Animal Diagnostics 2026 Outlook: Why IDEXX, Zoetis, and Neogen Diverge on Capital Allocation Amid EU IVDR Constraints and Tariff Realignments

Date : 2026-05-16

Reading : 241

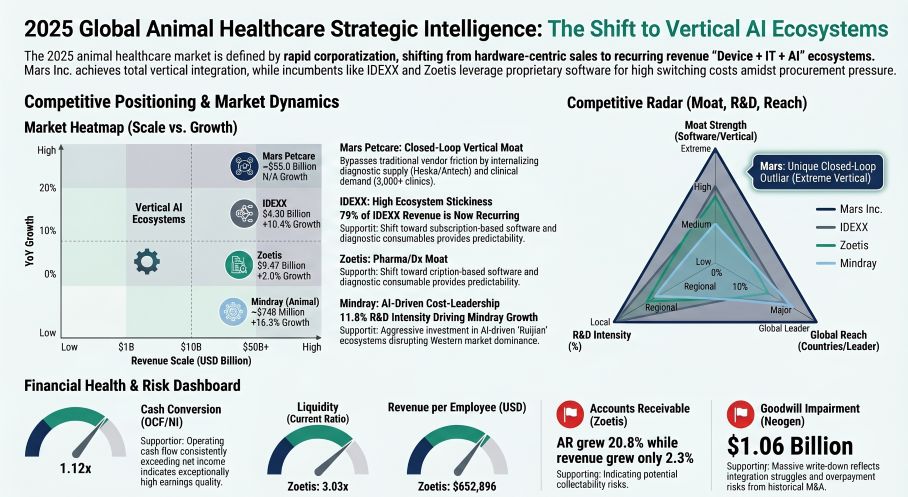

The 2025 animal diagnostics sector reveals a stark bifurcation in earnings quality, significantly distorted by M&A integration failures and macroeconomic friction. While leaders aggressively funnel R&D into AI-driven point-of-care (POC) ecosystems to defend recurring revenue, working capital anomalies—notably a 20.8% Accounts Receivable spike against 2.3% revenue growth at NYSE: ZTS—signal potential collectability risks. For institutional LPs, the critical variable heading into 2026 is no longer hardware placement, but structural resilience against tightening EU IVDR regulations, China's volume-based procurement (VBP), and escalating tariff frameworks.

Figure 2025 Global Animal Healthcare Strategic Intelligence: The Shift to Vertical Al Ecosystems

Segmental Financials & Earnings Hygiene

Segmental Financials & Earnings Hygiene

An audit of 2025 disclosures highlights severe divergences in cash conversion ratios (Operating Cash Flow / Net Income) and catastrophic capital destruction among mid-cap entities. The sector pivots heavily from physical capacity expansion toward recurring consumable revenue, which accounted for approximately 40% of targeted revenue at SZSE: 300760 and $1.496 billion globally for NASDAQ: IDXX.

* Zoetis (NYSE: ZTS): Reported $2,673 million in Net Income and $2,904 million in OCF (1.09x Cash Conversion). Liquidity remains high with $2,312 million in cash and a 3.03x current ratio, alongside long-term debt of $9,042 million vs. equity of $3,331 million (D/E: 2.71x). *Red Flag Indicator:* Accounts Receivable surged 20.8% year-over-year (from $1,316 million to $1,590 million), heavily outpacing total revenue growth of 2.3% ($9,256 million to $9,467 million). Allowance for doubtful accounts remains flat at $16 million. R&D spending hit $698 million (7% of revenue), with Capex at $621 million.

* IDEXX Laboratories (NASDAQ: IDXX): Generated $1,059.5 million in Net Income against $1,181.8 million OCF (1.12x Cash Conversion). AR grew 16.6% ($473.6 million to $552.4 million), closely tracking a 10.4% revenue increase. Structural efficiency is evident: $847.8 million in debt against $1,605.4 million in equity (D/E: 0.53x) and a 1.23x current ratio. 2025 Capex reached $124.68 million, projected to rise to $180.0 million in 2026 for customer-facing software. The firm capitalized $36.5 million in internal-use software against $251.2 million in R&D (5.8% of revenue). POC recurring revenues reached $1.84 billion ($348.9 million from rapid assays), while Reference Lab services generated $1.42 billion.

