Luxury Outerwear 2026 Outlook: Why Canada Goose and Moncler Diverge on Capital Structure and Climate Resilience Amid Greater China Volatility

Date : 2026-05-18

Reading : 239

The structural divergence between Canada Goose and Moncler exposes a stark reality for institutional LPs. As erratic weather patterns disrupt historical Q3/Q4 peak demand, Moncler shields operating margins via a USD 1,648.4 million net cash fortress and aggressive experiential retail expansion. Conversely, Canada Goose relies on 1.3x leveraged linear manufacturing to fund off-season working capital. With both entities extracting outsized revenues from Greater China, regional macroeconomic tightening and tariff volatility introduce asymmetric downside risks that traditional equity valuations have not fully priced in.

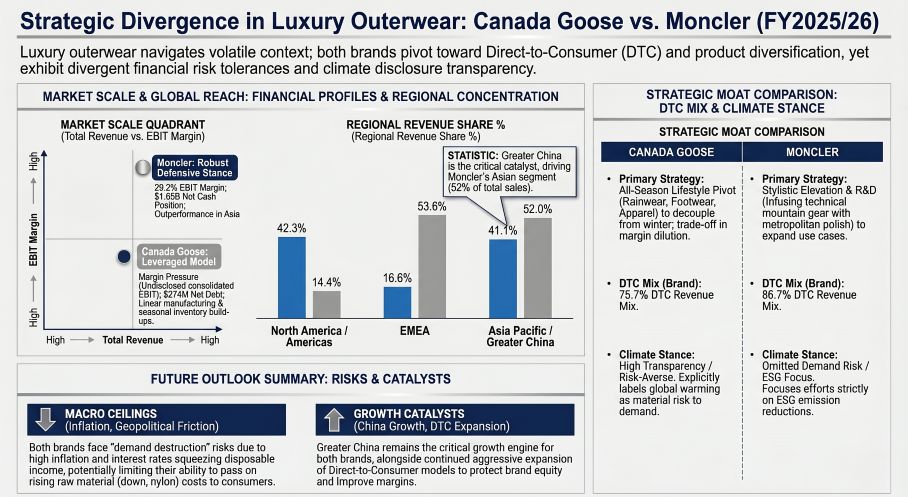

Figure Strategic Divergence in Luxury Outerwear: Canada Goose vs Moncler

Forensic Analysis: Segmental Profitability and Margin Divergence

Forensic Analysis: Segmental Profitability and Margin Divergence

A forensic financial extraction of fiscal 2025/2026 data indicates that both NYSE: GOOS and MIL: MONC are aggressively transitioning toward Direct-to-Consumer (DTC) architectures, though their capital efficiencies and unit economics starkly contrast.

* Canada Goose (FY 2026): Total revenue reached USD 1,093.7 million (CAD 1,528.2 million), with DTC generating a dominant 75.7% (USD 828.3 million) and Wholesale compressing to 19.1%. Operating with 74 permanent retail locations, unit economics reflect an average revenue per store of USD 7.27 million and USD 2,926 per square foot. Human capital productivity sits at approximately USD 244,800 per employee (headcount: 3,942).

* Moncler Group (FY 2025): Consolidated revenues hit USD 3,541.2 million (EUR 3,132.1 million). The flagship Moncler brand (USD 3,076.2 million) is highly DTC-leveraged at 86.7%, while the Stone Island portfolio (USD 464.9 million) retains a heavy European wholesale footprint (44.9%). The Group delivered a robust 29.2% EBIT margin (USD 1,032.69 million).

Segmental Inventory & Capital Matrix

* *Net Leverage vs. Fortress Balance Sheets:* Moncler operates with a USD 1,648.4 million net financial cash position. Conversely, Canada Goose carries USD 274.2 million in net debt (1.3x Adjusted EBITDA) heavily structured around a USD 298.3 million Term Loan anchored at a 7.16% interest rate, exposing the firm to elevated servicing costs in a higher-for-longer rate environment.

* *Regional Dependency:* Moncler derives 52.0% (USD 1,600.9 million) of flagship brand revenue from Asia. Canada Goose extracts 32.6% (USD 356.6 million) of its global revenue exclusively from Greater China, operating 32 of its 88 global stores within this single geopolitical theater.

