Lokotech Group AS: Fabless Hardware Pivot Near Kautokeino Hydropower Hub as $13.34M CapEx Signals Imminent Scrypt ASIC Commercialization

Date : 2026-05-17

Reading : 78

Lokotech Group AS is executing a high-stakes transition from an R&D incubator to a vertically integrated semiconductor manufacturer. While FY2025 filings show near-perfect gross margins (~99.9%) driven entirely by mining pool software revenues, this conceals a highly capital-intensive fabless hardware reality. With $7.09 million prepaid for an undisclosed foundry’s mask set, the firm’s structural moat relies entirely on translating its proprietary design into a sub-0.1 J/MH efficiency metric. For institutional LPs, the thesis hinges on whether localized Norwegian hydropower deployments and impending AI-blockchain convergence can offset the execution risk of H2 2026 hardware deliveries.

Forensic Financial Audit & Segmental Incremental Margins

The 2025 financial profile reflects a severe divergence between software-driven cash flow and hardware-driven Capital Expenditure (CapEx). Internal capital allocation aggressively favors R&D-to-moat translation, while legacy non-core assets (e.g., Arctic Core AS server leasing and Filecoin operations) are being systematically liquidated.

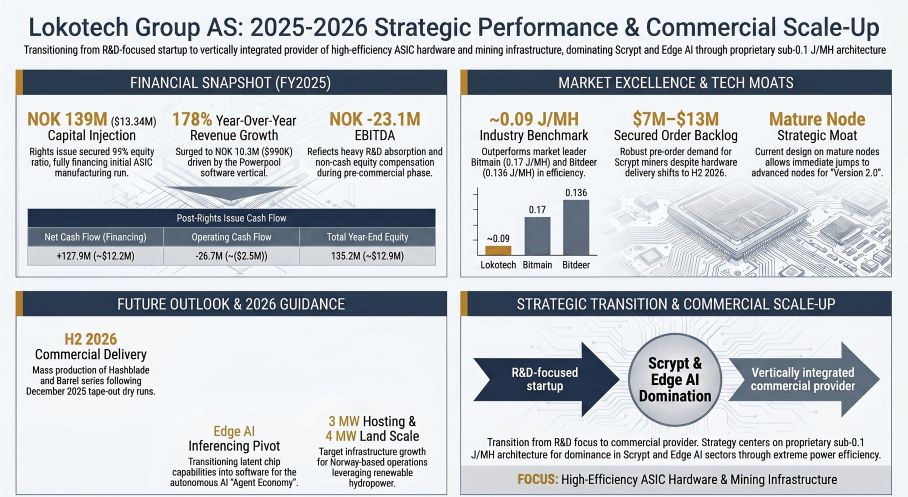

Figure Lokotech Group AS: 2025-2026 Strategic Performance & Commercial Scale-Up

Segmental Revenue & Price-Mix Variance

Segmental Revenue & Price-Mix Variance

* Software & Services (Powerpool Mining SL): Generated 100% of the Group’s commercial revenue at €874,219 ($988,392). Average daily net revenue scaled to €2,395 ($2,708), achieving a 54% YoY increase despite a harsh price-mix variance in H2 2025 (a 40-60% drop in underlying Litecoin/Dogecoin spot prices). The pool added 5,112 new users, bringing total clients to 10,815. In H1 2025, the subsidiary paid out €400,000 ($452,240) in dividends.

* Hardware (Lokotech AS): Pre-revenue ($0) in 2025. Holds a secured pre-order backlog of $7 million to $13 million. Technical delays resulted in heavily contained order cancellations of merely ~$53,000.

* Geographic Split: Extreme borderless distribution. Norway generated just $1,536 (NOK 16,010; <0.2%), while global markets generated $989,381 (NOK 10,309,355; >99.8%).

Quantitative Ledger: Profitability & FCF Conversion

The balance sheet transition is financed via a highly dilutive but structurally necessary NOK 139 million (~$13.34 million) Rights Issue.

