BioVentrix: Surgical-Only Pivot Near Mansfield Headquarters as $14.6M Working Capital Deficit Signals Distressed Bridge Financing

Date : 2026-05-20

Reading : 115

BioVentrix’s disclosures reveal a critical juncture for institutional LPs: a pre-revenue MedTech entity utilizing a proposed $15.0 million IPO strictly as distressed bridge financing rather than a commercialization vehicle. By abandoning its hybrid surgical approach for a cardiothoracic-only procedure, the company is attempting to salvage its flagship Revivent System. However, with operations tethered to a single Massachusetts facility and a $14.61 million working capital deficit, the firm faces a severe 2028 FDA timeline bottleneck that standard venture capital has eschewed in favor of highly dilutive, insider-led 15% debt.

Figure BioVentrix Strategic Overview: A Bridge to Structural Heart Innovation

Capital Structure Distresses & RELIVE Trial Unit Economics

Capital Structure Distresses & RELIVE Trial Unit Economics

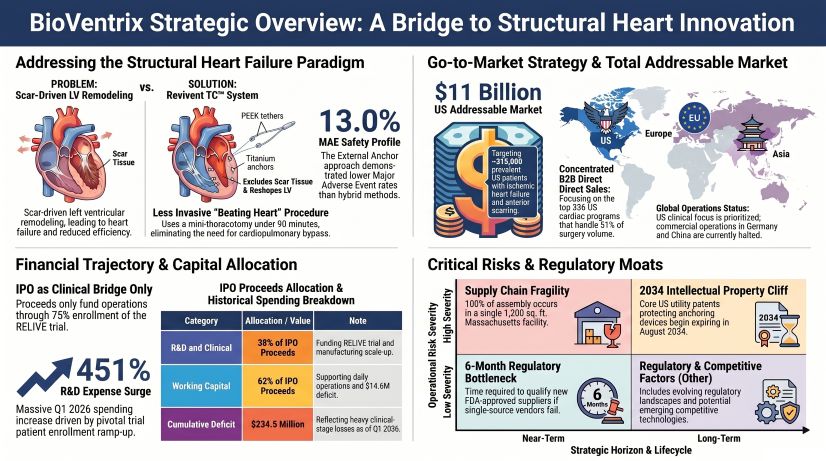

BioVentrix (NASDAQ: BVTR) presents an asset-light, cash-incinerating financial profile defined entirely by its pivot to the 126-patient (84 treated; 42 control) RELIVE pivotal trial. Following the failure of the ALIVE trial’s primary efficacy endpoints, the company abandoned its hybrid approach (which yielded a 20.0% Major Adverse Event rate) in favor of a strictly surgical External Anchor approach (13.0% MAE rate). This clinical pivot has drastically accelerated operating leverage deterioration.

The company generated $0 in commercial revenue across FY2024, FY2025, and Q1 2026, having intentionally halted European operations—which historically accounted for 338 global procedures (including 109 in Germany and 38 in the Czech Republic)—at the end of 2023. Unit economics currently rely on a $25,000 per-procedure clinical site reimbursement, recorded strictly as an R&D offset.

Financial & Capital Structure Inventory (As of Q1 2026)

* Operating Leverage Breakdown: R&D expenses surged 99% in FY2025 and 451% in Q1 2026 ($597,576), directly tracking the RELIVE trial ramp-up (patient enrollment began September 2025). SG&A expanded 116% YoY in Q1 2026 to $2.08 million.

* Liquidity Crisis: The Q1 2026 balance sheet holds merely $924,026 in cash against a staggering $14.61 million working capital deficit. The accumulated deficit stands at $234.49 million.

* Debt Servicing & Insider Capital: Net loss expansion outpaced operating losses driven by a 349% YoY increase in interest expenses in FY2025. The capital stack is burdened by $10.88 million in secured convertible promissory notes compounding at a punitive 15% interest rate, heavily funded by corporate insiders via complex equity "sweetener" round-tripping.

