CXMT Corporation: Strategic Equipment Localization Near Hefei Hub as Conservative Accounting Signals Genuine FY2025 Profitability

Date : 2026-05-19

Reading : 169

CXMT Corporation’s FY2025 prospectus indicates a critical inflection point for global memory markets. By aggressively compressing R&D capitalization to absolute zero, the company engineered a mathematically pristine $993.98 million net profit reversal. For institutional LPs, the actionable narrative lies in the proposed $4.10 billion IPO allocation: a structural pivot from defensive geopolitical compliance to offensive supply chain localization. As international export controls threaten access to advanced Wafer Fabrication Equipment (WFE), CXMT is utilizing its 12-inch mega-fabs as live qualification environments for domestic suppliers, fundamentally altering the global DRAM dependency calculus.

Figure CXMT Strategic lPO Blueprint: Scaling the Global DRAM Frontier

Forensic Financials & Structural Margin Analysis

Forensic Financials & Structural Margin Analysis

CXMT reveals an underlying cash-generative engine historically masked by ultra-conservative accounting policies and front-loaded capital expenditures.

Segmental Inventory & Earnings Quality Audit

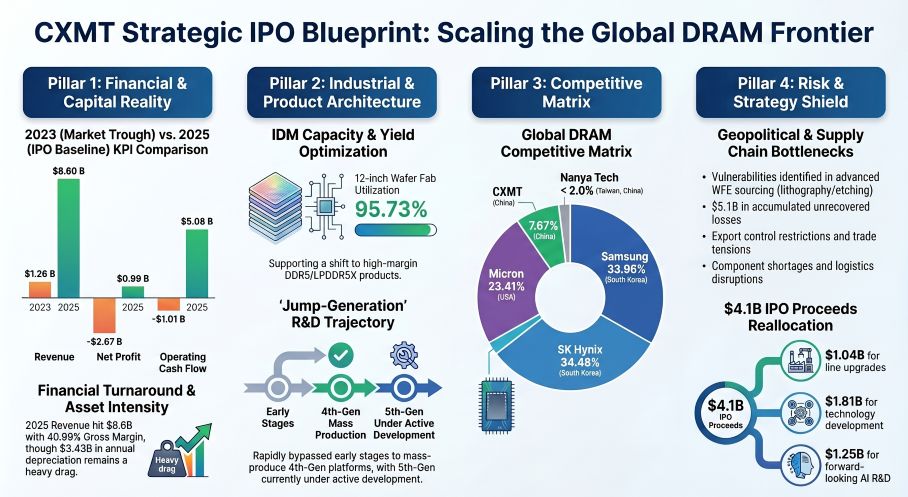

* R&D Capitalization & Profitability: CXMT dropped its R&D capitalization rate from 27.34% in 2024 to 0% in 2025. The FY2025 net profit of $993.98 million (CNY 7.14 billion) is entirely organically driven by scale and DDR5 / LPDDR5X premium pricing, completely devoid of accounting inflation.

* Depreciation Drag (Hidden Margin Reserve): Management enforces a highly aggressive 5-8 year depreciation lifespan for Machinery & Equipment, significantly shorter than the 5-16 year range utilized by peers like SK Hynix and Nanya Tech. In FY2025, this resulted in a $3.43 billion fixed asset depreciation charge. This front-loaded accounting suppresses reported gross margins while shielding core operating cash flows.

* Receivables & Liquidity: Counterparty risk is virtually non-existent. CXMT commands an accounts receivable turnover ratio of 36.49x, with 97.2% of its $213.11 million AR balance aged under six months. The expected credit loss provision sits at a highly conservative 0.51%.

* Forward Guidance (H1 2026): Management projections model an aggressive revenue target of $15.30 billion to $16.69 billion (612%–677% YoY growth), targeting an anticipated net profit ceiling of $10.43 billion as next-generation server memory penetration accelerates.

