Nauticus Robotics: Solvency Crisis at Webster Headquarters as $250 Million Equity Facility Signals 95% Theoretical Dilution

Date : 2026-05-17

Reading : 94

Nauticus Robotics faces an existential liquidity crisis marked by a formal going concern warning and reliance on highly dilutive capital mechanisms. While pitching an autonomous subsea robotics moat targeting U.S. defense and Brazilian energy markets, the financial architecture heavily favors institutional creditors. For institutional LPs, the firm's $250 million variable-price equity facility mathematically caps upside. This transforms what is marketed as a defense-tech growth play into a distressed-debt restructuring vehicle, exposing common equity to a toxic financing spiral.

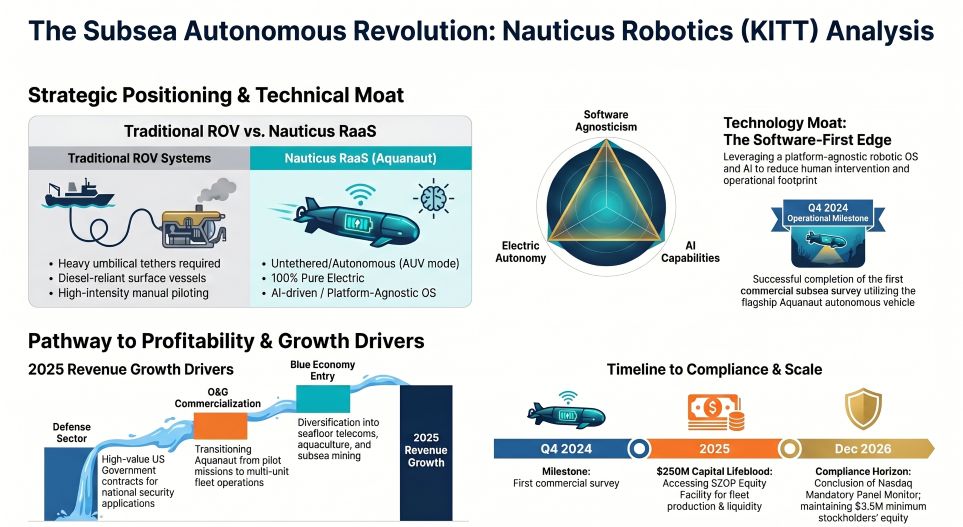

Figure The Subsea Autonomous Revolution: Nauticus Robotics (KITT) Analysis

Forensic Analysis of Capital Structure & Dilution Mechanics

Forensic Analysis of Capital Structure & Dilution Mechanics

A forensic audit of the May 2026 S-1 registration statement reveals an internal capital allocation engineered primarily for debt recovery. The company's fully diluted capitalization structure illustrates extreme dilution overhang, projecting a 95.53% theoretical dilution rate against the current float. Operating leverage is non-existent as internal controls exhibit a formal "material weakness."

Quantitative Inventory & Balance Sheet Metrics:

* Share Structure Contraction: A 1-for-8 reverse stock split executed on April 21, 2026, contracted outstanding common stock to 5,002,925 shares (as of May 11, 2026), generating a baseline market capitalization of $12.06 million at a $2.41 share price.

* The $250M Overhang: An Equity Purchase Facility Agreement (EPFA) with SZOP Opportunities I LLC spans 24 months, registering up to 103,734,439 shares. The facility is constrained by a 9.99% beneficial ownership limitation and a floating market price mechanism.

* Punitive Preferred Stock Triggers: The capital stack includes Series A (40,000 designated; 5% dividend), Series B (50,000 designated; 10% dividend), and Series C (100,000 designated; 10% dividend) preferred stock. A "Bankruptcy Triggering Event" forces cash redemption at a 1.25x premium for Series A, and a 25% premium for Series B/C, while automatically spiking default dividend rates to 18%.

* Convertible Debt & Conversion Pricing: Outstanding derivative securities include 242,424 shares from convertible debentures and 86,024 shares from term loans. Preferred holders possess "Alternate Conversion" rights pegged to 98% of the lowest 10-day Volume Weighted Average Price (VWAP), virtually guaranteeing aggressive equity saturation if the stock price drops.

* Historical Debt-to-Equity Swaps: In 2024 and 2025, structural reliance on secured debt included conversions of $2.55 million and $3.0 million term loans, alongside a Q1 2026 issuance of $1.02 million and $2.0 million in institutional convertible notes.

* Regulatory Deadlines: NASDAQ: KITT operates under a Mandatory Panel Monitor until December 19, 2026, requiring the maintenance of a $3.5 million minimum stockholders’ equity each fiscal quarter to avoid delisting.

Subsea Supply Chain Vulnerabilities & Geo-Economic Constraints

Despite claims of a software-first approach utilizing its ToolKITT robotic operating system, the company is fundamentally constrained by hardware manufacturing limitations and geopolitical exposure.

* Geographic Footprint: Operations are centralized at the principal executive headquarters located at 17146 Feathercraft Lane, Suite 450, Webster, Texas 77598. International operations are anchored by Nauticus Robotics Brazil Ltda., which executed a strategic agreement with Petróleo Brasileiro S.A. (Petrobras) on May 23, 2023.

* Supply Chain & Manufacturing: Commercialization of the flagship Aquanaut® (an autonomous, untethered underwater vehicle) relies on highly specialized, single-source vendors for electric robotic manipulators. Management explicitly notes that large-scale manufacturing capacity remains "unproven."