* Top-Line & OPEX: Consolidated group revenue printed at NOK 10,309,355 (178% YoY growth from NOK 3,708,945). Total operating expenses scaled to NOK 44,793,825.

* Cost Structure: Payroll consumed NOK 17,209,472 (distorted by a NOK 7,869,872 non-cash option expense). Other OPEX equaled NOK 16,236,117. COGS sat at a negligible NOK 5,595, yielding a ~99.9% transitional gross margin.

* Earnings & R&D Burn: D&A printed at NOK 11,342,641, heavily weighted by ASIC R&D depreciation (NOK 8,482,668 / $813,997). The firm capitalized NOK 3,420,000 ($327,982) in hardware development and NOK 1,860,000 ($179,045) in new development additions. Combined R&D run-rate equates to 115.4% of total group revenue.

* Net Margins: EBITDA registered at NOK -23,125,819. EBIT was NOK -34,468,460. Net Profit fell to NOK -36,803,557, generating a Return on Equity (ROE) of -27.2%.

* Cash Flow: Operating Cash Flow (OCF) burned NOK -26,727,265. Investing Cash Flow bled NOK -77,062,393, fully offset by Financing Cash Flow of +NOK 127,938,668.

* Liquidity & Solvency: Current Assets sit at NOK 118,039,669 (Cash: NOK 37,002,186; Receivables: NOK 79,313,338) against Current Liabilities of NOK 7,066,059, driving a 16.7x current ratio. Total Liabilities are strictly short-term at NOK 7,113,319 against Total Equity of NOK 135,200,751. Debt-to-Equity is 5.26%; Equity Ratio is a robust 95.00%. Deferred tax assets of NOK 32.6 million ($3.13 million) are conservatively kept off-balance sheet.

* Impairments: NOK 10,053,200 in parent intra-group writedowns, including a NOK 2,050,000 hit on Nordic Green Datacenter AS. A NOK 898,822 direct Bitcoin treasury investment was impaired to zero. Fully depreciated legacy patents hold a $0 book value (historical cost NOK 133,367 / $12,798).

Geo-Economic Supply Chain Audit & Physical Moat

Lokotech’s architectural superiority must navigate severe execution risks tethered to physical supply chains. The business physicality relies on localized renewable energy hedging against global semiconductor cyclicality.

Sourcing Dependencies & Yield Risk

Lokotech operates as a fabless semiconductor entity. A massive NOK 73,884,074 ($7.09 million) prepayment is deployed for the physical ASIC mask set at an unnamed third-party foundry. Following design modifications triggered by third-party EDA library updates, the ASIC initiated tape-out dry runs on December 15, 2025. Management identifies "re-spins" (mask set corrections) as the primary existential risk. The firm is aggressively hoarding "long lead-time components" to insulate against Middle East geopolitical friction and shipping bottlenecks. Simultaneously, the smart PSU-module is undergoing critical pilot testing with an external customer in the United States.

Unit Economics vs. Peer-Group Spreads

The hardware moat depends entirely on power efficiency. Lokotech targets 0.09 J/MH. This functionally obsoletes the current top 5 market players:

* Bitmain (Private): 0.17 - 0.21 J/MH (L9, L11 Pro/Hyd)

* NASDAQ: BTDR (Bitdeer): 0.136 - 0.149 J/MH (SEAL-DL1)

* ElphaPex: 0.27 - 0.31 J/MH

* VolcMiner: 0.18 - 0.25 J/MH

* Goldshell: 0.53 - 0.96 J/MH

Hardware is segmented into modular deployments: *Hashblade* (1.55 GH/s at 144W), *Single Barrel* (9.32 GH/s at 880W), and *Double Barrel* (18.64 GH/s at 1,835W). This efficiency lowers the operational viability threshold to extreme asset price floors (e.g., $30-$50 LTC).

