Global Subsea Defense & Robotics 2026 Outlook: Why General Dynamics, Saab, and Nauticus Robotics Diverge on Capital Allocation Amid Transatlantic Procurement Shifts

Date : 2026-05-19

Reading : 192

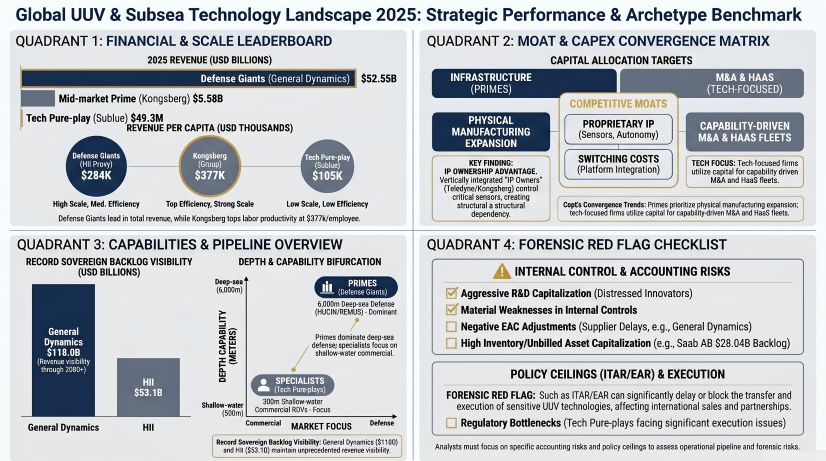

The 2025 financial disclosures reveal a structural paradox in the subsea defense sector: order pipelines are overflowing while margin conversion stalls. Sovereign primes like General Dynamics and Huntington Ingalls Industries face severe execution drag from microelectronic scarcity and heavy metal fabrication bottlenecks, despite holding historic $118 billion and $53.1 billion backlogs, respectively. For institutional LPs, the actionable delta lies in pure-play technology providers bypassing legacy hardware constraints. The true alpha generation will stem from vertically integrated component monopolies controlling acoustic and navigation architectures amidst stringent export regulations.

Figure Global UUV & Subsea Technology Landscape 2025: Strategic Performance & Archetvpe Benchmark

Segmental Incremental Margins and Cash Conversion

Segmental Incremental Margins and Cash Conversion

The 2025 filings bifurcates the industry into three distinct financial archetypes: Cash-Generating Primes, High-Margin Niche Integrators, and Cash-Burning Innovators. Operating leverage is heavily distorted by Estimate at Completion (EAC) adjustments and working capital liquidations.

Table Comparative Financial Benchmarking of Defense, Marine Technology, and Robotics Companies (FY2025)

Unit Economics & CapEx Realignment:

* Asset Turnover Outliers: Forum Energy operates an asset-light consumable model achieving 1.05x turnover, whereas Nauticus Robotics sits at a distressed 0.12x turnover, holding $42.5 million in assets but failing to generate commercial traction.

* Contract Anomalies: Huntington Ingalls recorded gross unfavorable cumulative catch-up adjustments of -$350 million tied to the Newport News shipyard facility (specifically aircraft carriers and the Virginia-class submarine program delivering through 2034).

* Capitalizing vs. Expensing R&D: Saab capitalized $74.5 million in development costs, pushing 2025 free cash flow higher but building long-term amortization pressure. Kongsberg similarly capitalized $27.2 million.

Supply Chain Audit & Geo-Economic Moat: Execution Bottlenecks

The physicality of the subsea supply chain remains the primary threat to the conversion of Remaining Performance Obligations (RPO) into recognized revenue.

* Geopolitical Material Scarcity: Teledyne faces explicit margin threats due to Chinese export restrictions on critical gallium and germanium, directly impacting its semiconductor and digital imaging divisions. Cross-strait geopolitical tensions involving Taiwan, Province of China, present existential threats to the trans-Pacific microelectronics supply chain upon which L3Harris and General Dynamics depend for C6ISR integrations.

