Suzhou Watech’s $386M IPO: How 3000W RF LDMOS & RugSiC Architectures Disrupt Tier-1 Monopolies

Date : 2026-05-20

Reading : 87

Suzhou Watech Electronics Co., Ltd. (Huatai) is fundamentally re-architecting the high-power semiconductor supply chain with its pending $386.87 million STAR Market IPO. Executing a highly calibrated "Virtual IDM + In-House Packaging" strategy out of its Suzhou headquarters, the firm has effectively dismantled Tier-1 foreign monopolies in the 5G telecom and plasma etching equipment sectors. With 2025 main business revenues hitting $95.60 million—driven by a 90.74% concentration in its Radio Frequency (RF) segment—Watech's capitalization targets the accelerated commercialization of its proprietary 3000W RF LDMOS and gate-oxide-free RugSiC platforms to insulate critical domestic infrastructure from escalating geopolitical export controls.

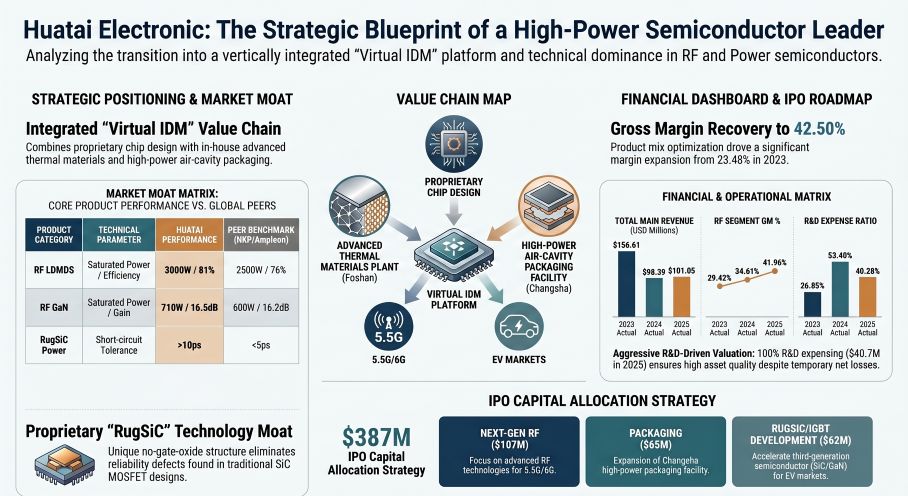

Figure Huatai Electronic: The Strategic Blueprint of a High-Power Semiconductor Leader

Virtual IDM and Sub-Segment Dominance

Virtual IDM and Sub-Segment Dominance

Proprietary supply-side modeling suggests that Watech’s competitive moat is not solely derived from circuit design, but from a vertically integrated physical ecosystem that bypasses standard foundry bottlenecks.

In the ultra-high-power RF power supply segment for semiconductor manufacturing equipment (e.g., plasma etching, ion implantation), Watech remains the sole domestic enterprise capable of mass-producing RF LDMOS products exceeding 3000W. Operating at a breakthrough 110V breakdown voltage with 81% efficiency, this silicon-based architecture significantly outpaces competing 2500W products from global incumbents like Ampleon.

Simultaneously, the company's Power Business is deploying its proprietary "RugSiC" architecture. By engineering a P-Gate structure devoid of traditional gate-oxide, Watech physically eradicates the reliability flaws and threshold voltage drifts inherent in conventional SiC MOSFETs dominated by Infineon and STMicroelectronics. Delivering a short-circuit tolerance time exceeding 10µs and an ultra-low feedback capacitance of 0.1pF, the RugSiC platform achieves megahertz-level high-frequency switching capabilities essential for AI server power supplies and EV onboard chargers.

CapEx Allocation and Asset Utilization

A highly bifurcated capacity utilization profile across Watech's regional manufacturing nodes, reflecting the realities of its Virtual IDM transition.

To mitigate thermal bottlenecks in 3000W+ chips, Watech internalized its advanced packaging ecosystem. At its Foshan Huazhi subsidiary, the production of multi-layer copper/molybdenum and diamond-copper composite thermal materials is operating at extreme overcapacity (111.73% utilization in 2025). Conversely, its Changsha Yaohua base—tasked with industrializing proprietary Air-Cavity Packaging using nano-sintered silver—is running at a low 55.03% utilization rate. This capacity overhang highlights significant room for external OSAT (Outsourced Semiconductor Assembly and Test) service expansion, directly challenging traditional, capital-heavy ceramic packaging supply chains.

