High-Throughput Sequencing 2026 Outlook: Why Illumina, MGI Tech, and Pacific Biosciences Diverge on Capital Allocation Amid China Decoupling

Date : 2026-05-18

Reading : 351

The 2025 high-throughput sequencing sector reveals a brutal bifurcation: mature diagnostic giants are harvesting cash while pre-profit innovators face acute capital starvation. Illumina's $65 million revenue evaporation following its addition to China's "Unreliable Entities" list forced a massive geographic market share transfer to MGI Tech. For institutional LPs, the critical metric is no longer raw gigabase throughput, but defensive unit economics. As Pacific Biosciences completely abandons short-reads via a $50 million asset sale to Illumina, the clinical market is aggressively pivoting toward AI-driven bioinformatics lock-ins and decentralized, room-temperature regulatory approvals.

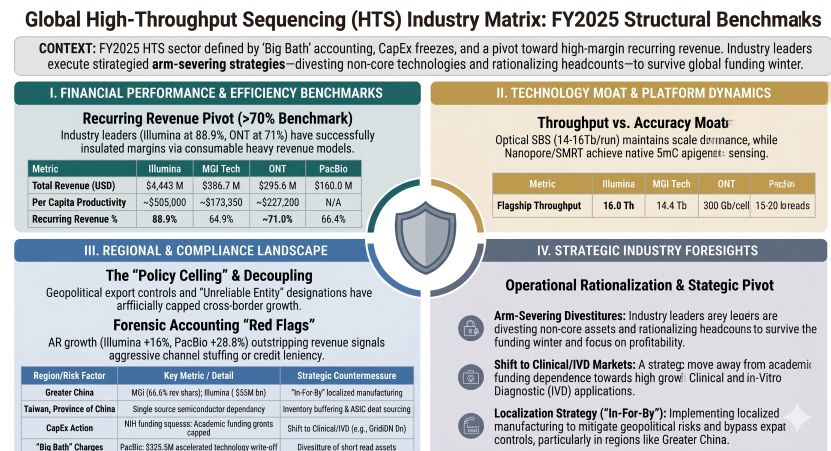

Figure Global High-Throughput Sequencing (HTS) Industry Matrix: FY2025 Structural Benchmarks

Forensic Financials & Margin Quality: The Divergence of Operating Leverage

Based on a Forensic Analysis of the 2025 annual reports, the industry is executing a defensive shift away from aggressive capital expenditure (CapEx) toward asset-light margin preservation. The "Razor and Blade" unit economics are undergoing severe stress tests as macroeconomic headwinds constrain hospital equipment budgets.

* Illumina (NASDAQ: ILMN): Generated $4.34 billion in total revenue (-1% YoY), but engineered an impressive Operating Cash Flow (OCF) of $1.08 billion against a net income of $850 million. The core moat is its 88.9% recurring revenue stream (consumables + services). However, this earnings quality was heavily padded by a $328 million non-operating gain from GRAIL investments.

* Pacific Biosciences (NASDAQ: PACB): Demonstrates severe structural balance sheet distress. The firm reported a net loss of -$546.4 million with an OCF burn of -$111.2 million. Carrying a lethal Debt-to-Equity ratio of ~121x ($645.4 million in convertible notes vs. $5.3 million equity), the company drastically slashed CapEx to $2.7 million and executed a $359.3 million accelerated amortization charge to entirely write off its Omniome short-read technology.

* Oxford Nanopore Technologies (LSE: ONT): Achieved a highly resilient 22.2% top-line growth to $295.37 million (£223.9 million), driven by clinical applied markets (+59.9%). Operating with a current ratio of 5.56x and $399.5 million in liquidity, ONT is fully capitalized to hit its 2027 EBITDA break-even target, primarily supported by a 25% surge in PromethION flow cell utilization.

* Axbio (Pre-IPO): Operating in a critical net liability position (deficit of $80.1 million) with a 0.3x current ratio. With $24.6 million in cash and a ~$14.3 million burn rate, Axbio’s ~1.5-year runway hinges entirely on its planned IPO to convert $104.7 million in preferred shares into equity before its AXP-100 system hits clinical trials in Q3 2026.