* Regulatory Friction: Export control regimes strictly cap the Total Addressable Market (TAM). Nauticus Robotics' expansion into the UAE via a $47.0 million funding arrangement with the Master Investment Group exposes the firm to intense EAR/ITAR scrutiny. European primes like Kongsberg and Saab operate under the Norwegian Ministry of Foreign Affairs (DEKSA) and the Swedish Inspectorate of Strategic Products (ISP), which restrict sales based on human rights assessments.

* Tier-1 Component Dependency: The industry is strictly bound by single-source dependencies for untethered Autonomous Underwater Vehicles (AUVs). Nauticus Robotics relies heavily on SubCTech (Germany) for defense-grade lithium-ion battery modules. Ongoing Middle Eastern maritime shipping reroutes dramatically increase the freight cost and timeline for delivering these highly regulated, thermal-runaway-prone modules.

* Regional Footprints & Joint Ventures: James Fisher is shifting reliance away from the Middle East/Africa via a staged closure of legacy operations, pivoting to the Indo-Pacific through strategic alliances with ST Engineering Marine (Singapore) and Larsen & Toubro to deploy Tactical Diving Vehicles by Q4 2026.

HDIN Institutional Perspective

The Structural Vulnerability of the Integrator Model

We view the current CapEx and R&D deployments of legacy defense primes as a severe long-term risk. General Dynamics and Huntington Ingalls report internal R&D-to-revenue intensities below 1%, actively choosing to deploy billions in CapEx toward physical infrastructure (e.g., HII’s multi-purpose carrier refueling center and submarine manufacturing centers of excellence). While this satiates near-term naval demands (like the 2030 Columbia-class deliveries), it effectively outsources AI and autonomy R&D to government-funded contracts. If primes fail to internalize software moats like HII's Odyssey autonomy suite or Saab’s Autonomous Ocean Core, they risk being downgraded to low-margin "metal-benders."

Conversely, Nauticus Robotics’ decision to slash 2025 R&D to $0 is a critical red flag. Management cites "technological feasibility," but our forensic audit indicates desperate cash conservation. The $14.2 million acquisition of the SeaTrepid ROV fleet and the $0.5 million Olympic Arm inventory write-down suggest Nauticus is abandoning its software-first autonomous moat for a traditional, capital-intensive subsea services model that the Street has not accurately priced. We confirm that true structural defensibility resides with upstream hardware monopolists—Teledyne, Kongsberg, and Exail—who control the proprietary Intellectual Property for Inertial Navigation Systems (INS) and Doppler Velocity Logs (DVL), dictating terms to the rest of the supply chain.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure Global UUV & Subsea Technology Landscape 2025: Strategic Performance & Archetvpe Benchmark

Segmental Incremental Margins and Cash ConversionThe 2025 filings bifurcates the industry into three distinct financial archetypes: Cash-Generating Primes, High-Margin Niche Integrators, and Cash-Burning Innovators. Operating leverage is heavily distorted by Estimate at Completion (EAC) adjustments and working capital liquidations.

Table Comparative Financial Benchmarking of Defense, Marine Technology, and Robotics Companies (FY2025)

| Entity (Ticker) | 2025 Total Revenue | Net Profit Margin | R&D-to-Revenue | OCF to Net Income (Cash Conversion) |

|---|---|---|---|---|

| General Dynamics | $52.55 Billion | 8.01% | 0.92% | 1.21x |

| L3Harris Technologies | $21.86 Billion | 7.34% | 2.00% | Distorted by $47M EAC drag |

| Huntington Ingalls Industries | $12.48 Billion | 4.84% | 0.21% | 1.97x |

| Saab AB | $8.07 Billion | 8.03% | 15.86% | 1.90x |

| Teledyne Technologies | $6.11 Billion | 14.63% | 5.19% | 1.33x |

| Kongsberg Gruppen | $5.58 Billion | 13.51% | 3.78% | 1.60x |

| Forum Energy Technologies | $791.4 Million | -1.22% | N/A | Driven by working capital liquidation |

| James Fisher and Sons | $520.2 Million | -1.09% | ~1.95% | N/A |

| General Oceans | $124.1 Million | 12.66% | 1.20% | 1.63x |

| Deepinfar | $49.3 Million | -2.81% | 14.79% | Positive Cash Flow |

| Nauticus Robotics | $5.27 Million | -774.0% | 0.00% | Negative Cash Flow |

* Asset Turnover Outliers: Forum Energy operates an asset-light consumable model achieving 1.05x turnover, whereas Nauticus Robotics sits at a distressed 0.12x turnover, holding $42.5 million in assets but failing to generate commercial traction.