Infrastructure Footprint & Regulatory Hedging

Lokotech mitigates operational carbon footprint via its domestic hubs. Hardware testing and future 2-5 MW data center builds are aggressively expanding in Kautokeino and Telemark, Northern Norway, targeting a summer 2026 launch. The Powerpool Hosting pilot launched here was oversubscribed by 400%. To hedge against active Norwegian political hostility toward energy-intensive Proof-of-Work operations, management relies heavily on European Economic Area (EEA) compliance and local grid stabilization narratives (e.g., capturing stranded energy via Mobile Distributed Computing Units and reusing office server waste heat at the Oslo HQ).

Governance & Insider Capital Allocation

Corporate governance reflects high insider alignment but carries massive equity overhangs.

* Executive Remuneration: Highly conservative base capital outflow. CEO Ola Stene-Johansen's base salary is $104,336 (NOK 1,087,184). Aggregate Board fees equal $143,954 (NOK 1,500,000). There are zero executive loans or severance packages.

* Insider Ownership: The CEO controls 23.58 million shares and 6 million options. Chairman Yngve Johansen controls 7.62 million shares, and Board Member Ståle Flataker controls 10.47 million shares. A minor related-party transaction involves $4,318 (NOK 45,000) in rent paid to a Chairman-controlled entity. (An off-balance sheet HQ lease running June 2021–June 2026 costs $80,033 / NOK 833,948).

* Contingent Liabilities & Overhang: The cap table contains 45.55 million outstanding options (structured with flexible strikes to offset employer tax) and 54 million outstanding "in-the-money" warrants, threatening substantial dilution upon exercise. The firm carries zero pending litigations and maintains NOK 10 million in executive liability insurance. The core team consists of five males reporting 0% sick leave, though Board representation includes female IT veteran Kristin Åbyholm alongside technical experts Susheel Nuguru, Hans Jørgen Fosse, Christian Rustad, and CFO Christoffer Løvdal.

HDIN Institutional Perspective: A High-Wire Transition Masked by Pure-Play Software Optics

While the 2025 filings project a pristine ~99.9% margin software operation with SOC 2 compliance, this financial optic is strictly transitional. Lokotech is structurally a hardware-intensive semiconductor firm racing against a ticking clock.

The $13.34 million Rights Issue provides essential life support, but the true enterprise value is entirely bottlenecked at the unnamed foundry. By utilizing a "relatively mature production node" rather than bleeding-edge fabrication, Lokotech inherently limits baseline execution failure but heavily increases the risk of market-share erosion. If Bitmain or NASDAQ: BTDR release an intermediate-node hardware update before Lokotech’s H2 2026 delivery window, the $7-$13 million backlog will evaporate.

However, if Lokotech successfully transitions its hardware from TRL 6 to TRL 8 without a mask set re-spin, its sub-0.1 J/MH metric will dominate the Scrypt hardware sector. The macro thesis is sound: amid a $348 trillion global public debt crisis, autonomous AI agents require sub-cent (<$0.01) transaction finality (e.g., Litecoin's 2.5-minute blocks and LitVM smart contracts). If Lokotech captures this M2M "Agent Economy" convergence, the warrant-induced dilution will be fully absorbed by exponential infrastructure yield.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Forensic Financial Audit & Segmental Incremental Margins

The 2025 financial profile reflects a severe divergence between software-driven cash flow and hardware-driven Capital Expenditure (CapEx). Internal capital allocation aggressively favors R&D-to-moat translation, while legacy non-core assets (e.g., Arctic Core AS server leasing and Filecoin operations) are being systematically liquidated.

Figure Lokotech Group AS: 2025-2026 Strategic Performance & Commercial Scale-Up

Segmental Revenue & Price-Mix Variance* Software & Services (Powerpool Mining SL): Generated 100% of the Group’s commercial revenue at €874,219 ($988,392). Average daily net revenue scaled to €2,395 ($2,708), achieving a 54% YoY increase despite a harsh price-mix variance in H2 2025 (a 40-60% drop in underlying Litecoin/Dogecoin spot prices). The pool added 5,112 new users, bringing total clients to 10,815. In H1 2025, the subsidiary paid out €400,000 ($452,240) in dividends.