Table Strategic Capital Expenditure and Technology Roadmap

The Hefei-Beijing Axis and WFE Localization Imperative

CXMT’s physical footprint relies heavily on its dual 12-inch wafer fabrication hubs in Hefei and Beijing, supported by its wholly-owned back-end subsidiary, CXMT Products (Hefei) Co., Ltd. Currently capturing 7.67% of the global DRAM market (Q4 2025), the company operates a hybrid IDM model—utilizing proprietary fabs for front-end manufacturing while deploying a dual-track autonomous and outsourced model for back-end module testing.

Supply Chain Vulnerability & Defensive Localization

The prospectus explicitly flags international export controls on critical WFE (lithography, etching, thin-film deposition, and CMP) as a primary operational threat. The reliance on unnamed "Supplier J, C, G, F, and K" for multi-million dollar framework agreements exposes the Hefei-Beijing axis to severe geopolitical friction.

To mitigate this, CXMT is systematically executing a supply chain shock-proofing strategy. The $1.04 billion allocated for the Wafer Fab Tech Upgrade explicitly mandates the "verification and development of localized and novel equipment." Rather than merely expanding capacity, CXMT is operating its high-yield lines as testing grounds for domestic Tier-1 suppliers, engineering an irreversible decoupling from restricted foreign capital equipment dependencies.

HDIN Institutional Perspective

While retail consensus may fixate on the $5.10 billion in accumulated unrecovered losses and the massive inventory working capital lock-up (exceeding 250 implied turnover days), our forensic analysis yields a differentiated viewpoint. The Street has largely mispriced CXMT's capital structure.

The company is buttressed by an impenetrable "patient capital" fortress. Over 36% of pre-IPO shares are held by state-affiliated entities (including Hefei Industrial, CX Integration, and Big Fund II), which provide the implicit >$1.00 billion syndicated loan guarantees required to sustain continuous IDM CapEx. Furthermore, the governance architecture enforces draconian retention mechanics: a strict 36-month post-IPO lock-up for institutional capital, tied to performance benchmarks, combined with Chairman Zhu Yiming’s pledge to distribute 50% of his equity to grassroots engineers over a 10-year horizon. This structurally eliminates the risk of core R&D talent flight, securing the intellectual property moat (6,972 global patents) necessary to execute the "leapfrog" transition into 3D DRAM and AI-driven data center architectures.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

*About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.*

*2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."*

Figure CXMT Strategic lPO Blueprint: Scaling the Global DRAM Frontier

Forensic Financials & Structural Margin AnalysisCXMT reveals an underlying cash-generative engine historically masked by ultra-conservative accounting policies and front-loaded capital expenditures.

Segmental Inventory & Earnings Quality Audit

* R&D Capitalization & Profitability: CXMT dropped its R&D capitalization rate from 27.34% in 2024 to 0% in 2025. The FY2025 net profit of $993.98 million (CNY 7.14 billion) is entirely organically driven by scale and DDR5 / LPDDR5X premium pricing, completely devoid of accounting inflation.

* Depreciation Drag (Hidden Margin Reserve): Management enforces a highly aggressive 5-8 year depreciation lifespan for Machinery & Equipment, significantly shorter than the 5-16 year range utilized by peers like SK Hynix and Nanya Tech. In FY2025, this resulted in a $3.43 billion fixed asset depreciation charge. This front-loaded accounting suppresses reported gross margins while shielding core operating cash flows.

* Receivables & Liquidity: Counterparty risk is virtually non-existent. CXMT commands an accounts receivable turnover ratio of 36.49x, with 97.2% of its $213.11 million AR balance aged under six months. The expected credit loss provision sits at a highly conservative 0.51%.

* Forward Guidance (H1 2026): Management projections model an aggressive revenue target of $15.30 billion to $16.69 billion (612%–677% YoY growth), targeting an anticipated net profit ceiling of $10.43 billion as next-generation server memory penetration accelerates.

