Zhejiang Huasheng Radar: Vertical Integration Pivot Near Shaoxing Smart Manufacturing Center as -78.98% OCF-to-Net-Profit Conversion Signals Severe B2G Liquidity Constraints

Date : 2026-05-19

Reading : 109

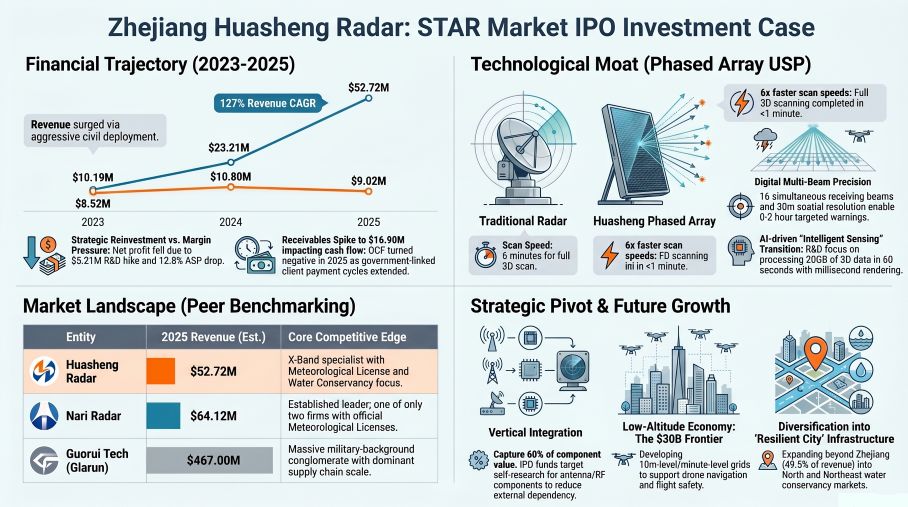

Zhejiang Huasheng Radar’s planned $150 million IPO attempts to paper over a severe working capital mismatch. While 2025 top-line revenue reached $52.72 million, the ballooning of accounts receivable to $16.89 million drove operating cash flows to a negative $7.12 million. This degradation in cash conversion exposes the systemic vulnerability of its B2G reliance, specifically on localized Zhejiang provincial meteorological budgets. For institutional LPs, the critical variable heading into 2026 is whether the Shaoxing facility expansion can internalize component margins before extended government payment cycles trigger a structural liquidity event.

Forensic Analysis of Financials & Segmental Operating Leverage

Zhejiang Huasheng Radar exhibits a classic early-stage commercialization profile: exponential top-line growth paired with compressing internal capital allocation efficiency. A forensic audit of the 2023–2025 operational metrics reveals significant price-mix variance and deteriorating unit economics.

* Revenue Trajectory & Profitability Compression: Top-line revenue surged at a 127.48% CAGR, from $10.19 million (2023) to $49.19 million (2024), culminating at $52.72 million in 2025. However, net profit contracted by 16.5% year-over-year in 2025 to $9.02 million, squeezed by rising impairment losses and R&D expenditures.

* Price-Mix Variance: The Average Selling Price (ASP) for radar units dropped 12.85% in 2025 to $706,602. This deflation is directly attributed to a strategic product mix shift toward lower-priced water conservancy rain-measuring radars and aggressive volume discounting granted to its largest client, Blue Sky Meteorology.

* Operating Leverage & Unit Economics: Main business gross margin stabilized at 45.40% in 2025 (up from 31.02% in 2023). The high-margin Software & O&M segment yielded a 52.53% gross margin, yet remains a fraction of total revenue (4.81% in 2025), preventing a software-SaaS valuation multiple.

* Internal Capital Allocation & Liquidity Matrix:

* *Operating Cash Flow (OCF)*: Collapsed from +$16.54 million in 2024 to -$7.12 million in 2025.

* *Free Cash Flow Conversion*: The OCF-to-Net-Profit ratio inverted violently to -78.98% in 2025.