To hedge against US and Japanese export controls targeting front-end semiconductor manufacturing equipment (SME), Watech routes 100% of its mass-market wafer fabrication to domestic foundries such as Huahong Semiconductor. However, specialized R&D lines for third-generation SiC processors remain moderately exposed to foreign capital equipment constraints, evidenced by procurement liabilities with Japanese vendors like NISSIN ION EQUIPMENT.

Supply Chain Concentration and Incumbent IP Friction

Despite robust technology parameters, Watech’s operational framework carries severe demand-side vulnerabilities. The oligopolistic nature of telecom infrastructure has forced an extreme revenue dependency on "Customer A," which accounted for 71.42% of 2025 top-line earnings. Any capex contraction by this single global telecom equipment giant presents an immediate liquidity risk, exacerbated by a bloated inventory cycle where Days Inventory Outstanding (DIO) stretched to approximately 223 days in 2025.

Furthermore, aggressive recruitment of top-tier talent from international competitors has triggered high-stakes IP litigation. The company is actively defending against patent invalidation appeals and a $1.11 million trade secret misappropriation lawsuit initiated by Ampleon. While early administrative and civil rulings favor Watech, this legal friction represents a calculated incumbent strategy to stall the firm's STAR Market entry.

Analyst Insight: The HDIN Viewpoint

The most misunderstood metric in Watech’s 2025 financial profile is the deeply negative gross margin (-57.66% in 2024, recovering marginally in 2025) of its nascent Power Business. Traditional equity pricing models might penalize the firm for its accumulated unrecovered deficit of $103.98 million, yet HDIN Research views this as a deliberate byproduct of strategic financial engineering.

Watech enforces a 100% R&D expensing policy—deploying $135.31 million over three years—refusing to capitalize development costs. Coupled with aggressive early-stage pricing to capture market share and heavily front-loaded depreciation on idle SiC equipment ($21.79 million impairment recognized), the GAAP losses mask the underlying asset quality. The firm is absorbing the upfront capital pain of building a localized Virtual IDM ecosystem. Once capacity utilization at the Changsha packaging base normalizes and the RugSiC platform secures Tier-1 automotive validation, the operational leverage will trigger exponential margin expansion, rendering current P/E multiples obsolete.

Analyst Quote

"Watech’s aggressive capitalization strategy is a textbook defense mechanism against global supply chain bifurcation. By bypassing standard foundry PDKs and integrating diamond-copper thermal materials in-house, they are not merely substituting imports; they are fundamentally rewriting the physical limits of high-power RF density. The ongoing IP litigation with global incumbents is less of an operational threat and more of a validation of Watech's disruptive market entry."

— Lead Semiconductor Strategist, HDIN Research

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

website: www.hdinresearch.com

Inquiries: sales@hdinresearch.com

AI Transparency Disclosure: This market intelligence was curated by HDIN Research analysts with technical drafting assistance from AI. All data, logic, and strategic conclusions have been audited and verified by our human editorial board to ensure professional-grade accuracy.

Figure Huatai Electronic: The Strategic Blueprint of a High-Power Semiconductor Leader

Virtual IDM and Sub-Segment DominanceProprietary supply-side modeling suggests that Watech’s competitive moat is not solely derived from circuit design, but from a vertically integrated physical ecosystem that bypasses standard foundry bottlenecks.

In the ultra-high-power RF power supply segment for semiconductor manufacturing equipment (e.g., plasma etching, ion implantation), Watech remains the sole domestic enterprise capable of mass-producing RF LDMOS products exceeding 3000W. Operating at a breakthrough 110V breakdown voltage with 81% efficiency, this silicon-based architecture significantly outpaces competing 2500W products from global incumbents like Ampleon.