* MGI Tech (SHA: 688114): Showcases bizarre but highly effective cash conversion. Despite a net loss of -$29.6 million, strict inventory control and $12.2 million in combined state subsidies and asset disposals generated a positive OCF of $30.5 million. MGI's miniaturized E25 platform saw consumable revenue explode by 459.7% YoY.

Supply Chain Audit & Geo-Economic Moat: Patent Thickets and Regional Monopolies

The physical footprint of sequencing hardware is fracturing along geopolitical fault lines. To bypass Western litigation and trade restrictions, supply chains and intellectual property are being heavily decentralized.

* The Out-Licensing Pivot: Following aggressive global patent injunctions initiated by NASDAQ: ILMN, MGI Tech faced structural exclusion in Germany, the UK, and France. To circumvent these commercial blockades, MGI offloaded 100% of its US subsidiary, Complete Genomics, to Swiss Rockets AG in March 2026. This allows MGI to collect royalty streams without bearing direct Western commercialization risks, while concurrently capturing ~70% of China's public tender market.

* Solid-State Decentralization: Hardware physicality is shifting away from bulky optical architecture. LSE: ONT launched the MinION Mk1D, specifically engineered for thermal stability between 10°C and 35°C, effectively removing traditional HVAC lab infrastructure dependencies for edge-computing genomic surveillance. Similarly, NASDAQ: ILMN eliminated cold-chain logistics requirements for Sequencing by Synthesis (SBS) with its MiSeq i100 ambient-temperature reagents.

* Semiconductor Dependencies: Pre-commercial disruptor Axbio's primary supply chain vulnerability rests on its 300mm wafer, 65nm Bio-CMOS fabrication process. The 6.85 kg AXP-100 relies on microfluidic AC impedance detection, bypassing optical lenses entirely to achieve real-time infectious disease sequencing at the point of care.

HDIN Institutional Perspective: The Channel Stuffing Mirage

While management commentary across the sector champions recurring revenue resilience, our audit of working capital ratios reveals a classic "red flag" divergence indicating aggressive premature revenue recognition and potential distributor channel stuffing.

Illumina reported a 1% decline in 2025 consolidated revenue, yet Gross Accounts Receivable (AR) spiked 16% from $735 million to $854 million, matched by climbing inventory levels. This AR divergence against flat sales strongly suggests lenient credit extensions to pull forward demand.

More alarming is Pacific Biosciences. The firm registered a modest 4% top-line growth, but AR surged 28.8% to $35.4 million. Crucially, PacBio utilizes a highly aggressive FOB Shipping Point revenue recognition policy for its non-end-user distributors. Booking revenue the moment a Revio system leaves the warehouse—coupled with an $18.7 million non-operating contingent gain tied to legally voiding milestone payments on a failed product pipeline—artificially masks the true degradation of end-market CapEx demand. The Street has not fully priced in the working capital risk embedded in these receivables.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Global High-Throughput Sequencing (HTS) Industry Matrix: FY2025 Structural Benchmarks

Forensic Financials & Margin Quality: The Divergence of Operating Leverage

Based on a Forensic Analysis of the 2025 annual reports, the industry is executing a defensive shift away from aggressive capital expenditure (CapEx) toward asset-light margin preservation. The "Razor and Blade" unit economics are undergoing severe stress tests as macroeconomic headwinds constrain hospital equipment budgets.

* Illumina (NASDAQ: ILMN): Generated $4.34 billion in total revenue (-1% YoY), but engineered an impressive Operating Cash Flow (OCF) of $1.08 billion against a net income of $850 million. The core moat is its 88.9% recurring revenue stream (consumables + services). However, this earnings quality was heavily padded by a $328 million non-operating gain from GRAIL investments.