* *Actuarial Liabilities:* Canada Goose carries a USD 20.75 million compounding warranty provision on its balance sheet for its "Lifetime Warranty" promise. During FY 2025, it recognized USD 4.44 million in new provisions and utilized USD 5.37 million for physical repair and replacement claims. Moncler omits disclosure of forward warranty liabilities.

Supply Chain Audit: Physicality, Sourcing Vulnerabilities, and Geo-Economic Moats

The physicality of the luxury outerwear supply chain reveals acute structural bottlenecks and raw material volatility, directly challenging the industry's pricing elasticity.

Manufacturing Linearization and Liquidity Bridging

To combat extreme seasonal demand concentration, Canada Goose utilizes a linear manufacturing model across its internal Canadian facilities and European contract manufacturers. This continuous production stages heavy inventory (reaching USD 274.8 million, or a ~3.5x Sales-to-Inventory ratio) during the off-season. To finance this working capital build-up, the company draws on specialized localized credit facilities, including a CAD 517.5 million revolving facility capacity optimized specifically for the June 1 through November 30 peak production window, alongside a JPY 4,000.0 million facility in Japan.

Raw Material Sourcing and Compliance Hurdles

Canada Goose's COGS are highly exposed to inflation in down, nylon, and polyester. The brand manages compliance via the Responsible Down Standard (RDS, certified in 2022) and strict adherence to *Canada’s Fighting Against Forced Labour and Child Labour in Supply Chains Act*. Conversely, Moncler's supply chain disclosures prioritize Scope 3 decarbonization and material circularity, achieving targets of sourcing over 60% of nylon from recycled materials and 55% of cotton from organic/recycled origins. Moncler’s Stone Island division actively funds material R&D, deploying proprietary "DENIM RESEARCH" capsules utilizing Polypropylene Denim and Micro Corduroy.

Brand Protection & Physical Authentication

Canada Goose recorded a USD 32.0 million legal settlement resulting from a commercial supplier dispute, highlighting the friction inherent in vendor termination. Furthermore, to combat counterfeiting, the brand avoids digital RFID/NFC tagging, relying instead on legacy holographic tags implemented in 2011 and distributor domain-verification tools. Moncler’s disclosures omit specific IP litigation budgets or digital traceability investments.

HDIN Institutional Perspective

While the Street continues to evaluate both Canada Goose and Moncler through the lens of traditional luxury multiples, the physical inventory metrics suggest a highly vulnerable, hardware-intensive burn rate for Canada Goose that equity markets have mispriced.

Canada Goose acknowledges that it may lose the ability to pass inflationary supply chain costs to consumers without destroying demand, indicating a structural cap on gross margin elasticity. Furthermore, Canada Goose's ongoing product pivot—shifting away from high-margin traditional down parkas toward lower-margin transitional rainwear and footwear to combat milder winters—will likely compress ROIC over the next 24 months. Meanwhile, Moncler's exclusion of lease liabilities from its "net financial position" masks the true operational leverage embedded within its aggressive expansion of 295 Moncler DOS and 95 Stone Island DOS locations. Ultimately, institutional investors must discount both entities for their hyper-concentration in the Greater China region, where shifting consumer sentiment and real estate headwinds pose an immediate threat to FY 2026 DTC conversion rates.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Strategic Divergence in Luxury Outerwear: Canada Goose vs Moncler

Forensic Analysis: Segmental Profitability and Margin DivergenceA forensic financial extraction of fiscal 2025/2026 data indicates that both NYSE: GOOS and MIL: MONC are aggressively transitioning toward Direct-to-Consumer (DTC) architectures, though their capital efficiencies and unit economics starkly contrast.

* Canada Goose (FY 2026): Total revenue reached USD 1,093.7 million (CAD 1,528.2 million), with DTC generating a dominant 75.7% (USD 828.3 million) and Wholesale compressing to 19.1%. Operating with 74 permanent retail locations, unit economics reflect an average revenue per store of USD 7.27 million and USD 2,926 per square foot. Human capital productivity sits at approximately USD 244,800 per employee (headcount: 3,942).

