Duke Robotics: Pivot to Dual-Use AEROTRACE Services Near Tel Aviv as 249% Revenue Surge Signals Validation of Partner-Funded Margin Model

Date : 2026-05-15

Reading : 353

Duke Robotics’ 2025 S-1 exposes an extreme asset-light transition, translating a negligible $104,000 R&D spend into a commercial-stage robotics operator. While Elbit Systems absorbs heavy defense manufacturing CapEx, Duke retains high-margin royalties from kinetic deployments. For institutional LPs, the KPMG “going concern” warning and $750,000 liquidity cliff present severe near-term execution risks. However, the impending $8.0 million Nasdaq uplisting offering provides a 3.5-year cash runway bridge, directly converting military battlefield validation into recurring AI-driven utility maintenance contracts across European grids.

Figure Duke Robotics (DUKR): The Strategic Inflection Point in Precision Drone Tech

Capital Structure Compression & Dual-Use Operating Leverage

Capital Structure Compression & Dual-Use Operating Leverage

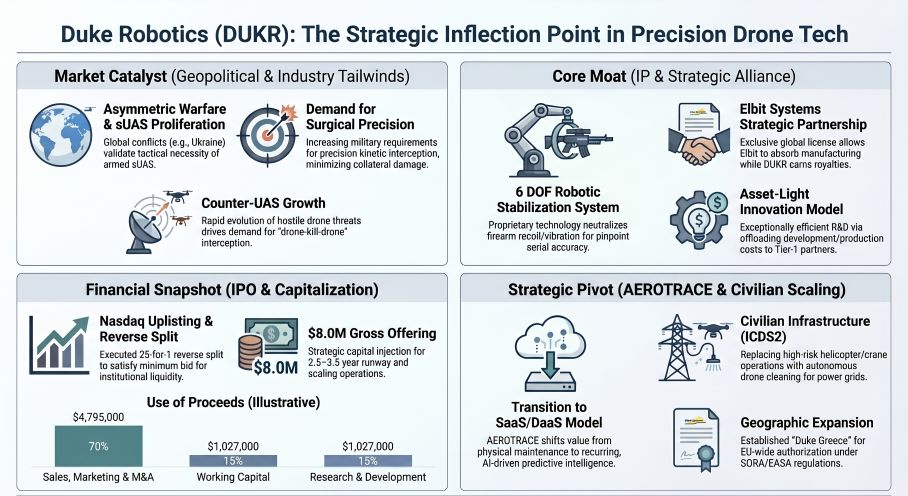

Duke Robotics (OTCQB: DUKE) demonstrates an asymmetrical R&D-to-Moat translation. By offloading serial production to NASDAQ: ESLT (Elbit Systems Land Ltd.), the firm achieved critical commercial milestones despite a 33% YoY contraction in R&D expenditure (dropping from $157,000 in 2024 to $104,000 in 2025). The internal capital allocation and segmental economics breakdown as follows:

* Top-Line & Margin Inflection: FY2025 revenue reached $377,000 (+249% YoY from $108,000), driven by a >$1,000,000 initial order commitment from the Israel Electric Corporation (IEC) for the ICDS2 platform and the first recognition of Q2 2025 defense royalties. Gross profit expanded to $179,000 (47.4% margin).

* Operating Leverage & Burn: SG&A surged 41.5% to $1.28 million, widening the net loss from $985,000 to $1.24 million. However, core cash used in operations tightened from $(918,000) to $(811,000), indicating early working capital stabilization.

* Liquidity Squeeze & Solvency: Cash plummeted to $750,000 against current liabilities of $756,000 (net working capital of $151,000). The accumulated deficit sits at $12.4 million, triggering KPMG's formal going concern qualification.

* Capital Allocation ($8.0M Offering): Target pricing at $10.50/unit for 761,905 units yields $6.85 million net. Post the March 6, 2026, 25-for-1 reverse split, 70% ($4.79 million) of proceeds are earmarked for sales force expansion and M&A, extending the implied cash runway by 2.5 to 3.5 years.

* Equity Overhang & Anti-Takeover: New investors face an immediate net tangible book value dilution of $8.18 per share. 731,394 warrants and 319,876 options remain outstanding. Furthermore, 10,000,000 "blank check" preferred shares function as a structural poison pill.

Middle Eastern Concentration vs. European Expansion

Duke Robotics’ physical footprint is highly localized, operating a bifurcated supply chain that isolates defense risk while exposing civilian hardware to global macro constraints.

* Logistics Hubs & Physicality: Final assembly, integration, and testing of the ICDS2 platform occur strictly in-house at the Tel Aviv laboratory. Custom-machined parts are sourced from approximately 20 Tier-1 suppliers across Israel, the United States, Europe, and China.

* Regulatory Hurdles & Defense Moat: The "Bird of Prey" (legacy TIKAD) defense system avoids direct manufacturing bottlenecks because Elbit Systems finances the serial production lines. Elbit recoups its CapEx via a $6,000,000 max offset cap, withholding 50% of DUKE's low-to-mid-double-digit royalties (which run until a $50,000,000 milestone is met). However, all defense exports are bound by strict Israeli Ministry of Defense (IMOD) licensing, presenting severe geopolitical delay risks.

* Expansion & Macro Choke Points: Civilian operations are aggressively pivoting to the EU. On January 13, 2026, the newly established Duke Robotics Hellas M I.K.E secured Hellenic Civil Aviation Authority (HCAA) authorization under the EU's SORA framework. Conversely, supply routes face physical risks from Iranian-backed Houthi Red Sea shipping attacks, and civilian expansion faces regulatory friction from the American Security Drone Act (ASDA), which bans U.S. federal agencies from procuring Chinese-sourced drone components.

