Mindray Bio-Medical: 'Flow-Based' Consumables Pivot Near Shenzhen and Wuhan Hubs as 23% Domestic Contraction Signals Systemic Capex Repricing

Date : 2026-05-16

Reading : 455

Mindray’s 2025 revenue contraction to $4.63 billion reflects severe macro headwinds in Mainland China, where Volume-Based Procurement (VBP) and DRG implementations triggered a 23% domestic top-line decline. For institutional LPs, the critical narrative is not the cyclical cap-ex compression, but the structural pivot. Mindray is accelerating a highly sticky "flow-based" consumable model, now 40% of revenue, shielded by aggressive vertical M&A. This strategic shift, backed by a 1.20x cash conversion ratio, effectively hedges against localized procurement barriers like the EU IPI and US tariff volatility ahead of 2026.

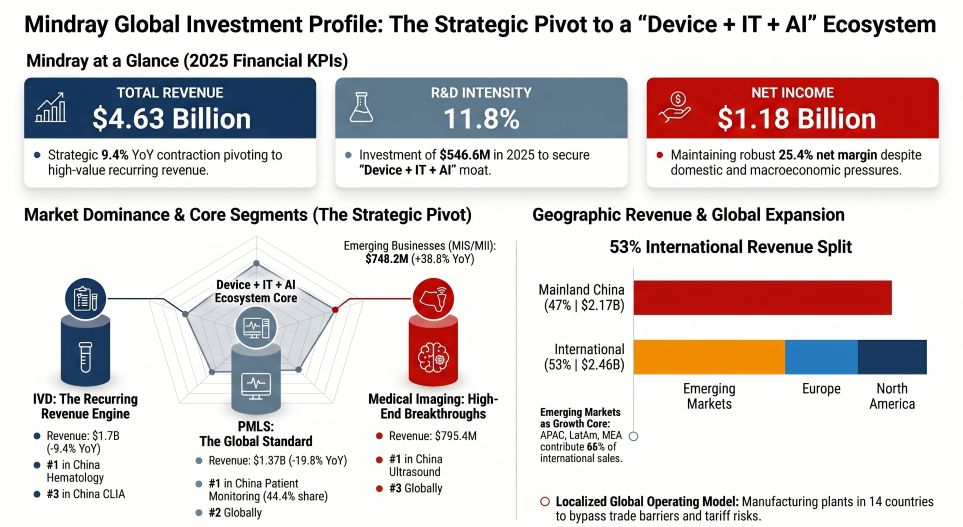

Figure Mindray Global Investment Profile: The Strategic Pivot to a Device + IT + AI Ecosystem

Segmental Incremental Margins and Internal Capital Allocation

Segmental Incremental Margins and Internal Capital Allocation

Operating under the ticker SZSE: 300760, Mindray's 2025 financials expose a distinct bifurcation: traditional heavy-metal capital expenditures are eroding under policy pressure, while integrated consumables and M&A-driven emerging lines represent the definitive growth vector. Despite top-line contraction, the company's capital structure remains highly unleveraged, providing a fortress balance sheet for sustained global acquisitions.

* Top-Line & Profitability Variance: Total 2025 revenue contracted 9.4% YoY to $4,630.56 million (CNY 33,282.2 million), dragging net profit down 28.0% YoY to $1,175.86 million. Gross margins compressed longitudinally from 64.2% (2023) to 60.3% (2025), largely driven by domestic VBP pricing re-baselines.

* Operating Leverage & Cash Conversion: Earnings quality remains impeccable. The 2025 Operating Cash Flow (OCF) stood at $1,411.47 million against net profits of $1,175.86 million—a conversion ratio of 1.20x. High cash generation is insulated by an ultra-conservative gearing ratio of 27.4%, with near-zero long-term interest-bearing bank debt ($0.67 million) and $2,452.16 million in cash reserves.