Simultaneously, the company's Power Business is deploying its proprietary "RugSiC" architecture. By engineering a P-Gate structure devoid of traditional gate-oxide, Watech physically eradicates the reliability flaws and threshold voltage drifts inherent in conventional SiC MOSFETs dominated by Infineon and STMicroelectronics. Delivering a short-circuit tolerance time exceeding 10µs and an ultra-low feedback capacitance of 0.1pF, the RugSiC platform achieves megahertz-level high-frequency switching capabilities essential for AI server power supplies and EV onboard chargers.

CapEx Allocation and Asset Utilization

A highly bifurcated capacity utilization profile across Watech's regional manufacturing nodes, reflecting the realities of its Virtual IDM transition.

To mitigate thermal bottlenecks in 3000W+ chips, Watech internalized its advanced packaging ecosystem. At its Foshan Huazhi subsidiary, the production of multi-layer copper/molybdenum and diamond-copper composite thermal materials is operating at extreme overcapacity (111.73% utilization in 2025). Conversely, its Changsha Yaohua base—tasked with industrializing proprietary Air-Cavity Packaging using nano-sintered silver—is running at a low 55.03% utilization rate. This capacity overhang highlights significant room for external OSAT (Outsourced Semiconductor Assembly and Test) service expansion, directly challenging traditional, capital-heavy ceramic packaging supply chains.

To hedge against US and Japanese export controls targeting front-end semiconductor manufacturing equipment (SME), Watech routes 100% of its mass-market wafer fabrication to domestic foundries such as Huahong Semiconductor. However, specialized R&D lines for third-generation SiC processors remain moderately exposed to foreign capital equipment constraints, evidenced by procurement liabilities with Japanese vendors like NISSIN ION EQUIPMENT.

Supply Chain Concentration and Incumbent IP Friction

Despite robust technology parameters, Watech’s operational framework carries severe demand-side vulnerabilities. The oligopolistic nature of telecom infrastructure has forced an extreme revenue dependency on "Customer A," which accounted for 71.42% of 2025 top-line earnings. Any capex contraction by this single global telecom equipment giant presents an immediate liquidity risk, exacerbated by a bloated inventory cycle where Days Inventory Outstanding (DIO) stretched to approximately 223 days in 2025.

Furthermore, aggressive recruitment of top-tier talent from international competitors has triggered high-stakes IP litigation. The company is actively defending against patent invalidation appeals and a $1.11 million trade secret misappropriation lawsuit initiated by Ampleon. While early administrative and civil rulings favor Watech, this legal friction represents a calculated incumbent strategy to stall the firm's STAR Market entry.

Analyst Insight: The HDIN Viewpoint

The most misunderstood metric in Watech’s 2025 financial profile is the deeply negative gross margin (-57.66% in 2024, recovering marginally in 2025) of its nascent Power Business. Traditional equity pricing models might penalize the firm for its accumulated unrecovered deficit of $103.98 million, yet HDIN Research views this as a deliberate byproduct of strategic financial engineering.

Watech enforces a 100% R&D expensing policy—deploying $135.31 million over three years—refusing to capitalize development costs. Coupled with aggressive early-stage pricing to capture market share and heavily front-loaded depreciation on idle SiC equipment ($21.79 million impairment recognized), the GAAP losses mask the underlying asset quality. The firm is absorbing the upfront capital pain of building a localized Virtual IDM ecosystem. Once capacity utilization at the Changsha packaging base normalizes and the RugSiC platform secures Tier-1 automotive validation, the operational leverage will trigger exponential margin expansion, rendering current P/E multiples obsolete.

Analyst Quote

"Watech’s aggressive capitalization strategy is a textbook defense mechanism against global supply chain bifurcation. By bypassing standard foundry PDKs and integrating diamond-copper thermal materials in-house, they are not merely substituting imports; they are fundamentally rewriting the physical limits of high-power RF density. The ongoing IP litigation with global incumbents is less of an operational threat and more of a validation of Watech's disruptive market entry."

— Lead Semiconductor Strategist, HDIN Research

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research

HDIN Research focuses on providing market consulting services. As an independent third-party consulting firm, it is committed to providing in-depth market research and analysis reports.

website: www.hdinresearch.com

Inquiries: sales@hdinresearch.com

AI Transparency Disclosure: This market intelligence was curated by HDIN Research analysts with technical drafting assistance from AI. All data, logic, and strategic conclusions have been audited and verified by our human editorial board to ensure professional-grade accuracy.