* Internal Capital Allocation (IPO): The anticipated $15.0 million gross IPO proceeds allocate 0% to commercial launch. Instead, 38% is earmarked for R&D/manufacturing and 62% for working capital—providing just enough runway to enroll 75% of the RELIVE patients and fund operations for exactly three months thereafter.

Massachusetts Concentration & The 6-Month Bottleneck

BioVentrix’s operational architecture exhibits extreme supplier concentration and geographic fragility. The company’s entire physical footprint, corporate headquarters, and R&D epicenter are hyper-consolidated into a single 9,000-square-foot leased facility in Mansfield, Massachusetts.

* Assembly Node Vulnerability: 100% of internal manufacturing, final inspection, testing, and pouch-sealing for the Revivent System is executed within a minimal 1,200-square-foot ISO 13485-certified Class 8 cleanroom in the Mansfield facility. Net Property and Equipment is immaterial at just $90,390, reflecting the asset-light vulnerability of the firm.

* Tier-1 Single-Source Dependencies: BioVentrix relies on single-source suppliers without long-term contracts for nearly all external components, including its proprietary titanium anchors, PEEK tethers, and outsourced "Force Gauge." Final finished-product sterilization is monopolized by a single third-party gamma radiation vendor.

* The Regulatory Bottleneck: Management estimates a severe six-month lead time to identify, test, and qualify an alternative FDA-approved supplier in the event of a disruption. Because the firm carries $0 in capitalized inventory (expensing all RELIVE trial production under ASC 730), any localized Massachusetts disruption or third-party vendor failure would immediately halt clinical supply, devastating the target of gathering Q1 2028 six-month follow-up data for a mid-2028 FDA PMA submission.

HDIN Institutional Perspective

While BioVentrix models an $11 billion U.S. Total Addressable Market (TAM) anchored by a projected $35,000 ASP and a hypothetical $50,000 Diagnosis-Related Group (DRG) hospital reimbursement, the capital architecture suggests a severe commercialization mismatch.

The Street may interpret the proposed IPO as a commercial launchpad targeting the 315,000 U.S. prevalent patients suffering from scar-induced HFrEF. However, our differentiated viewpoint concludes this offering is merely a distressed bridge. The company’s pipeline asset, Alginate, has already seen its CE mark lapse, requiring a new FDA IDE submission that the current balance sheet cannot support. Furthermore, BioVentrix is currently defending a fiduciary class-action lawsuit brought by Gary Moline regarding a punitive 1-for-65,500 reverse stock split, carrying a $600,000 contingent liability.

With core U.S. utility patents expiring in August 2034 and a 180-day FINRA lock-up governing the post-IPO float, the firm's extreme reliance on 15% convertible notes guarantees immediate, punitive dilution for public entrants. Without intervention from tier-one strategic acquirers (e.g., Johnson & Johnson or Medtronic), BioVentrix's survival to the mid-2028 FDA approval window remains highly speculative.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Figure BioVentrix Strategic Overview: A Bridge to Structural Heart Innovation

Capital Structure Distresses & RELIVE Trial Unit EconomicsBioVentrix (NASDAQ: BVTR) presents an asset-light, cash-incinerating financial profile defined entirely by its pivot to the 126-patient (84 treated; 42 control) RELIVE pivotal trial. Following the failure of the ALIVE trial’s primary efficacy endpoints, the company abandoned its hybrid approach (which yielded a 20.0% Major Adverse Event rate) in favor of a strictly surgical External Anchor approach (13.0% MAE rate). This clinical pivot has drastically accelerated operating leverage deterioration.

The company generated $0 in commercial revenue across FY2024, FY2025, and Q1 2026, having intentionally halted European operations—which historically accounted for 338 global procedures (including 109 in Germany and 38 in the Czech Republic)—at the end of 2023. Unit economics currently rely on a $25,000 per-procedure clinical site reimbursement, recorded strictly as an R&D offset.