* Moncler Group (FY 2025): Consolidated revenues hit USD 3,541.2 million (EUR 3,132.1 million). The flagship Moncler brand (USD 3,076.2 million) is highly DTC-leveraged at 86.7%, while the Stone Island portfolio (USD 464.9 million) retains a heavy European wholesale footprint (44.9%). The Group delivered a robust 29.2% EBIT margin (USD 1,032.69 million).

Segmental Inventory & Capital Matrix

* *Net Leverage vs. Fortress Balance Sheets:* Moncler operates with a USD 1,648.4 million net financial cash position. Conversely, Canada Goose carries USD 274.2 million in net debt (1.3x Adjusted EBITDA) heavily structured around a USD 298.3 million Term Loan anchored at a 7.16% interest rate, exposing the firm to elevated servicing costs in a higher-for-longer rate environment.

* *Regional Dependency:* Moncler derives 52.0% (USD 1,600.9 million) of flagship brand revenue from Asia. Canada Goose extracts 32.6% (USD 356.6 million) of its global revenue exclusively from Greater China, operating 32 of its 88 global stores within this single geopolitical theater.

* *Actuarial Liabilities:* Canada Goose carries a USD 20.75 million compounding warranty provision on its balance sheet for its "Lifetime Warranty" promise. During FY 2025, it recognized USD 4.44 million in new provisions and utilized USD 5.37 million for physical repair and replacement claims. Moncler omits disclosure of forward warranty liabilities.

Supply Chain Audit: Physicality, Sourcing Vulnerabilities, and Geo-Economic Moats

The physicality of the luxury outerwear supply chain reveals acute structural bottlenecks and raw material volatility, directly challenging the industry's pricing elasticity.

Manufacturing Linearization and Liquidity Bridging

To combat extreme seasonal demand concentration, Canada Goose utilizes a linear manufacturing model across its internal Canadian facilities and European contract manufacturers. This continuous production stages heavy inventory (reaching USD 274.8 million, or a ~3.5x Sales-to-Inventory ratio) during the off-season. To finance this working capital build-up, the company draws on specialized localized credit facilities, including a CAD 517.5 million revolving facility capacity optimized specifically for the June 1 through November 30 peak production window, alongside a JPY 4,000.0 million facility in Japan.

Raw Material Sourcing and Compliance Hurdles

Canada Goose's COGS are highly exposed to inflation in down, nylon, and polyester. The brand manages compliance via the Responsible Down Standard (RDS, certified in 2022) and strict adherence to *Canada’s Fighting Against Forced Labour and Child Labour in Supply Chains Act*. Conversely, Moncler's supply chain disclosures prioritize Scope 3 decarbonization and material circularity, achieving targets of sourcing over 60% of nylon from recycled materials and 55% of cotton from organic/recycled origins. Moncler’s Stone Island division actively funds material R&D, deploying proprietary "DENIM RESEARCH" capsules utilizing Polypropylene Denim and Micro Corduroy.

Brand Protection & Physical Authentication

Canada Goose recorded a USD 32.0 million legal settlement resulting from a commercial supplier dispute, highlighting the friction inherent in vendor termination. Furthermore, to combat counterfeiting, the brand avoids digital RFID/NFC tagging, relying instead on legacy holographic tags implemented in 2011 and distributor domain-verification tools. Moncler’s disclosures omit specific IP litigation budgets or digital traceability investments.

HDIN Institutional Perspective

While the Street continues to evaluate both Canada Goose and Moncler through the lens of traditional luxury multiples, the physical inventory metrics suggest a highly vulnerable, hardware-intensive burn rate for Canada Goose that equity markets have mispriced.

Canada Goose acknowledges that it may lose the ability to pass inflationary supply chain costs to consumers without destroying demand, indicating a structural cap on gross margin elasticity. Furthermore, Canada Goose's ongoing product pivot—shifting away from high-margin traditional down parkas toward lower-margin transitional rainwear and footwear to combat milder winters—will likely compress ROIC over the next 24 months. Meanwhile, Moncler's exclusion of lease liabilities from its "net financial position" masks the true operational leverage embedded within its aggressive expansion of 295 Moncler DOS and 95 Stone Island DOS locations. Ultimately, institutional investors must discount both entities for their hyper-concentration in the Greater China region, where shifting consumer sentiment and real estate headwinds pose an immediate threat to FY 2026 DTC conversion rates.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant):*

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."