* Government Contract Concentration: The company is strategically pivoted toward U.S. defense applications and government entities. These contracts are highly volatile, frequently only partially funded, subject to immediate termination, and exposed to rigorous federal audits.

* Inorganic Growth: The balance sheet absorbed assets from SeaTrepid International, L.L.C. via an Asset Purchase Agreement executed in March 2025, though unit economics surrounding this integration remain opaque.

HDIN Institutional Verdict

While retail investors may focus on the proprietary autonomous hardware narratives, the SEC filings indicate that NASDAQ: KITT is structurally impaired. The presence of ATW Special Situations functioning simultaneously as a senior secured creditor and a dominant equity holder—having previously converted a principal value of $2.19 million into 22.64 million shares—creates a severe governance and capital conflict.

The EPFA is not a growth mechanism; it is a defensive liquidity facility. If the stock price experiences downward pressure, the floating purchase price mechanism and the 98% VWAP alternate conversion clauses on preferred stock will force the issuance of exponentially more shares. This mathematically engineers a capital market "death spiral," suggesting that current valuations severely misprice the execution and solvency risk profile.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

Figure The Subsea Autonomous Revolution: Nauticus Robotics (KITT) Analysis

Forensic Analysis of Capital Structure & Dilution MechanicsA forensic audit of the May 2026 S-1 registration statement reveals an internal capital allocation engineered primarily for debt recovery. The company's fully diluted capitalization structure illustrates extreme dilution overhang, projecting a 95.53% theoretical dilution rate against the current float. Operating leverage is non-existent as internal controls exhibit a formal "material weakness."

Quantitative Inventory & Balance Sheet Metrics:

* Share Structure Contraction: A 1-for-8 reverse stock split executed on April 21, 2026, contracted outstanding common stock to 5,002,925 shares (as of May 11, 2026), generating a baseline market capitalization of $12.06 million at a $2.41 share price.

* The $250M Overhang: An Equity Purchase Facility Agreement (EPFA) with SZOP Opportunities I LLC spans 24 months, registering up to 103,734,439 shares. The facility is constrained by a 9.99% beneficial ownership limitation and a floating market price mechanism.

* Punitive Preferred Stock Triggers: The capital stack includes Series A (40,000 designated; 5% dividend), Series B (50,000 designated; 10% dividend), and Series C (100,000 designated; 10% dividend) preferred stock. A "Bankruptcy Triggering Event" forces cash redemption at a 1.25x premium for Series A, and a 25% premium for Series B/C, while automatically spiking default dividend rates to 18%.

* Convertible Debt & Conversion Pricing: Outstanding derivative securities include 242,424 shares from convertible debentures and 86,024 shares from term loans. Preferred holders possess "Alternate Conversion" rights pegged to 98% of the lowest 10-day Volume Weighted Average Price (VWAP), virtually guaranteeing aggressive equity saturation if the stock price drops.

* Historical Debt-to-Equity Swaps: In 2024 and 2025, structural reliance on secured debt included conversions of $2.55 million and $3.0 million term loans, alongside a Q1 2026 issuance of $1.02 million and $2.0 million in institutional convertible notes.

* Regulatory Deadlines: NASDAQ: KITT operates under a Mandatory Panel Monitor until December 19, 2026, requiring the maintenance of a $3.5 million minimum stockholders’ equity each fiscal quarter to avoid delisting.

Subsea Supply Chain Vulnerabilities & Geo-Economic Constraints

Despite claims of a software-first approach utilizing its ToolKITT robotic operating system, the company is fundamentally constrained by hardware manufacturing limitations and geopolitical exposure.

* Geographic Footprint: Operations are centralized at the principal executive headquarters located at 17146 Feathercraft Lane, Suite 450, Webster, Texas 77598. International operations are anchored by Nauticus Robotics Brazil Ltda., which executed a strategic agreement with Petróleo Brasileiro S.A. (Petrobras) on May 23, 2023.

* Supply Chain & Manufacturing: Commercialization of the flagship Aquanaut® (an autonomous, untethered underwater vehicle) relies on highly specialized, single-source vendors for electric robotic manipulators. Management explicitly notes that large-scale manufacturing capacity remains "unproven."

* Government Contract Concentration: The company is strategically pivoted toward U.S. defense applications and government entities. These contracts are highly volatile, frequently only partially funded, subject to immediate termination, and exposed to rigorous federal audits.

* Inorganic Growth: The balance sheet absorbed assets from SeaTrepid International, L.L.C. via an Asset Purchase Agreement executed in March 2025, though unit economics surrounding this integration remain opaque.

HDIN Institutional Verdict

While retail investors may focus on the proprietary autonomous hardware narratives, the SEC filings indicate that NASDAQ: KITT is structurally impaired. The presence of ATW Special Situations functioning simultaneously as a senior secured creditor and a dominant equity holder—having previously converted a principal value of $2.19 million into 22.64 million shares—creates a severe governance and capital conflict.

The EPFA is not a growth mechanism; it is a defensive liquidity facility. If the stock price experiences downward pressure, the floating purchase price mechanism and the 98% VWAP alternate conversion clauses on preferred stock will force the issuance of exponentially more shares. This mathematically engineers a capital market "death spiral," suggesting that current valuations severely misprice the execution and solvency risk profile.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*