* Pacific Biosciences (NASDAQ: PACB): Demonstrates severe structural balance sheet distress. The firm reported a net loss of -$546.4 million with an OCF burn of -$111.2 million. Carrying a lethal Debt-to-Equity ratio of ~121x ($645.4 million in convertible notes vs. $5.3 million equity), the company drastically slashed CapEx to $2.7 million and executed a $359.3 million accelerated amortization charge to entirely write off its Omniome short-read technology.

* Oxford Nanopore Technologies (LSE: ONT): Achieved a highly resilient 22.2% top-line growth to $295.37 million (£223.9 million), driven by clinical applied markets (+59.9%). Operating with a current ratio of 5.56x and $399.5 million in liquidity, ONT is fully capitalized to hit its 2027 EBITDA break-even target, primarily supported by a 25% surge in PromethION flow cell utilization.

* Axbio (Pre-IPO): Operating in a critical net liability position (deficit of $80.1 million) with a 0.3x current ratio. With $24.6 million in cash and a ~$14.3 million burn rate, Axbio’s ~1.5-year runway hinges entirely on its planned IPO to convert $104.7 million in preferred shares into equity before its AXP-100 system hits clinical trials in Q3 2026.

* MGI Tech (SHA: 688114): Showcases bizarre but highly effective cash conversion. Despite a net loss of -$29.6 million, strict inventory control and $12.2 million in combined state subsidies and asset disposals generated a positive OCF of $30.5 million. MGI's miniaturized E25 platform saw consumable revenue explode by 459.7% YoY.

Supply Chain Audit & Geo-Economic Moat: Patent Thickets and Regional Monopolies

The physical footprint of sequencing hardware is fracturing along geopolitical fault lines. To bypass Western litigation and trade restrictions, supply chains and intellectual property are being heavily decentralized.

* The Out-Licensing Pivot: Following aggressive global patent injunctions initiated by NASDAQ: ILMN, MGI Tech faced structural exclusion in Germany, the UK, and France. To circumvent these commercial blockades, MGI offloaded 100% of its US subsidiary, Complete Genomics, to Swiss Rockets AG in March 2026. This allows MGI to collect royalty streams without bearing direct Western commercialization risks, while concurrently capturing ~70% of China's public tender market.

* Solid-State Decentralization: Hardware physicality is shifting away from bulky optical architecture. LSE: ONT launched the MinION Mk1D, specifically engineered for thermal stability between 10°C and 35°C, effectively removing traditional HVAC lab infrastructure dependencies for edge-computing genomic surveillance. Similarly, NASDAQ: ILMN eliminated cold-chain logistics requirements for Sequencing by Synthesis (SBS) with its MiSeq i100 ambient-temperature reagents.

* Semiconductor Dependencies: Pre-commercial disruptor Axbio's primary supply chain vulnerability rests on its 300mm wafer, 65nm Bio-CMOS fabrication process. The 6.85 kg AXP-100 relies on microfluidic AC impedance detection, bypassing optical lenses entirely to achieve real-time infectious disease sequencing at the point of care.

HDIN Institutional Perspective: The Channel Stuffing Mirage

While management commentary across the sector champions recurring revenue resilience, our audit of working capital ratios reveals a classic "red flag" divergence indicating aggressive premature revenue recognition and potential distributor channel stuffing.

Illumina reported a 1% decline in 2025 consolidated revenue, yet Gross Accounts Receivable (AR) spiked 16% from $735 million to $854 million, matched by climbing inventory levels. This AR divergence against flat sales strongly suggests lenient credit extensions to pull forward demand.

More alarming is Pacific Biosciences. The firm registered a modest 4% top-line growth, but AR surged 28.8% to $35.4 million. Crucially, PacBio utilizes a highly aggressive FOB Shipping Point revenue recognition policy for its non-end-user distributors. Booking revenue the moment a Revio system leaves the warehouse—coupled with an $18.7 million non-operating contingent gain tied to legally voiding milestone payments on a failed product pipeline—artificially masks the true degradation of end-market CapEx demand. The Street has not fully priced in the working capital risk embedded in these receivables.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."