* *Receivables Backlog*: Accounts receivable spiked from $4.78 million (2024) to $16.89 million (2025). Consequently, the AR turnover rate plummeted from 18.28x to 5.23x.

* *R&D-to-Moat Translation*: R&D expenses increased by $1.59 million YoY in 2025 to $5.21 million. Total 3-year R&D spend represents 11.08% of cumulative revenue ($10.80 million).

Figure Zhejiang Huasheng Radar: STAR Market lPo Investment Case

Supply Chain Audit & Geo-Economic Moat

Supply Chain Audit & Geo-Economic Moat

Zhejiang Huasheng Radar operates a highly concentrated physical and geographic footprint. Its manufacturing strategy relies on a "produce based on sales" model, exposing the firm to strict regional dependencies and Tier-1 supplier bottlenecks.

* The Shaoxing Smart Manufacturing Hub: Functioning as the core production artery, the Shaoxing Smart Manufacturing Center achieved a 90.91% capacity utilization rate in 2025 (producing 60 of 66 capable units). The company’s structural reliance on external customized components is severe; antenna components currently account for ~60% of radar build costs. The $141 million Capex allocation (drawing $122 million from the proposed IPO) is earmarked strictly for this Shaoxing site to internalize component manufacturing.

* Tier-1 Supplier Concentration Risk: The procurement ecosystem lacks vertical integration. In 2025, Xi'an Yiding Intelligent Technology Co., Ltd. commanded 28.41% of raw material spend ($6.83 million) for antenna components, while Shijiazhuang Shilianda Technology Co., Ltd. accounted for 9.05% ($2.18 million) for servo components.

* Geographic Sales Footprint: The company exhibits extreme localized dependency on the East China market. Zhejiang Province generated 49.47% of total revenue in 2025 (down from 63.93% in 2024). Single-client concentration risk is critical, with Blue Sky Meteorology (a Zhejiang state-owned entity) contributing 28.60% of 2025 revenues. Geographically targeted mitigation efforts have secured nominal footholds in North China (Tangshan and Shijiazhuang Meteorological Bureaus) and Northeast China (Jilin Provincial Hydrology Bureau).

* The Beijing AI Proving Ground: A $28.02 million Capex injection is mapped for the Beijing R&D Center, targeting AI-driven algorithms for the nascent Low-Altitude Economy and drone-route meteorological tracking.

HDIN Institutional Perspective

While Zhejiang Huasheng Radar aggressively pitches a high-margin "software-defined" future via its X-Band Dual-Polarization Phased Array technology, the reality of its balance sheet reveals a highly vulnerable, hardware-heavy defense contractor model. The 253% surge in accounts receivable against a mere 7.1% revenue growth in 2025 highlights a dangerous reliance on prolonged municipal B2G budget cycles. Furthermore, with nearly 40% of its raw material costs locked into external Tier-1 suppliers, the company’s ability to defend its 45.40% gross margins against military-grade, heavily capitalized incumbents like Guorui Technology remains structurally weak. If the Shaoxing vertical integration project is not executed flawlessly ahead of 2026, the current negative FCF trajectory threatens to erode its operational runway, rendering the localized Zhejiang market monopoly insufficient to sustain public market valuation expectations.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant)*:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."

Forensic Analysis of Financials & Segmental Operating Leverage

Zhejiang Huasheng Radar exhibits a classic early-stage commercialization profile: exponential top-line growth paired with compressing internal capital allocation efficiency. A forensic audit of the 2023–2025 operational metrics reveals significant price-mix variance and deteriorating unit economics.

* Revenue Trajectory & Profitability Compression: Top-line revenue surged at a 127.48% CAGR, from $10.19 million (2023) to $49.19 million (2024), culminating at $52.72 million in 2025. However, net profit contracted by 16.5% year-over-year in 2025 to $9.02 million, squeezed by rising impairment losses and R&D expenditures.