* Segmental Inventory & Unit Economics:

* *In-Vitro Diagnostics (IVD):* $1,703.05 million (36.8% of Rev). Gross margins compressed to 58.3%. Production: 59.7K equipment units and 27.49 million reagent units. Strategy hinges on high-frequency reagent consumption offsetting hardware ASP declines.

* *Patient Monitoring and Life Support (PMLS):* $1,368.59 million (29.6% of Rev). Down 19.8% YoY; 584.0K units produced. Margin dropped to 59.4%. Hurt by delayed replacement cycles and tightened public hospital budgets.

* *Medical Imaging Systems:* $795.37 million (17.2% of Rev). Down 18.0% YoY; 44.0K units produced. Squeezed by domestic anti-corruption scrutiny on large tenders, partially offset by overseas Resona A20 traction.

* *Emerging Business (MIS, MII, Animal Care):* The sole hyper-growth pillar, generating $748.24 million (+38.8% YoY). Margins expanded to 63.7%, bolstered by the $1.06 billion integration of Huitai Medical (which independently generated $359.5 million in 2025 revenue).

* R&D-to-Moat Translation: R&D expenditure structurally increased to $546.63 million (11.8% of revenue) in 2025. The portfolio commands 12,983 patent applications (72.39% invention-based).

Supply Chain Physicality and Post-2026 Trade Resilience

Mindray’s physical footprint is systematically detaching from single-market reliance. International revenues now command 53.0% of the total ($2,455.7 million), with Emerging Markets acting as the anchor (34.8% of total revenue).

* Domestic Manufacturing & Dark Factories: Mindray is transitioning its core production bases in Shenzhen, Nanjing, Dangshan, and Wuhan into fully automated, IIoT-driven "dark factories." However, proactive global expansion has temporarily suppressed capacity utilization (e.g., PMLS dropped to 55.4% in 2025, IVD equipment to 64.9%).

* Geopolitical Hedging & Localization: To circumvent the EU’s International Procurement Instrument (IPI)—which restricts Chinese entities from public bids over $5.65 million (EUR 5 million)—and the US 30% retaliatory tariff truce (expiring Nov 2026), Mindray has established local production projects across 14 countries.

* Supply Chain Autonomy: Supplier concentration is statistically negligible. The top five suppliers account for just 6.0% ($111.15 million) of procurement. Crucially, direct dependency on US-imported raw materials is capped below 5%, neutralizing immediate "chokehold" sanctions risk. The acquisitions of HyTest (Finland) and DiaSys (Germany) further internalized critical upstream IVD antigens and overseas logistics.

HDIN Institutional Perspective

While Mindray's prospectus heavily markets its "Device + IT + AI" ecosystem and the "Qi Yuan" LLMs as high-switching-cost SaaS equivalents, forensic financial data suggests a divergent reality. The 119.1% surge in goodwill to $1,543.41 million—primarily from the Huitai Medical acquisition—indicates that future growth is increasingly purchased through capital-intensive M&A rather than organically engineered software adoption. Furthermore, with inventory write-downs accelerating to $44.43 million in 2025 due to global stockpiling and domestic utilization rates plunging, Mindray is currently suffering the frictions of a heavy-metal manufacturer. The Street is over-indexing on the "AI software" narrative; the actual 2026 margin defense will rely entirely on Mindray's ability to seamlessly distribute physical "flow-based" surgical and diagnostic consumables through its newly acquired global infrastructure.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*

Figure Mindray Global Investment Profile: The Strategic Pivot to a Device + IT + AI Ecosystem

Segmental Incremental Margins and Internal Capital AllocationOperating under the ticker SZSE: 300760, Mindray's 2025 financials expose a distinct bifurcation: traditional heavy-metal capital expenditures are eroding under policy pressure, while integrated consumables and M&A-driven emerging lines represent the definitive growth vector. Despite top-line contraction, the company's capital structure remains highly unleveraged, providing a fortress balance sheet for sustained global acquisitions.

* Top-Line & Profitability Variance: Total 2025 revenue contracted 9.4% YoY to $4,630.56 million (CNY 33,282.2 million), dragging net profit down 28.0% YoY to $1,175.86 million. Gross margins compressed longitudinally from 64.2% (2023) to 60.3% (2025), largely driven by domestic VBP pricing re-baselines.