Financial & Capital Structure Inventory (As of Q1 2026)

* Operating Leverage Breakdown: R&D expenses surged 99% in FY2025 and 451% in Q1 2026 ($597,576), directly tracking the RELIVE trial ramp-up (patient enrollment began September 2025). SG&A expanded 116% YoY in Q1 2026 to $2.08 million.

* Liquidity Crisis: The Q1 2026 balance sheet holds merely $924,026 in cash against a staggering $14.61 million working capital deficit. The accumulated deficit stands at $234.49 million.

* Debt Servicing & Insider Capital: Net loss expansion outpaced operating losses driven by a 349% YoY increase in interest expenses in FY2025. The capital stack is burdened by $10.88 million in secured convertible promissory notes compounding at a punitive 15% interest rate, heavily funded by corporate insiders via complex equity "sweetener" round-tripping.

* Internal Capital Allocation (IPO): The anticipated $15.0 million gross IPO proceeds allocate 0% to commercial launch. Instead, 38% is earmarked for R&D/manufacturing and 62% for working capital—providing just enough runway to enroll 75% of the RELIVE patients and fund operations for exactly three months thereafter.

Massachusetts Concentration & The 6-Month Bottleneck

BioVentrix’s operational architecture exhibits extreme supplier concentration and geographic fragility. The company’s entire physical footprint, corporate headquarters, and R&D epicenter are hyper-consolidated into a single 9,000-square-foot leased facility in Mansfield, Massachusetts.

* Assembly Node Vulnerability: 100% of internal manufacturing, final inspection, testing, and pouch-sealing for the Revivent System is executed within a minimal 1,200-square-foot ISO 13485-certified Class 8 cleanroom in the Mansfield facility. Net Property and Equipment is immaterial at just $90,390, reflecting the asset-light vulnerability of the firm.

* Tier-1 Single-Source Dependencies: BioVentrix relies on single-source suppliers without long-term contracts for nearly all external components, including its proprietary titanium anchors, PEEK tethers, and outsourced "Force Gauge." Final finished-product sterilization is monopolized by a single third-party gamma radiation vendor.

* The Regulatory Bottleneck: Management estimates a severe six-month lead time to identify, test, and qualify an alternative FDA-approved supplier in the event of a disruption. Because the firm carries $0 in capitalized inventory (expensing all RELIVE trial production under ASC 730), any localized Massachusetts disruption or third-party vendor failure would immediately halt clinical supply, devastating the target of gathering Q1 2028 six-month follow-up data for a mid-2028 FDA PMA submission.

HDIN Institutional Perspective

While BioVentrix models an $11 billion U.S. Total Addressable Market (TAM) anchored by a projected $35,000 ASP and a hypothetical $50,000 Diagnosis-Related Group (DRG) hospital reimbursement, the capital architecture suggests a severe commercialization mismatch.

The Street may interpret the proposed IPO as a commercial launchpad targeting the 315,000 U.S. prevalent patients suffering from scar-induced HFrEF. However, our differentiated viewpoint concludes this offering is merely a distressed bridge. The company’s pipeline asset, Alginate, has already seen its CE mark lapse, requiring a new FDA IDE submission that the current balance sheet cannot support. Furthermore, BioVentrix is currently defending a fiduciary class-action lawsuit brought by Gary Moline regarding a punitive 1-for-65,500 reverse stock split, carrying a $600,000 contingent liability.

With core U.S. utility patents expiring in August 2034 and a 180-day FINRA lock-up governing the post-IPO float, the firm's extreme reliance on 15% convertible notes guarantees immediate, punitive dilution for public entrants. Without intervention from tier-one strategic acquirers (e.g., Johnson & Johnson or Medtronic), BioVentrix's survival to the mid-2028 FDA approval window remains highly speculative.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."