HDIN Institutional Perspective

We challenge the Street's potential framing of Duke Robotics as a pure-play hardware innovator. A differentiated viewpoint of the S-1 reveals that Duke is effectively an IP-holding and data-analytics entity heavily levered to third-party manufacturing. While the February 2026 launch of AEROTRACE™ promises high-margin, recurring Data-as-a-Service (DaaS) revenue, the company's hardware supply chain remains structurally un-sanitized for the lucrative U.S. federal market. Furthermore, the explicit lack of non-compete clauses with its Chinese and European hardware suppliers suggests the core algorithmic moat is legally vulnerable. Despite the February 26, 2026 dismissal of the LOOL T.V. litigation, the IP architecture is thin (relying on a single 2021 USPTO patent and unprotected trade secrets). If the $8.0 million capital injection fails to secure aggressive European civilian grid contracts before the Chief Technology Officer's 20,000 ($5.25 strike) and 4,000 ($7.88 strike) options begin their 2026-2029 vesting cliffs, the underlying equity value faces severe compression.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Duke Robotics (DUKR): The Strategic Inflection Point in Precision Drone Tech

Capital Structure Compression & Dual-Use Operating Leverage Duke Robotics (OTCQB: DUKE) demonstrates an asymmetrical R&D-to-Moat translation. By offloading serial production to NASDAQ: ESLT (Elbit Systems Land Ltd.), the firm achieved critical commercial milestones despite a 33% YoY contraction in R&D expenditure (dropping from $157,000 in 2024 to $104,000 in 2025). The internal capital allocation and segmental economics breakdown as follows:

* Top-Line & Margin Inflection: FY2025 revenue reached $377,000 (+249% YoY from $108,000), driven by a >$1,000,000 initial order commitment from the Israel Electric Corporation (IEC) for the ICDS2 platform and the first recognition of Q2 2025 defense royalties. Gross profit expanded to $179,000 (47.4% margin).

* Operating Leverage & Burn: SG&A surged 41.5% to $1.28 million, widening the net loss from $985,000 to $1.24 million. However, core cash used in operations tightened from $(918,000) to $(811,000), indicating early working capital stabilization.

* Liquidity Squeeze & Solvency: Cash plummeted to $750,000 against current liabilities of $756,000 (net working capital of $151,000). The accumulated deficit sits at $12.4 million, triggering KPMG's formal going concern qualification.

* Capital Allocation ($8.0M Offering): Target pricing at $10.50/unit for 761,905 units yields $6.85 million net. Post the March 6, 2026, 25-for-1 reverse split, 70% ($4.79 million) of proceeds are earmarked for sales force expansion and M&A, extending the implied cash runway by 2.5 to 3.5 years.

* Equity Overhang & Anti-Takeover: New investors face an immediate net tangible book value dilution of $8.18 per share. 731,394 warrants and 319,876 options remain outstanding. Furthermore, 10,000,000 "blank check" preferred shares function as a structural poison pill.

Middle Eastern Concentration vs. European Expansion

Duke Robotics’ physical footprint is highly localized, operating a bifurcated supply chain that isolates defense risk while exposing civilian hardware to global macro constraints.

* Logistics Hubs & Physicality: Final assembly, integration, and testing of the ICDS2 platform occur strictly in-house at the Tel Aviv laboratory. Custom-machined parts are sourced from approximately 20 Tier-1 suppliers across Israel, the United States, Europe, and China.

* Regulatory Hurdles & Defense Moat: The "Bird of Prey" (legacy TIKAD) defense system avoids direct manufacturing bottlenecks because Elbit Systems finances the serial production lines. Elbit recoups its CapEx via a $6,000,000 max offset cap, withholding 50% of DUKE's low-to-mid-double-digit royalties (which run until a $50,000,000 milestone is met). However, all defense exports are bound by strict Israeli Ministry of Defense (IMOD) licensing, presenting severe geopolitical delay risks.

* Expansion & Macro Choke Points: Civilian operations are aggressively pivoting to the EU. On January 13, 2026, the newly established Duke Robotics Hellas M I.K.E secured Hellenic Civil Aviation Authority (HCAA) authorization under the EU's SORA framework. Conversely, supply routes face physical risks from Iranian-backed Houthi Red Sea shipping attacks, and civilian expansion faces regulatory friction from the American Security Drone Act (ASDA), which bans U.S. federal agencies from procuring Chinese-sourced drone components.

HDIN Institutional Perspective

We challenge the Street's potential framing of Duke Robotics as a pure-play hardware innovator. A differentiated viewpoint of the S-1 reveals that Duke is effectively an IP-holding and data-analytics entity heavily levered to third-party manufacturing. While the February 2026 launch of AEROTRACE™ promises high-margin, recurring Data-as-a-Service (DaaS) revenue, the company's hardware supply chain remains structurally un-sanitized for the lucrative U.S. federal market. Furthermore, the explicit lack of non-compete clauses with its Chinese and European hardware suppliers suggests the core algorithmic moat is legally vulnerable. Despite the February 26, 2026 dismissal of the LOOL T.V. litigation, the IP architecture is thin (relying on a single 2021 USPTO patent and unprotected trade secrets). If the $8.0 million capital injection fails to secure aggressive European civilian grid contracts before the Chief Technology Officer's 20,000 ($5.25 strike) and 4,000 ($7.88 strike) options begin their 2026-2029 vesting cliffs, the underlying equity value faces severe compression.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."