Cortigent: Strategic CMO Transition Near Valencia R&D Hub as Accelerating $833k Quarterly Cash Burn Signals Make-or-Break 2027 Clinical Timelines

Date : 2026-05-17

Reading : 84

Cortigent’s 2026 S-1 reveals a precarious 18-month post-IPO liquidity window built on $13.375 million in estimated net proceeds. Operating with a formal "going concern" qualification and an $833,000 Q1 2026 cash burn, the Valencia-based entity is racing against a looming 2029 intellectual property cliff for its Orion®system. For institutional LPs, the critical pivot from internal manufacturing to a dual U.S. Contract Manufacturing Organization (CMO) model dictates survival. If Cortigent fails to secure FDA clearance and resolve single-source supply bottlenecks before 2027, its $10 billion TAM narrative faces systemic collapse.

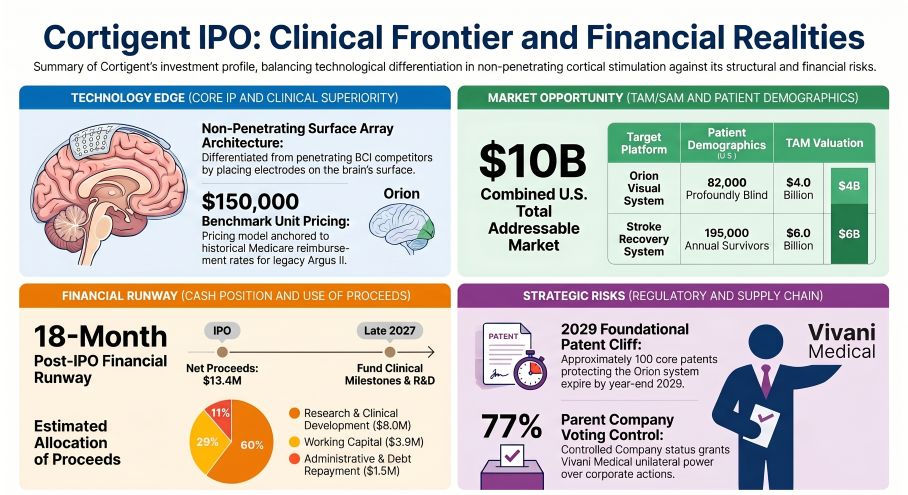

Figure Cortigent lPO: Clinical Frontier and Financial Realities

Quantifying the 18-Month Liquidity Window

Quantifying the 18-Month Liquidity Window

Cortigent’s internal capital allocation reflects a highly speculative, pre-revenue burn profile heavily subsidized by its parent, Vivani Medical. The proposed initial public offering acts as a mandatory liquidity event to fund R&D up to the 2027 pivotal clinical trial commencement. Unit economics demand a premium $150,000 target price per device—benchmarked against the legacy Argus II®Medicare reimbursement rate—to capture the estimated $4 billion Artificial Vision TAM (82,000 U.S. patients) and $6 billion Stroke Recovery TAM (195,000 U.S. patients).

Operational Leverage & IPO Proceeds Allocation:

* Total Expected Net Proceeds:$13.375 million (assuming $10.00/share).

* R&D & Clinical Development (60%):$8.0 million ($3.0M for Orion/Stroke R&D, $1.0M for Orion pivotal trial preparation, $4.0M for clinical device manufacturing).

* Administrative & Debt Reduction (40%):$5.375 million ($3.875M general working capital; $1.5M direct repayment to Vivaniunder the Transition Funding Agreement).

Table Segmental Financial Inventory (FY24 – Q1 2026):

The Valencia-to-Houston Clinical Corridor

Cortigent executes a "virtual technology" R&D footprint anchored at 27200 Tourney Road, Valencia, California. The clinical validation nodes for the 60-channel Orion®surface array are highly localized, utilizing the Ronald Reagan UCLA Medical Center (Los Angeles)and Baylor College of Medicine (Houston)for the 6-year Early Feasibility Study (EFS).

The physicality of Cortigent's supply chain reveals acute, systemic risks. The firm lacks commercial-scale manufacturing capacity and remains entirely captive to four Tier-1 "sole-source" providers for its 60-channel flexible circuit arrays and hermetically sealed bio-compatible cases:

* Thin Film Industries, Inc.:Sole provider of trace metallization on ceramic substrates.

* Morgan Advanced Materials plc:Exclusive supplier for brazing ceramic substrates to metal device walls.

* Nusil Technology LLC:Sole supplier of critical silicone over-molding for neuro-protection.

* UHV Sputtering, Inc.:Exclusive provider of metal deposition on flexible circuits.

Any failure in executing the planned shift to two specialized U.S.-based CMOs before the late 2027 FDA Investigational Device Exemption (IDE) window will trigger cascading delays, directly threatening the 2030 (Orion) and 2031 (Stroke) commercial launch projections.