* Operating Leverage & Cash Conversion: Earnings quality remains impeccable. The 2025 Operating Cash Flow (OCF) stood at $1,411.47 million against net profits of $1,175.86 million—a conversion ratio of 1.20x. High cash generation is insulated by an ultra-conservative gearing ratio of 27.4%, with near-zero long-term interest-bearing bank debt ($0.67 million) and $2,452.16 million in cash reserves.

* Segmental Inventory & Unit Economics:

* *In-Vitro Diagnostics (IVD):* $1,703.05 million (36.8% of Rev). Gross margins compressed to 58.3%. Production: 59.7K equipment units and 27.49 million reagent units. Strategy hinges on high-frequency reagent consumption offsetting hardware ASP declines.

* *Patient Monitoring and Life Support (PMLS):* $1,368.59 million (29.6% of Rev). Down 19.8% YoY; 584.0K units produced. Margin dropped to 59.4%. Hurt by delayed replacement cycles and tightened public hospital budgets.

* *Medical Imaging Systems:* $795.37 million (17.2% of Rev). Down 18.0% YoY; 44.0K units produced. Squeezed by domestic anti-corruption scrutiny on large tenders, partially offset by overseas Resona A20 traction.

* *Emerging Business (MIS, MII, Animal Care):* The sole hyper-growth pillar, generating $748.24 million (+38.8% YoY). Margins expanded to 63.7%, bolstered by the $1.06 billion integration of Huitai Medical (which independently generated $359.5 million in 2025 revenue).

* R&D-to-Moat Translation: R&D expenditure structurally increased to $546.63 million (11.8% of revenue) in 2025. The portfolio commands 12,983 patent applications (72.39% invention-based).

Supply Chain Physicality and Post-2026 Trade Resilience

Mindray’s physical footprint is systematically detaching from single-market reliance. International revenues now command 53.0% of the total ($2,455.7 million), with Emerging Markets acting as the anchor (34.8% of total revenue).

* Domestic Manufacturing & Dark Factories: Mindray is transitioning its core production bases in Shenzhen, Nanjing, Dangshan, and Wuhan into fully automated, IIoT-driven "dark factories." However, proactive global expansion has temporarily suppressed capacity utilization (e.g., PMLS dropped to 55.4% in 2025, IVD equipment to 64.9%).

* Geopolitical Hedging & Localization: To circumvent the EU’s International Procurement Instrument (IPI)—which restricts Chinese entities from public bids over $5.65 million (EUR 5 million)—and the US 30% retaliatory tariff truce (expiring Nov 2026), Mindray has established local production projects across 14 countries.

* Supply Chain Autonomy: Supplier concentration is statistically negligible. The top five suppliers account for just 6.0% ($111.15 million) of procurement. Crucially, direct dependency on US-imported raw materials is capped below 5%, neutralizing immediate "chokehold" sanctions risk. The acquisitions of HyTest (Finland) and DiaSys (Germany) further internalized critical upstream IVD antigens and overseas logistics.

HDIN Institutional Perspective

While Mindray's prospectus heavily markets its "Device + IT + AI" ecosystem and the "Qi Yuan" LLMs as high-switching-cost SaaS equivalents, forensic financial data suggests a divergent reality. The 119.1% surge in goodwill to $1,543.41 million—primarily from the Huitai Medical acquisition—indicates that future growth is increasingly purchased through capital-intensive M&A rather than organically engineered software adoption. Furthermore, with inventory write-downs accelerating to $44.43 million in 2025 due to global stockpiling and domestic utilization rates plunging, Mindray is currently suffering the frictions of a heavy-metal manufacturer. The Street is over-indexing on the "AI software" narrative; the actual 2026 margin defense will rely entirely on Mindray's ability to seamlessly distribute physical "flow-based" surgical and diagnostic consumables through its newly acquired global infrastructure.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards.*