* Hardware (Lokotech AS): Pre-revenue ($0) in 2025. Holds a secured pre-order backlog of $7 million to $13 million. Technical delays resulted in heavily contained order cancellations of merely ~$53,000.

* Geographic Split: Extreme borderless distribution. Norway generated just $1,536 (NOK 16,010; <0.2%), while global markets generated $989,381 (NOK 10,309,355; >99.8%).

Quantitative Ledger: Profitability & FCF Conversion

The balance sheet transition is financed via a highly dilutive but structurally necessary NOK 139 million (~$13.34 million) Rights Issue.

* Top-Line & OPEX: Consolidated group revenue printed at NOK 10,309,355 (178% YoY growth from NOK 3,708,945). Total operating expenses scaled to NOK 44,793,825.

* Cost Structure: Payroll consumed NOK 17,209,472 (distorted by a NOK 7,869,872 non-cash option expense). Other OPEX equaled NOK 16,236,117. COGS sat at a negligible NOK 5,595, yielding a ~99.9% transitional gross margin.

* Earnings & R&D Burn: D&A printed at NOK 11,342,641, heavily weighted by ASIC R&D depreciation (NOK 8,482,668 / $813,997). The firm capitalized NOK 3,420,000 ($327,982) in hardware development and NOK 1,860,000 ($179,045) in new development additions. Combined R&D run-rate equates to 115.4% of total group revenue.

* Net Margins: EBITDA registered at NOK -23,125,819. EBIT was NOK -34,468,460. Net Profit fell to NOK -36,803,557, generating a Return on Equity (ROE) of -27.2%.

* Cash Flow: Operating Cash Flow (OCF) burned NOK -26,727,265. Investing Cash Flow bled NOK -77,062,393, fully offset by Financing Cash Flow of +NOK 127,938,668.

* Liquidity & Solvency: Current Assets sit at NOK 118,039,669 (Cash: NOK 37,002,186; Receivables: NOK 79,313,338) against Current Liabilities of NOK 7,066,059, driving a 16.7x current ratio. Total Liabilities are strictly short-term at NOK 7,113,319 against Total Equity of NOK 135,200,751. Debt-to-Equity is 5.26%; Equity Ratio is a robust 95.00%. Deferred tax assets of NOK 32.6 million ($3.13 million) are conservatively kept off-balance sheet.

* Impairments: NOK 10,053,200 in parent intra-group writedowns, including a NOK 2,050,000 hit on Nordic Green Datacenter AS. A NOK 898,822 direct Bitcoin treasury investment was impaired to zero. Fully depreciated legacy patents hold a $0 book value (historical cost NOK 133,367 / $12,798).

Geo-Economic Supply Chain Audit & Physical Moat

Lokotech’s architectural superiority must navigate severe execution risks tethered to physical supply chains. The business physicality relies on localized renewable energy hedging against global semiconductor cyclicality.

Sourcing Dependencies & Yield Risk

Lokotech operates as a fabless semiconductor entity. A massive NOK 73,884,074 ($7.09 million) prepayment is deployed for the physical ASIC mask set at an unnamed third-party foundry. Following design modifications triggered by third-party EDA library updates, the ASIC initiated tape-out dry runs on December 15, 2025. Management identifies "re-spins" (mask set corrections) as the primary existential risk. The firm is aggressively hoarding "long lead-time components" to insulate against Middle East geopolitical friction and shipping bottlenecks. Simultaneously, the smart PSU-module is undergoing critical pilot testing with an external customer in the United States.