* Price-Mix Variance: The Average Selling Price (ASP) for radar units dropped 12.85% in 2025 to $706,602. This deflation is directly attributed to a strategic product mix shift toward lower-priced water conservancy rain-measuring radars and aggressive volume discounting granted to its largest client, Blue Sky Meteorology.

* Operating Leverage & Unit Economics: Main business gross margin stabilized at 45.40% in 2025 (up from 31.02% in 2023). The high-margin Software & O&M segment yielded a 52.53% gross margin, yet remains a fraction of total revenue (4.81% in 2025), preventing a software-SaaS valuation multiple.

* Internal Capital Allocation & Liquidity Matrix:

* *Operating Cash Flow (OCF)*: Collapsed from +$16.54 million in 2024 to -$7.12 million in 2025.

* *Free Cash Flow Conversion*: The OCF-to-Net-Profit ratio inverted violently to -78.98% in 2025.

* *Receivables Backlog*: Accounts receivable spiked from $4.78 million (2024) to $16.89 million (2025). Consequently, the AR turnover rate plummeted from 18.28x to 5.23x.

* *R&D-to-Moat Translation*: R&D expenses increased by $1.59 million YoY in 2025 to $5.21 million. Total 3-year R&D spend represents 11.08% of cumulative revenue ($10.80 million).

Figure Zhejiang Huasheng Radar: STAR Market lPo Investment Case

Supply Chain Audit & Geo-Economic MoatZhejiang Huasheng Radar operates a highly concentrated physical and geographic footprint. Its manufacturing strategy relies on a "produce based on sales" model, exposing the firm to strict regional dependencies and Tier-1 supplier bottlenecks.

* The Shaoxing Smart Manufacturing Hub: Functioning as the core production artery, the Shaoxing Smart Manufacturing Center achieved a 90.91% capacity utilization rate in 2025 (producing 60 of 66 capable units). The company’s structural reliance on external customized components is severe; antenna components currently account for ~60% of radar build costs. The $141 million Capex allocation (drawing $122 million from the proposed IPO) is earmarked strictly for this Shaoxing site to internalize component manufacturing.

* Tier-1 Supplier Concentration Risk: The procurement ecosystem lacks vertical integration. In 2025, Xi'an Yiding Intelligent Technology Co., Ltd. commanded 28.41% of raw material spend ($6.83 million) for antenna components, while Shijiazhuang Shilianda Technology Co., Ltd. accounted for 9.05% ($2.18 million) for servo components.

* Geographic Sales Footprint: The company exhibits extreme localized dependency on the East China market. Zhejiang Province generated 49.47% of total revenue in 2025 (down from 63.93% in 2024). Single-client concentration risk is critical, with Blue Sky Meteorology (a Zhejiang state-owned entity) contributing 28.60% of 2025 revenues. Geographically targeted mitigation efforts have secured nominal footholds in North China (Tangshan and Shijiazhuang Meteorological Bureaus) and Northeast China (Jilin Provincial Hydrology Bureau).

* The Beijing AI Proving Ground: A $28.02 million Capex injection is mapped for the Beijing R&D Center, targeting AI-driven algorithms for the nascent Low-Altitude Economy and drone-route meteorological tracking.

HDIN Institutional Perspective

While Zhejiang Huasheng Radar aggressively pitches a high-margin "software-defined" future via its X-Band Dual-Polarization Phased Array technology, the reality of its balance sheet reveals a highly vulnerable, hardware-heavy defense contractor model. The 253% surge in accounts receivable against a mere 7.1% revenue growth in 2025 highlights a dangerous reliance on prolonged municipal B2G budget cycles. Furthermore, with nearly 40% of its raw material costs locked into external Tier-1 suppliers, the company’s ability to defend its 45.40% gross margins against military-grade, heavily capitalized incumbents like Guorui Technology remains structurally weak. If the Shaoxing vertical integration project is not executed flawlessly ahead of 2026, the current negative FCF trajectory threatens to erode its operational runway, rendering the localized Zhejiang market monopoly insufficient to sustain public market valuation expectations.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.

*2026 AI Transparency Footer (C2PA Compliant)*:

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."