* Neogen Corporation (NASDAQ: NEOG): Suffered a Net Loss of $(1,092.0) million, driven by a catastrophic $1.06 billion non-cash goodwill impairment tied to the 3M Food Safety integration. OCF remained positive at $58.2 million. The balance sheet shows $894.1 million in total debt against $2,071.3 million in equity (D/E: 0.43x) with a 3.31x current ratio. R&D stood at $21.1 million; Capex at $104.6 million. In July 2025, it divested its Cleaners and Disinfectants business to Kersia Group for $130 million.

* Mindray (SZSE: 300760): Delivered CNY 8,451.5 million (~$1,175.8 million) in Net Income, maintaining overall gross margins of 60.3%. R&D intensity reached 11.8% of revenue at $546.62 million (CNY 3.93 billion). Direct sales to key accounts represented 11.6% of revenue (~$535.6 million).

* Zomedica Corp. (NYSE American: ZOM): Distressed earnings quality with a Net Loss of $(81.9) million, heavily penalized by $55.8 million in goodwill impairments ($45.6 million specifically tied to PulseVet and Assisi in Q1 2025). Highly liquid but operationally vulnerable: $53.2 million in cash/securities against ~$11.0 million in liabilities (5.80x current ratio, ~0.0x D/E). Consumable revenues grew from $17.66 million to $20.67 million. Instrument carrying value was recorded at $9,545. R&D was $7.17 million.

* BioNote (KOSPI: 377740): Executed a lean 2025 Capex of $2.77 million (KRW 3.93 billion), anticipating $4.71 million (KRW 6.7 billion) in 2026 for ERP systems. R&D totaled $11.89 million (KRW 16.9 billion). Acquired a 23.04% equity stake in CTC Bio for $10.07 million (KRW 14.3 billion) in January 2025.

Diagnostic Hardware Base & Proprietary Technology Unit Economics

* IDEXX: Commands an installed base of 164,000 premium diagnostic instruments (78,000 Catalyst; 56,000 Premium Hematology; 24,000 SediVue Dx; 6,000 inVue Dx).

* Mindray: Aggressively capturing high-throughput share with 756 units of the BS-2800M chemistry analyzer (+50% YoY), 1,035 units of the CL-8000i immunoassay analyzer, and 270 installations (out of 360 orders) for the MT 8000 automation line.

* Strategic Pipeline Dates: NASDAQ: IDXX plans to expand its North American Cancer Dx Panel to include canine mast cell tumors by 2026. NYSE American: ZOM schedules the advanced AI upgrade for its TRUVIEW hematology system for January 2026.

Supply Chain Audit & Geo-Economic Moat

The physical footprint of the industry is actively restructuring to hedge against strict geopolitical barriers, namely a U.S. 10% baseline/125% reciprocal tariff on Chinese imports, EU IVDR certification hurdles, and the EU Artificial Intelligence Act.

* Localized Manufacturing: SZSE: 300760 bypassed tariff friction by initiating localized production projects across 14 countries (11 currently active). KOSPI: 377740 directed its facility Capex specifically to U.S. and India outposts.

* Service Delivery Hubs & Single-Point Vulnerabilities: NASDAQ: NEOG operates a decentralized service model through 6 global laboratories (U.S., Scotland, Brazil, Australia, China, Canada), but faced severe supply chain backlogs due to a disrupted SAP ERP implementation and elevated write-offs. NYSE: ZTS consolidated its U.K. and Ireland reference lab footprint by acquiring the Veterinary Pathology Group (VPG). Meanwhile, NYSE American: ZOM maintains a highly vulnerable bottleneck, relying on a single supplier (Qorvo) for TRUFORMA BAW sensors, despite acquiring Qorvo Biotechnologies to internalize manufacturing.