Unit Economics vs. Peer-Group Spreads

The hardware moat depends entirely on power efficiency. Lokotech targets 0.09 J/MH. This functionally obsoletes the current top 5 market players:

* Bitmain (Private): 0.17 - 0.21 J/MH (L9, L11 Pro/Hyd)

* NASDAQ: BTDR (Bitdeer): 0.136 - 0.149 J/MH (SEAL-DL1)

* ElphaPex: 0.27 - 0.31 J/MH

* VolcMiner: 0.18 - 0.25 J/MH

* Goldshell: 0.53 - 0.96 J/MH

Hardware is segmented into modular deployments: *Hashblade* (1.55 GH/s at 144W), *Single Barrel* (9.32 GH/s at 880W), and *Double Barrel* (18.64 GH/s at 1,835W). This efficiency lowers the operational viability threshold to extreme asset price floors (e.g., $30-$50 LTC).

Infrastructure Footprint & Regulatory Hedging

Lokotech mitigates operational carbon footprint via its domestic hubs. Hardware testing and future 2-5 MW data center builds are aggressively expanding in Kautokeino and Telemark, Northern Norway, targeting a summer 2026 launch. The Powerpool Hosting pilot launched here was oversubscribed by 400%. To hedge against active Norwegian political hostility toward energy-intensive Proof-of-Work operations, management relies heavily on European Economic Area (EEA) compliance and local grid stabilization narratives (e.g., capturing stranded energy via Mobile Distributed Computing Units and reusing office server waste heat at the Oslo HQ).

Governance & Insider Capital Allocation

Corporate governance reflects high insider alignment but carries massive equity overhangs.

* Executive Remuneration: Highly conservative base capital outflow. CEO Ola Stene-Johansen's base salary is $104,336 (NOK 1,087,184). Aggregate Board fees equal $143,954 (NOK 1,500,000). There are zero executive loans or severance packages.

* Insider Ownership: The CEO controls 23.58 million shares and 6 million options. Chairman Yngve Johansen controls 7.62 million shares, and Board Member Ståle Flataker controls 10.47 million shares. A minor related-party transaction involves $4,318 (NOK 45,000) in rent paid to a Chairman-controlled entity. (An off-balance sheet HQ lease running June 2021–June 2026 costs $80,033 / NOK 833,948).

* Contingent Liabilities & Overhang: The cap table contains 45.55 million outstanding options (structured with flexible strikes to offset employer tax) and 54 million outstanding "in-the-money" warrants, threatening substantial dilution upon exercise. The firm carries zero pending litigations and maintains NOK 10 million in executive liability insurance. The core team consists of five males reporting 0% sick leave, though Board representation includes female IT veteran Kristin Åbyholm alongside technical experts Susheel Nuguru, Hans Jørgen Fosse, Christian Rustad, and CFO Christoffer Løvdal.

HDIN Institutional Perspective: A High-Wire Transition Masked by Pure-Play Software Optics

While the 2025 filings project a pristine ~99.9% margin software operation with SOC 2 compliance, this financial optic is strictly transitional. Lokotech is structurally a hardware-intensive semiconductor firm racing against a ticking clock.

The $13.34 million Rights Issue provides essential life support, but the true enterprise value is entirely bottlenecked at the unnamed foundry. By utilizing a "relatively mature production node" rather than bleeding-edge fabrication, Lokotech inherently limits baseline execution failure but heavily increases the risk of market-share erosion. If Bitmain or NASDAQ: BTDR release an intermediate-node hardware update before Lokotech’s H2 2026 delivery window, the $7-$13 million backlog will evaporate.

However, if Lokotech successfully transitions its hardware from TRL 6 to TRL 8 without a mask set re-spin, its sub-0.1 J/MH metric will dominate the Scrypt hardware sector. The macro thesis is sound: amid a $348 trillion global public debt crisis, autonomous AI agents require sub-cent (<$0.01) transaction finality (e.g., Litecoin's 2.5-minute blocks and LitVM smart contracts). If Lokotech captures this M2M "Agent Economy" convergence, the warrant-induced dilution will be fully absorbed by exponential infrastructure yield.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."