Xinhua Semiconductor Captures 60% Domestic Polysilicon Share; 2025 Revenue Surges 61.4%

Date : 2026-05-20

Reading : 102

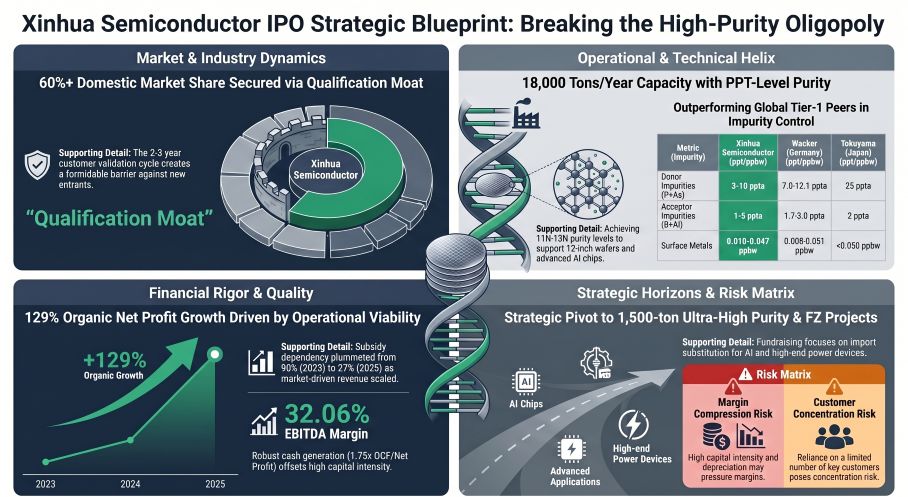

Breaking the decades-long supply chain oligopoly held by Wacker, Hemlock, and Tokuyama, Jiangsu Xinhua Semiconductor Technology Co., Ltd. has captured over 60% of China’s domestic integrated circuit electronic-grade polysilicon market as of 2025. Driven by the commissioning of its 10,000-ton Inner Mongolia facility, the firm recorded a 61.41% year-over-year revenue surge to $249.19 million, with organic net profit exploding by 129.0%. Our primary data confirms this 18,000-ton aggregate capacity effectively neutralizes critical raw material bottlenecks for domestic 12-inch advanced wafer fabs, fundamentally restructuring the geopolitical chokepoints for ultra-high purity semiconductor materials.

Figure Xinhua Semiconductor IPO Strategic Blueprint: Breaking the High-Purity Oligopoly

The 12-Inch Wafer Monopolistic Rupture

The 12-Inch Wafer Monopolistic Rupture

The structural foundation of Xinhua Semiconductor’s market dominance is predicated on exceptional customer switching costs and rigorous trace impurity control. Operating at the 11N to 13N purity threshold, the company restricts donor impurities (P+As) to 3-10 parts per trillion (ppta) and acceptor impurities (B+Al) to 1-5 ppta—metrics that strictly match or outperform German and Japanese tier-one benchmarks.

Because wafer manufacturers enforce a draconian 2-to-3-year qualification cycle encompassing sample testing, crystal pulling, and terminal fab validation, Xinhua has established a virtually impenetrable defensive moat. Supply agreements with top-tier clients, including TCL Zhonghuan, NSIG (Shanghai Silicon Industry Group), and Xi'an Simgui, locked in 71.49% of its 2025 revenue ($178.14 million). The primary headwind embedded in this model, however, is a deliberate 5.05% Average Selling Price (ASP) compression utilized to aggressively accelerate domestic import substitution, demanding hyper-efficient cost controls to maintain gross margins.

The Xuzhou-Inner Mongolia Dual-Base Strategy

Xinhua Semiconductor operates a highly strategic dual-base manufacturing footprint designed to balance R&D precision with massive economies of scale. The mature Xuzhou base (8,000 tons/year) functions as the technological epicenter for defect reduction and legacy capacity. Conversely, the newly commissioned Inner Mongolia base (10,000 tons/year) acts as the primary volume engine.

Procurement dynamics are strictly localized. By stripping away foreign reliance for critical inputs like silicon powder and trichlorosilane, the firm is structurally insulated from US export controls. However, the modified Siemens process remains intensely energy-dependent, with electricity and steam accounting for 56.75% of total procurement costs ($74.72 million) in 2025. The Inner Mongolia expansion leverages lower regional power tariffs, fundamentally reducing unit production costs while pushing overall capacity utilization to an effective 77.77%.

Forensic Margin Analysis & Operating Leverage Risk

A rigorous stripping of government subsidies reveals a highly viable, market-driven profitability cycle. While non-operational grants constituted over 90% of pre-tax profit in 2023, this dependency plummeted to 27.21% by 2025. Stripping out anomalies, core operational net profit hit $20.39 million, underscoring the raw earning power of its P-grade polysilicon volume.

Despite robust cash generation (OCF to Net Profit ratio of 1.75x), the balance sheet carries immense operating leverage risks. The capitalization of the Inner Mongolia plant triggered a massive depreciation wave, charging $55.14 million against profits in 2025 alone—a $1.35 million monthly drag on net earnings. Concurrently, the trial phases of this expansion generated high volumes of off-spec solar-grade by-products. Depressed photovoltaic market pricing forced a $15.37 million inventory impairment (21.50% of total inventory value).

Analyst Insight: The HDIN Viewpoint

While Xinhua Semiconductor’s capacity scale-up is a definitive geopolitical triumph for Chinese semiconductor autonomy, the firm is entering a precarious margin stress-test window. The strategic pivot toward ultra-high-resistance (J-grade) and Float-Zone (FZ) polysilicon—essential for AI chips and advanced IGBT power devices—is a necessary evolution to escape the commoditization of standard P-grade materials.