HDIN Institutional Perspective

While the S-1 filing touts a robust 147 U.S. patent portfolio and a combined $10 billion TAM, the operational realities present a highly asymmetric risk profile. We challenge management's narrative of a streamlined path to commercialization. The 50% clinical attrition rate observed in the Orion EFS—where 3 of 6 patients requested device explantation for reasons unrelated to safety or efficacy—exposes a severe BCI patient-retention headwind that the Street has not adequately priced into the modeling.

Furthermore, the post-IPO governance structure entrenches Vivaniwith 77% voting power under the "Controlled Company" exemption. Relying on $1.5 million of the $13.375 million IPO proceeds to immediately repay parent entity advances, while operating with a meager $428,000 in Q1 2026 cash, signals a defensive capital extraction by the parent. This mechanism structurally transfers disproportionate developmental risk onto minority public shareholders just as Cortigent races against the expiration of approximately 100 foundational U.S. patents in 2029.

Presentation Download & Video Access:

Presentation Download:Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link:Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Cortigent lPO: Clinical Frontier and Financial Realities

Quantifying the 18-Month Liquidity WindowCortigent’s internal capital allocation reflects a highly speculative, pre-revenue burn profile heavily subsidized by its parent, Vivani Medical. The proposed initial public offering acts as a mandatory liquidity event to fund R&D up to the 2027 pivotal clinical trial commencement. Unit economics demand a premium $150,000 target price per device—benchmarked against the legacy Argus II®Medicare reimbursement rate—to capture the estimated $4 billion Artificial Vision TAM (82,000 U.S. patients) and $6 billion Stroke Recovery TAM (195,000 U.S. patients).

Operational Leverage & IPO Proceeds Allocation:

* Total Expected Net Proceeds:$13.375 million (assuming $10.00/share).

* R&D & Clinical Development (60%):$8.0 million ($3.0M for Orion/Stroke R&D, $1.0M for Orion pivotal trial preparation, $4.0M for clinical device manufacturing).

* Administrative & Debt Reduction (40%):$5.375 million ($3.875M general working capital; $1.5M direct repayment to Vivaniunder the Transition Funding Agreement).

Table Segmental Financial Inventory (FY24 – Q1 2026):

| Financial Metric | FY 2024 | FY 2025 | Q1 2026 |

|---|---|---|---|

| R&D Expense | $324,000 | $570,000 | $118,000 |

| G&A Expense | $1,752,000 | $2,062,000 | $608,000 |

| Net Loss | $(2,232,000) | $(3,112,000) | $(768,000) |

| Operating Cash Burn | $(2,175,000) | $(2,712,000) | $(833,000) |

| Cash & Cash Equivalents | $797,000 | $467,000 | $428,000 |

| Working Capital Deficit | — | — | $(3,753,000) (as of Q1 2026) |

The Valencia-to-Houston Clinical Corridor

Cortigent executes a "virtual technology" R&D footprint anchored at 27200 Tourney Road, Valencia, California. The clinical validation nodes for the 60-channel Orion®surface array are highly localized, utilizing the Ronald Reagan UCLA Medical Center (Los Angeles)and Baylor College of Medicine (Houston)for the 6-year Early Feasibility Study (EFS).

The physicality of Cortigent's supply chain reveals acute, systemic risks. The firm lacks commercial-scale manufacturing capacity and remains entirely captive to four Tier-1 "sole-source" providers for its 60-channel flexible circuit arrays and hermetically sealed bio-compatible cases:

* Thin Film Industries, Inc.:Sole provider of trace metallization on ceramic substrates.

* Morgan Advanced Materials plc:Exclusive supplier for brazing ceramic substrates to metal device walls.

* Nusil Technology LLC:Sole supplier of critical silicone over-molding for neuro-protection.

* UHV Sputtering, Inc.:Exclusive provider of metal deposition on flexible circuits.

Any failure in executing the planned shift to two specialized U.S.-based CMOs before the late 2027 FDA Investigational Device Exemption (IDE) window will trigger cascading delays, directly threatening the 2030 (Orion) and 2031 (Stroke) commercial launch projections.

HDIN Institutional Perspective

While the S-1 filing touts a robust 147 U.S. patent portfolio and a combined $10 billion TAM, the operational realities present a highly asymmetric risk profile. We challenge management's narrative of a streamlined path to commercialization. The 50% clinical attrition rate observed in the Orion EFS—where 3 of 6 patients requested device explantation for reasons unrelated to safety or efficacy—exposes a severe BCI patient-retention headwind that the Street has not adequately priced into the modeling.

Furthermore, the post-IPO governance structure entrenches Vivaniwith 77% voting power under the "Controlled Company" exemption. Relying on $1.5 million of the $13.375 million IPO proceeds to immediately repay parent entity advances, while operating with a meager $428,000 in Q1 2026 cash, signals a defensive capital extraction by the parent. This mechanism structurally transfers disproportionate developmental risk onto minority public shareholders just as Cortigent races against the expiration of approximately 100 foundational U.S. patents in 2029.

Presentation Download & Video Access:

Presentation Download:Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link:Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."