored at its 607 Shelby Street, Suite 700 PMB 214, Detroit, Michigan headquarters. The operational "physicality" relies entirely on an agile engineering nexus capable of deploying more than five new platform features per week.

Amesite's geo-economic moat is built upon proprietary AI models trained on selectively curated datasets rather than generalized open-source LLMs. By focusing on the post-acute care market (skilled nursing, hospice, home health), the platform enforces strict HIPAA and CMS compliance natively. The architecture is engineered as a "zero-integration" asset—bypassing the need to interface with legacy Electronic Medical Record (EMR) systems. This self-contained operational model mitigates IT bottlenecks common in institutional healthcare deployments, turning digital workflow agility into a defensible barrier against both legacy EMR providers and mid-market AI entrants.

HDIN Institutional Perspective

While the S-1 frames the "freemium-to-enterprise" NurseMagic funnel as a highly efficient Customer Acquisition Cost (CAC) mitigant, the reality of a sub-12-month runway and zero cyber-liability coverage suggests a fragile architecture that the Street is structurally mispricing.

The strategy to use a free B2C nursing app as a bottom-up Trojan horse to bypass enterprise pilot programs is theoretically sound. However, the 18% YoY net loss reduction was primarily achieved by halting R&D for the legacy EdTech platform, not through stabilized healthcare revenue realization. The admitted lack of any existing cybersecurity risk insurance—despite handling deeply regulated, proprietary medical data—is a catastrophic "orphan risk." Ultimately, the April 2026 financing round did not fund long-term growth; it merely purchased short-term regulatory survival at the cost of massive minority shareholder dilution.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."