Proprietary supply-side modeling suggests that the looming fixed-cost burden leaves zero margin for error regarding downstream wafer demand contraction. The firm's ultimate viability hinges entirely on successfully executing its $576.16 million capital expenditure roadmap to transition from a pure-play polysilicon provider to a comprehensive "Silicon + High Purity" matrix (including silicon-based electronic specialty gases and 7N high-purity quartz sand) before peak-cycle depreciation erodes its operational cash flow.

Analyst Quote

"Xinhua Semiconductor has effectively commoditized what was once a highly weaponized geopolitical chokepoint," notes the Lead Semiconductor Materials Analyst at HDIN Research. "The immediate strategic implication is not merely domestic market capture, but the enforcement of a brutal capital expenditure barrier that locks out new domestic entrants, while simultaneously challenging the pricing power of global tier-one conglomerates in the 12-inch wafer supply chain."

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

Inquiries: sales@hdinresearch.com

AI Transparency Disclosure

*This market intelligence was curated by HDIN Research analysts with technical drafting assistance from AI. All data, logic, and strategic conclusions have been audited and verified by our human editorial board to ensure professional-grade accuracy.*

Figure Xinhua Semiconductor IPO Strategic Blueprint: Breaking the High-Purity Oligopoly

The 12-Inch Wafer Monopolistic RuptureThe structural foundation of Xinhua Semiconductor’s market dominance is predicated on exceptional customer switching costs and rigorous trace impurity control. Operating at the 11N to 13N purity threshold, the company restricts donor impurities (P+As) to 3-10 parts per trillion (ppta) and acceptor impurities (B+Al) to 1-5 ppta—metrics that strictly match or outperform German and Japanese tier-one benchmarks.

Because wafer manufacturers enforce a draconian 2-to-3-year qualification cycle encompassing sample testing, crystal pulling, and terminal fab validation, Xinhua has established a virtually impenetrable defensive moat. Supply agreements with top-tier clients, including TCL Zhonghuan, NSIG (Shanghai Silicon Industry Group), and Xi'an Simgui, locked in 71.49% of its 2025 revenue ($178.14 million). The primary headwind embedded in this model, however, is a deliberate 5.05% Average Selling Price (ASP) compression utilized to aggressively accelerate domestic import substitution, demanding hyper-efficient cost controls to maintain gross margins.

The Xuzhou-Inner Mongolia Dual-Base Strategy

Xinhua Semiconductor operates a highly strategic dual-base manufacturing footprint designed to balance R&D precision with massive economies of scale. The mature Xuzhou base (8,000 tons/year) functions as the technological epicenter for defect reduction and legacy capacity. Conversely, the newly commissioned Inner Mongolia base (10,000 tons/year) acts as the primary volume engine.

Procurement dynamics are strictly localized. By stripping away foreign reliance for critical inputs like silicon powder and trichlorosilane, the firm is structurally insulated from US export controls. However, the modified Siemens process remains intensely energy-dependent, with electricity and steam accounting for 56.75% of total procurement costs ($74.72 million) in 2025. The Inner Mongolia expansion leverages lower regional power tariffs, fundamentally reducing unit production costs while pushing overall capacity utilization to an effective 77.77%.

Forensic Margin Analysis & Operating Leverage Risk

A rigorous stripping of government subsidies reveals a highly viable, market-driven profitability cycle. While non-operational grants constituted over 90% of pre-tax profit in 2023, this dependency plummeted to 27.21% by 2025. Stripping out anomalies, core operational net profit hit $20.39 million, underscoring the raw earning power of its P-grade polysilicon volume.

Despite robust cash generation (OCF to Net Profit ratio of 1.75x), the balance sheet carries immense operating leverage risks. The capitalization of the Inner Mongolia plant triggered a massive depreciation wave, charging $55.14 million against profits in 2025 alone—a $1.35 million monthly drag on net earnings. Concurrently, the trial phases of this expansion generated high volumes of off-spec solar-grade by-products. Depressed photovoltaic market pricing forced a $15.37 million inventory impairment (21.50% of total inventory value).

Analyst Insight: The HDIN Viewpoint

While Xinhua Semiconductor’s capacity scale-up is a definitive geopolitical triumph for Chinese semiconductor autonomy, the firm is entering a precarious margin stress-test window. The strategic pivot toward ultra-high-resistance (J-grade) and Float-Zone (FZ) polysilicon—essential for AI chips and advanced IGBT power devices—is a necessary evolution to escape the commoditization of standard P-grade materials.

Proprietary supply-side modeling suggests that the looming fixed-cost burden leaves zero margin for error regarding downstream wafer demand contraction. The firm's ultimate viability hinges entirely on successfully executing its $576.16 million capital expenditure roadmap to transition from a pure-play polysilicon provider to a comprehensive "Silicon + High Purity" matrix (including silicon-based electronic specialty gases and 7N high-purity quartz sand) before peak-cycle depreciation erodes its operational cash flow.

Analyst Quote

"Xinhua Semiconductor has effectively commoditized what was once a highly weaponized geopolitical chokepoint," notes the Lead Semiconductor Materials Analyst at HDIN Research. "The immediate strategic implication is not merely domestic market capture, but the enforcement of a brutal capital expenditure barrier that locks out new domestic entrants, while simultaneously challenging the pricing power of global tier-one conglomerates in the 12-inch wafer supply chain."

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

Website: www.hdinresearch.com

Inquiries: sales@hdinresearch.com

AI Transparency Disclosure

*This market intelligence was curated by HDIN Research analysts with technical drafting assistance from AI. All data, logic, and strategic conclusions have been audited and verified by our human editorial board to ensure professional-grade accuracy.*