* Regulatory Ceilings: China’s DRG/DIP and Volume-Based Procurement (VBP) mandates are aggressively capping margins on IVD reagents, forcing a consolidation that favors scaled operators. Concurrently, data localization frameworks (GDPR, China’s Personal Information Protection Law) are restricting the cross-border data transfers necessary for training AI platforms like NYSE: ZTS’s Vetscan Imagyst "AI Masses" and Mindray’s QiYuan AI model.

HDIN Institutional Perspective

While the Street aggressively prices the "software-defined" ecosystems of these diagnostic giants, the underlying forensic data suggests structural vulnerabilities ignored by consensus models. We challenge the unimpeded growth narrative surrounding NYSE: ZTS; an Accounts Receivable balance expanding nearly 10x faster than top-line revenue is a classical precursor to channel stuffing or distributor distress, presenting a material working capital risk that their $16 million doubtful accounts provision fails to adequately cover. Furthermore, the catastrophic $1.06 billion impairment at NASDAQ: NEOG and the $55.8 million write-off at NYSE American: ZOM expose a systemic flaw in the industry's M&A playbook: historical overpayment for growth assets that fundamentally fail to integrate. As the sector transitions to Phase 3 Algorithmic Clinical Decision Support, LPs must discount hardware projections and prioritize entities demonstrating localized supply chain resilience and strict cash conversion hygiene.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure 2025 Global Animal Healthcare Strategic Intelligence: The Shift to Vertical Al Ecosystems

Segmental Financials & Earnings HygieneAn audit of 2025 disclosures highlights severe divergences in cash conversion ratios (Operating Cash Flow / Net Income) and catastrophic capital destruction among mid-cap entities. The sector pivots heavily from physical capacity expansion toward recurring consumable revenue, which accounted for approximately 40% of targeted revenue at SZSE: 300760 and $1.496 billion globally for NASDAQ: IDXX.

* Zoetis (NYSE: ZTS): Reported $2,673 million in Net Income and $2,904 million in OCF (1.09x Cash Conversion). Liquidity remains high with $2,312 million in cash and a 3.03x current ratio, alongside long-term debt of $9,042 million vs. equity of $3,331 million (D/E: 2.71x). *Red Flag Indicator:* Accounts Receivable surged 20.8% year-over-year (from $1,316 million to $1,590 million), heavily outpacing total revenue growth of 2.3% ($9,256 million to $9,467 million). Allowance for doubtful accounts remains flat at $16 million. R&D spending hit $698 million (7% of revenue), with Capex at $621 million.

* IDEXX Laboratories (NASDAQ: IDXX): Generated $1,059.5 million in Net Income against $1,181.8 million OCF (1.12x Cash Conversion). AR grew 16.6% ($473.6 million to $552.4 million), closely tracking a 10.4% revenue increase. Structural efficiency is evident: $847.8 million in debt against $1,605.4 million in equity (D/E: 0.53x) and a 1.23x current ratio. 2025 Capex reached $124.68 million, projected to rise to $180.0 million in 2026 for customer-facing software. The firm capitalized $36.5 million in internal-use software against $251.2 million in R&D (5.8% of revenue). POC recurring revenues reached $1.84 billion ($348.9 million from rapid assays), while Reference Lab services generated $1.42 billion.

* Neogen Corporation (NASDAQ: NEOG): Suffered a Net Loss of $(1,092.0) million, driven by a catastrophic $1.06 billion non-cash goodwill impairment tied to the 3M Food Safety integration. OCF remained positive at $58.2 million. The balance sheet shows $894.1 million in total debt against $2,071.3 million in equity (D/E: 0.43x) with a 3.31x current ratio. R&D stood at $21.1 million; Capex at $104.6 million. In July 2025, it divested its Cleaners and Disinfectants business to Kersia Group for $130 million.

* Mindray (SZSE: 300760): Delivered CNY 8,451.5 million (~$1,175.8 million) in Net Income, maintaining overall gross margins of 60.3%. R&D intensity reached 11.8% of revenue at $546.62 million (CNY 3.93 billion). Direct sales to key accounts represented 11.6% of revenue (~$535.6 million).