Table Strategic Capital Expenditure and Technology Roadmap

| Strategic Objective | CapEx Allocation (USD) | Core Technological Focus |

|---|---|---|

| Wafer Fab Mass Production Upgrade | $1.04 Billion | Transition toward 12-inch wafer production and synchronized domestic equipment verification. |

| DRAM Memory Technology Upgrade | $1.81 Billion | Migration of core fabrication facilities to fifth-generation DRAM process nodes. |

| Forward-Looking Research & Development | $1.25 Billion | Development of LPDDR6, 4F² architectures, Compute Express Link (CXL), and near-memory computing technologies. |

The Hefei-Beijing Axis and WFE Localization Imperative

CXMT’s physical footprint relies heavily on its dual 12-inch wafer fabrication hubs in Hefei and Beijing, supported by its wholly-owned back-end subsidiary, CXMT Products (Hefei) Co., Ltd. Currently capturing 7.67% of the global DRAM market (Q4 2025), the company operates a hybrid IDM model—utilizing proprietary fabs for front-end manufacturing while deploying a dual-track autonomous and outsourced model for back-end module testing.

Supply Chain Vulnerability & Defensive Localization

The prospectus explicitly flags international export controls on critical WFE (lithography, etching, thin-film deposition, and CMP) as a primary operational threat. The reliance on unnamed "Supplier J, C, G, F, and K" for multi-million dollar framework agreements exposes the Hefei-Beijing axis to severe geopolitical friction.

To mitigate this, CXMT is systematically executing a supply chain shock-proofing strategy. The $1.04 billion allocated for the Wafer Fab Tech Upgrade explicitly mandates the "verification and development of localized and novel equipment." Rather than merely expanding capacity, CXMT is operating its high-yield lines as testing grounds for domestic Tier-1 suppliers, engineering an irreversible decoupling from restricted foreign capital equipment dependencies.

HDIN Institutional Perspective

While retail consensus may fixate on the $5.10 billion in accumulated unrecovered losses and the massive inventory working capital lock-up (exceeding 250 implied turnover days), our forensic analysis yields a differentiated viewpoint. The Street has largely mispriced CXMT's capital structure.

The company is buttressed by an impenetrable "patient capital" fortress. Over 36% of pre-IPO shares are held by state-affiliated entities (including Hefei Industrial, CX Integration, and Big Fund II), which provide the implicit >$1.00 billion syndicated loan guarantees required to sustain continuous IDM CapEx. Furthermore, the governance architecture enforces draconian retention mechanics: a strict 36-month post-IPO lock-up for institutional capital, tied to performance benchmarks, combined with Chairman Zhu Yiming’s pledge to distribute 50% of his equity to grassroots engineers over a 10-year horizon. This structurally eliminates the risk of core R&D talent flight, securing the intellectual property moat (6,972 global patents) necessary to execute the "leapfrog" transition into 3D DRAM and AI-driven data center architectures.

Presentation Download & Video Access:

Presentation Download: Click the PDF download link under 'Related Topics' to access the full institutional presentation of this report.

Video Link: Click this link to watch the HDIN analyst briefing on YouTube.

*About HDIN Research:

HDIN Research is a premier global market intelligence and strategic advisory firm specializing in institutional-grade financial analysis, supply chain audits, and macroeconomic forecasting. Our dedicated sector analysts deliver actionable, data-driven insights tailored for private equity, hedge funds, and corporate strategy teams. Visit us at http://www.hdinresearch.com.*

*2026 AI Transparency Footer (C2PA Compliant):

"This intelligence report was authored by HDIN Research analysts following a rigorous audit of official corporate filings. AI was utilized for massive-scale data synthesis and structural drafting, ensuring 100% inclusion of reported data points. All strategic insights, financial modeling, and final verdicts were verified by our editorial board to ensure professional accuracy and compliance with 2026 Google Search E-E-A-T standards."*