* Contract Anomalies: Huntington Ingalls recorded gross unfavorable cumulative catch-up adjustments of -$350 million tied to the Newport News shipyard facility (specifically aircraft carriers and the Virginia-class submarine program delivering through 2034).

* Capitalizing vs. Expensing R&D: Saab capitalized $74.5 million in development costs, pushing 2025 free cash flow higher but building long-term amortization pressure. Kongsberg similarly capitalized $27.2 million.

Supply Chain Audit & Geo-Economic Moat: Execution Bottlenecks

The physicality of the subsea supply chain remains the primary threat to the conversion of Remaining Performance Obligations (RPO) into recognized revenue.

* Geopolitical Material Scarcity: Teledyne faces explicit margin threats due to Chinese export restrictions on critical gallium and germanium, directly impacting its semiconductor and digital imaging divisions. Cross-strait geopolitical tensions involving Taiwan, Province of China, present existential threats to the trans-Pacific microelectronics supply chain upon which L3Harris and General Dynamics depend for C6ISR integrations.

* Regulatory Friction: Export control regimes strictly cap the Total Addressable Market (TAM). Nauticus Robotics' expansion into the UAE via a $47.0 million funding arrangement with the Master Investment Group exposes the firm to intense EAR/ITAR scrutiny. European primes like Kongsberg and Saab operate under the Norwegian Ministry of Foreign Affairs (DEKSA) and the Swedish Inspectorate of Strategic Products (ISP), which restrict sales based on human rights assessments.

* Tier-1 Component Dependency: The industry is strictly bound by single-source dependencies for untethered Autonomous Underwater Vehicles (AUVs). Nauticus Robotics relies heavily on SubCTech (Germany) for defense-grade lithium-ion battery modules. Ongoing Middle Eastern maritime shipping reroutes dramatically increase the freight cost and timeline for delivering these highly regulated, thermal-runaway-prone modules.

* Regional Footprints & Joint Ventures: James Fisher is shifting reliance away from the Middle East/Africa via a staged closure of legacy operations, pivoting to the Indo-Pacific through strategic alliances with ST Engineering Marine (Singapore) and Larsen & Toubro to deploy Tactical Diving Vehicles by Q4 2026.

HDIN Institutional Perspective

The Structural Vulnerability of the Integrator Model

We view the current CapEx and R&D deployments of legacy defense primes as a severe long-term risk. General Dynamics and Huntington Ingalls report internal R&D-to-revenue intensities below 1%, actively choosing to deploy billions in CapEx toward physical infrastructure (e.g., HII’s multi-purpose carrier refueling center and submarine manufacturing centers of excellence). While this satiates near-term naval demands (like the 2030 Columbia-class deliveries), it effectively outsources AI and autonomy R&D to government-funded contracts. If primes fail to internalize software moats like HII's Odyssey autonomy suite or Saab’s Autonomous Ocean Core, they risk being downgraded to low-margin "metal-benders."

Conversely, Nauticus Robotics’ decision to slash 2025 R&D to $0 is a critical red flag. Management cites "technological feasibility," but our forensic audit indicates desperate cash conservation. The $14.2 million acquisition of the SeaTrepid ROV fleet and the $0.5 million Olympic Arm inventory write-down suggest Nauticus is abandoning its software-first autonomous moat for a traditional, capital-intensive subsea services model that the Street has not accurately priced. We confirm that true structural defensibility resides with upstream hardware monopolists—Teledyne, Kongsberg, and Exail—who control the proprietary Intellectual Property for Inertial Navigation Systems (INS) and Doppler Velocity Logs (DVL), dictating terms to the rest of the supply chain.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."