* Zomedica Corp. (NYSE American: ZOM): Distressed earnings quality with a Net Loss of $(81.9) million, heavily penalized by $55.8 million in goodwill impairments ($45.6 million specifically tied to PulseVet and Assisi in Q1 2025). Highly liquid but operationally vulnerable: $53.2 million in cash/securities against ~$11.0 million in liabilities (5.80x current ratio, ~0.0x D/E). Consumable revenues grew from $17.66 million to $20.67 million. Instrument carrying value was recorded at $9,545. R&D was $7.17 million.

* BioNote (KOSPI: 377740): Executed a lean 2025 Capex of $2.77 million (KRW 3.93 billion), anticipating $4.71 million (KRW 6.7 billion) in 2026 for ERP systems. R&D totaled $11.89 million (KRW 16.9 billion). Acquired a 23.04% equity stake in CTC Bio for $10.07 million (KRW 14.3 billion) in January 2025.

Diagnostic Hardware Base & Proprietary Technology Unit Economics

* IDEXX: Commands an installed base of 164,000 premium diagnostic instruments (78,000 Catalyst; 56,000 Premium Hematology; 24,000 SediVue Dx; 6,000 inVue Dx).

* Mindray: Aggressively capturing high-throughput share with 756 units of the BS-2800M chemistry analyzer (+50% YoY), 1,035 units of the CL-8000i immunoassay analyzer, and 270 installations (out of 360 orders) for the MT 8000 automation line.

* Strategic Pipeline Dates: NASDAQ: IDXX plans to expand its North American Cancer Dx Panel to include canine mast cell tumors by 2026. NYSE American: ZOM schedules the advanced AI upgrade for its TRUVIEW hematology system for January 2026.

Supply Chain Audit & Geo-Economic Moat

The physical footprint of the industry is actively restructuring to hedge against strict geopolitical barriers, namely a U.S. 10% baseline/125% reciprocal tariff on Chinese imports, EU IVDR certification hurdles, and the EU Artificial Intelligence Act.

* Localized Manufacturing: SZSE: 300760 bypassed tariff friction by initiating localized production projects across 14 countries (11 currently active). KOSPI: 377740 directed its facility Capex specifically to U.S. and India outposts.

* Service Delivery Hubs & Single-Point Vulnerabilities: NASDAQ: NEOG operates a decentralized service model through 6 global laboratories (U.S., Scotland, Brazil, Australia, China, Canada), but faced severe supply chain backlogs due to a disrupted SAP ERP implementation and elevated write-offs. NYSE: ZTS consolidated its U.K. and Ireland reference lab footprint by acquiring the Veterinary Pathology Group (VPG). Meanwhile, NYSE American: ZOM maintains a highly vulnerable bottleneck, relying on a single supplier (Qorvo) for TRUFORMA BAW sensors, despite acquiring Qorvo Biotechnologies to internalize manufacturing.

* Regulatory Ceilings: China’s DRG/DIP and Volume-Based Procurement (VBP) mandates are aggressively capping margins on IVD reagents, forcing a consolidation that favors scaled operators. Concurrently, data localization frameworks (GDPR, China’s Personal Information Protection Law) are restricting the cross-border data transfers necessary for training AI platforms like NYSE: ZTS’s Vetscan Imagyst "AI Masses" and Mindray’s QiYuan AI model.

HDIN Institutional Perspective

While the Street aggressively prices the "software-defined" ecosystems of these diagnostic giants, the underlying forensic data suggests structural vulnerabilities ignored by consensus models. We challenge the unimpeded growth narrative surrounding NYSE: ZTS; an Accounts Receivable balance expanding nearly 10x faster than top-line revenue is a classical precursor to channel stuffing or distributor distress, presenting a material working capital risk that their $16 million doubtful accounts provision fails to adequately cover. Furthermore, the catastrophic $1.06 billion impairment at NASDAQ: NEOG and the $55.8 million write-off at NYSE American: ZOM expose a systemic flaw in the industry's M&A playbook: historical overpayment for growth assets that fundamentally fail to integrate. As the sector transitions to Phase 3 Algorithmic Clinical Decision Support, LPs must discount hardware projections and prioritize entities demonstrating localized supply chain resilience and strict cash conversion hygiene.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."